How To Convince Yourself To Invest Aggressively For A Better Tomorrow

Historical Market Performance and the Probability of Investment Success

To understand the rationale behind aggressive investing, one must analyze the historical trajectory of the United States equity markets. Since 1928, the S&P 500 has demonstrated a remarkable resilience, finishing in positive territory during approximately 73% of all calendar years. This statistical reality suggests that an investor who maintains a consistent market presence has nearly a three-in-four chance of capital appreciation in any given twelve-month period. This "win rate" significantly outperforms almost all other forms of risk-adjusted wealth generation, including gambling or short-term speculative trading.

The cyclical nature of the market is further defined by the relationship between bull and bear markets. Historical data indicates that the average bull market—defined as a sustained gain of 20% or more—lasts approximately 4.4 years with a cumulative gain of roughly 155.7%. Conversely, the average bear market—a decline of 20% or more—typically persists for only 10 months with a median decline of approximately 30%. This asymmetry highlights a fundamental truth of equity investing: while market downturns are psychologically taxing and feel catastrophic in real-time, they are historically brief interlopes within much longer periods of expansion.

For instance, major market corrections such as the Great Depression (1929), the stagflation crisis of the 1970s, the Dot-com bubble (2000), and the Global Financial Crisis (2008) initially appeared as existential threats to the global economy. However, in hindsight, these events manifest as minor "blips" on a long-term upward trajectory. An investor who stays the course during a 30% decline is statistically positioned to capture a subsequent 100% or greater return during the following recovery phase. The primary obstacle to wealth accumulation is therefore not the market’s volatility, but rather the investor’s psychological reaction to it.

Opportunity Cost Analysis: Capital Allocation and Generational Wealth

A critical component of aggressive investing is the rigorous application of opportunity cost analysis. This involves evaluating the long-term financial impact of every major expenditure. A prominent example within the FIRE community involves the choice between purchasing a luxury depreciating asset—such as a $120,000 vehicle—and allocating that same capital toward long-term investment vehicles like 529 college savings plans or custodial brokerage accounts.

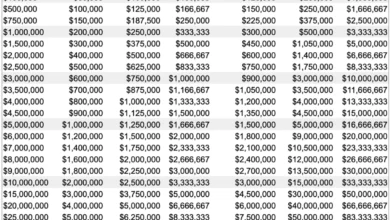

From a journalistic and financial perspective, the "true cost" of a $120,000 luxury car is not merely the purchase price. When factoring in a conservative 7.4% compound annual growth rate (CAGR), that $120,000, if invested in a diversified portfolio, could potentially grow to $350,000 over a 15-year horizon. In the context of rising education costs and a volatile labor market, the utility of $350,000 in liquid capital for a child’s future far outweighs the ephemeral utility of a high-end automobile.

Furthermore, the emergence of artificial intelligence (AI) has introduced a new layer of urