Federal Reserve Chair Kevin Warsh Signals Unwavering Commitment to Inflation Targets Amid Shifting Market Dynamics and Policy Behavioral Reforms

Federal Reserve Chair Kevin Warsh concluded his inaugural semiannual monetary policy testimony before Congress this week, delivering a resolute message to lawmakers regarding the central bank’s primary objective: a definitive return to the 2% inflation target. Over two days of intensive questioning before the House Financial Services Committee and the Senate Banking Committee, Warsh emphasized that the Federal Reserve maintains "no tolerance" for the persistently elevated price levels that have characterized the economic landscape over the past year. In a bold declaration that set the tone for his leadership, Warsh asserted that under his watch, "inflation will be a thing of the past," signaling a hawkish stance that prioritizes price stability above all other mandates.

The testimony coincided with a pivotal moment in the economic calendar. Just 90 minutes before Warsh appeared before House representatives on Tuesday, the Bureau of Labor Statistics released the June Consumer Price Index (CPI) report. The data revealed a surprising 0.4% decline in prices, the first such contraction in several months. While the market reacted with immediate optimism, Warsh maintained a disciplined, data-dependent composure. He acknowledged the report as "great news" but cautioned legislators against premature celebrations or policy pivots based on a single window of evidence. "It’s one data point," Warsh noted during the hearing. "I don’t want to overread or cherry-pick data."

A New Philosophy: Rejecting Forward Guidance and Behavioral Biases

One of the most significant departures from his predecessors was Warsh’s vocal skepticism regarding "forward guidance"—the practice of providing markets with long-term projections of future interest rate paths. Warsh argued that the central bank’s reliance on forecasts often leads to institutional inertia and cognitive biases that can cloud effective policymaking.

At the heart of Warsh’s critique is a recognition of human psychology in high-stakes financial environments. "We’re human," Warsh admitted to the committee, explaining that once a committee publishes a specific projection, its members often fall victim to "anchoring." This behavioral flaw causes policymakers to favor information that aligns with their prior forecasts while reflexively rejecting data that contradicts them. By moving away from rigid forward guidance, Warsh intends to foster a Federal Reserve that is "more circumspect" and capable of responding to real-time economic shifts without the baggage of previously stated expectations.

This shift in philosophy suggests a "pure data" approach to the upcoming Federal Open Market Committee (FOMC) meetings. Without the guardrails of forward guidance, market participants must now look more closely at actual economic outputs rather than deciphering the "dot plot" or speculative speeches from Fed officials.

Chronology of the Testimony and Market Reactions

The week began with high anticipation as investors sought clarity on the Fed’s trajectory for the second half of the year.

- Tuesday Morning: The June CPI report is released at 8:30 AM ET, showing a 0.4% monthly decline. Equity futures spiked as the "disinflation" narrative gained traction.

- Tuesday Late Morning: Chair Warsh begins his testimony before the House Financial Services Committee. He acknowledges the CPI data but refuses to commit to a rate hike or cut, emphasizing the need for a sustained trend.

- Wednesday: Warsh moves to the Senate Banking Committee. The questioning turns toward the structural independence of the Federal Reserve and the risks of a "hard landing" for the economy.

- Thursday/Friday: Market internal dynamics begin to shift. While the headline indices remain stable, a massive rotation begins as tech stocks—particularly semiconductors—experience a sharp sell-off, while small-cap and equal-weighted indices rally.

The timing of these events is critical, as the pre-FOMC blackout period begins on Saturday, July 18. This means that after Friday’s market close, Federal Reserve officials will be prohibited from making public comments until after the July 28–29 policy meeting. Consequently, Warsh’s testimony represents the final official word from the central bank leadership before the next interest rate decision.

Defending Central Bank Independence

During the hearings, several lawmakers raised concerns regarding the influence of the executive branch on monetary policy. Representative Nydia Velázquez specifically questioned whether Warsh "works for" the current administration, reflecting a broader public debate over the politicization of the Fed.

Warsh was firm in his rebuttal, reiterating the statutory independence of the institution. "We’re an independent central bank," he replied, underscoring that the Fed’s mandate is defined by Congress, not the White House. When pressed on how he would handle political pressure to lower rates ahead of an election cycle, Warsh committed only to "follow the law and follow the data." This exchange highlights the delicate balancing act the Fed must perform as it manages the dual mandate of maximum employment and stable prices in a highly polarized political environment.

Market Analysis: The Great Rotation and Technical Extremes

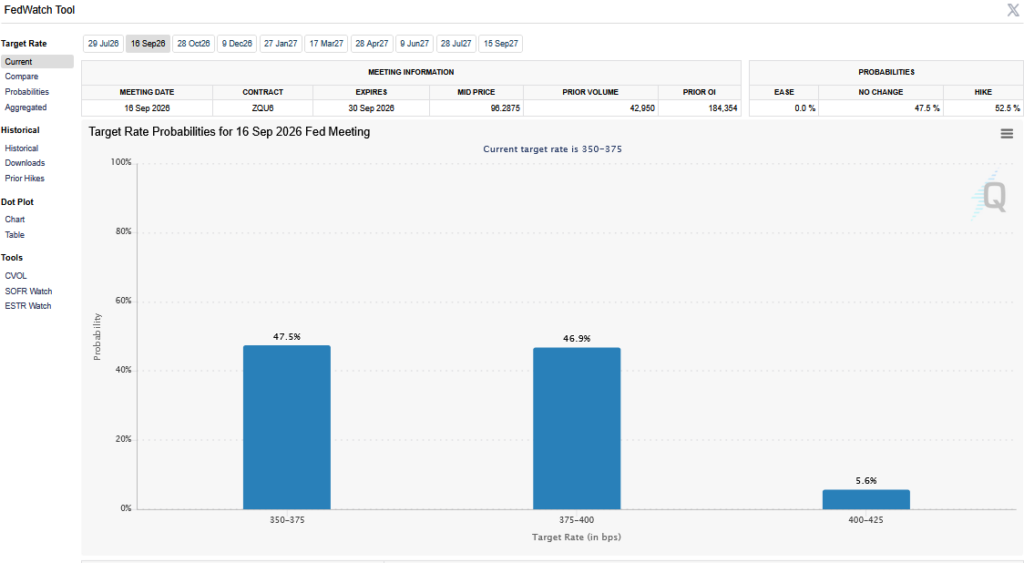

While Warsh provided the fundamental backdrop in Washington, Wall Street was busy repricing the risks of his "hawkishly data-dependent" stance. Current market data shows a Federal Reserve committee that is essentially split on the probability of a September rate hike. This uncertainty has triggered a significant "changing of seats" in equity markets.

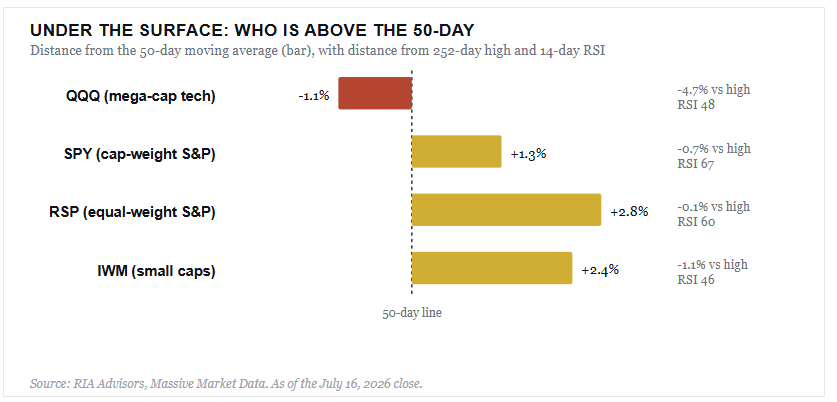

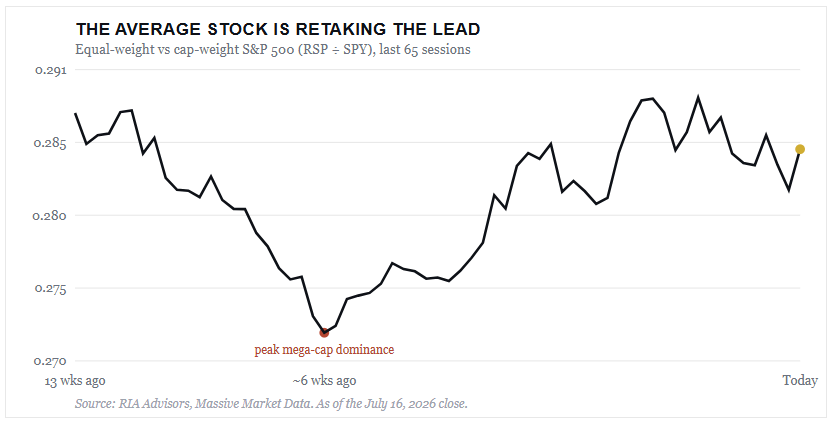

For much of the year, a handful of mega-cap technology and semiconductor stocks have driven the lion’s share of market gains. However, recent trading sessions have seen the VanEck Semiconductor ETF (SMH) drop approximately 3%, and the Nasdaq 100 slip below its 50-day moving average for the first time in months. Analysts describe this as a necessary "trimming of the parabola," as valuations in the AI-driven chip sector reached historic extremes.

Conversely, the "troops"—the broader market represented by the equal-weight S&P 500 (RSP) and small-cap stocks (IWM)—have shown remarkable resilience. As the tech "generals" retreated, the average stock advanced, pushing the equal-weight index 2.8% above its 50-day moving average. This broadening of the market is generally considered a healthy sign, but some analysts remain cautious. They suggest this rotation is being "forced" by tech deleveraging rather than a genuine surge in economic optimism. Small caps, in particular, face a challenging environment with a hawkish Fed and rising yields driven by higher oil prices.

The SK Hynix ADR Phenomenon: A Case Study in Market Inefficiency

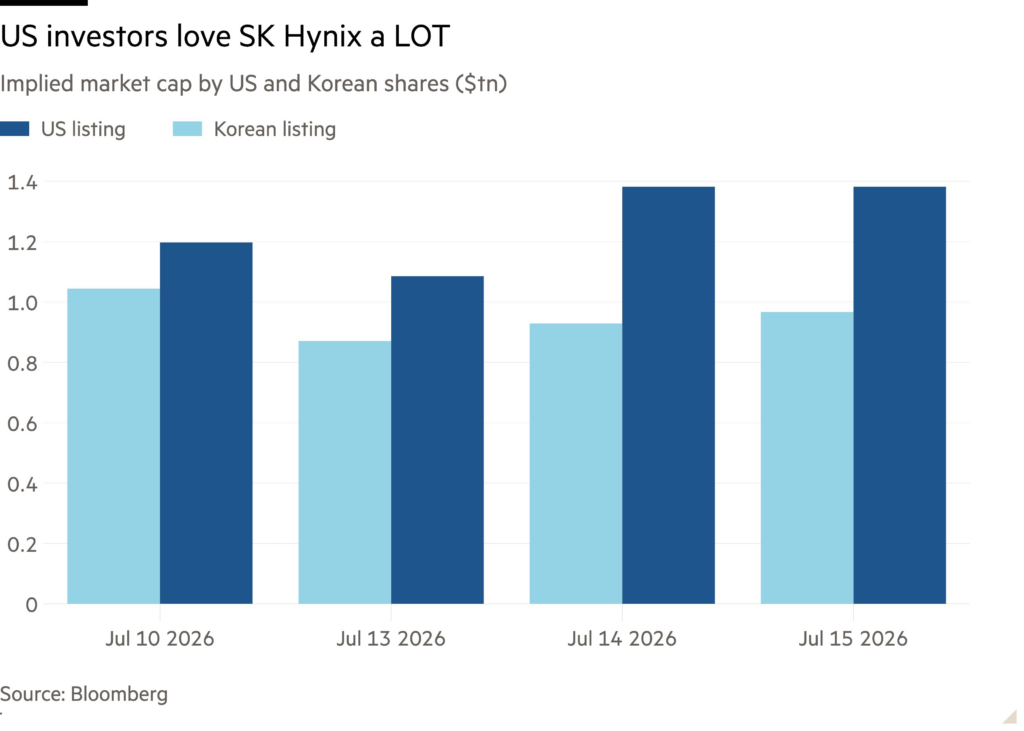

A notable sidebar to the week’s financial news was the debut of SK Hynix’s US-listed American Depositary Receipts (ADRs). The South Korean memory chip giant, a crucial player in the global AI supply chain, demonstrated a peculiar market anomaly known as a "Reverse Kimchi Premium."

Historically, South Korean companies have suffered from a "Kimchi discount," trading at lower valuations than global peers due to governance concerns. However, when SK Hynix’s ADR (SKHY) began trading on the Nasdaq, it closed at $193.92—a nearly 50% premium over its Seoul-listed shares, which closed at the equivalent of roughly $128 per share.

This massive price discrepancy for the same underlying business highlights the structural barriers in international arbitrage. While SK Hynix ADRs can be converted into Seoul-listed shares, the reverse process requires complex regulatory approval. This one-way conversion model, similar to that used by Taiwan Semiconductor Manufacturing Company (TSMC), allows US-listed premiums to persist for years. For investors, this serves as a reminder that "price" and "value" can diverge wildly based on exchange-specific liquidity and accessibility.

Broader Implications and the Path to the July Meeting

As the Federal Reserve enters its blackout period, the consensus among economists is one of watchful waiting. Warsh has successfully re-anchored the conversation around the 2% inflation target, effectively dampening hopes for an immediate, aggressive pivot to rate cuts despite the soft June CPI print.

The implications for the broader economy are multifaceted:

- Monetary Policy: The Fed is likely to maintain current rates in July, using the meeting to further digest the June data and observe if the disinflationary trend continues through July.

- Risk Management: Investors are being encouraged to "manage risk at the line," maintaining high-quality portfolios and keeping cash reserves (dry powder) to capitalize on potential pullbacks toward the S&P 500’s support levels near 7,456.

- Behavioral Shift: If Warsh succeeds in removing forward guidance, the era of "predictable" Fed moves may be over, leading to higher volatility around data releases as markets lose their long-term roadmap.

In summary, Kevin Warsh’s first congressional testimony has established a new era of Federal Reserve leadership defined by behavioral transparency, a rejection of rigid forecasting, and an uncompromising focus on the 2% inflation mandate. While the markets are currently in a state of flux—transitioning from a tech-heavy rally to a broader, more defensive posture—the "Warsh Fed" appears prepared to let the data dictate the pace of the economy, regardless of the political or market noise.

{kind=link}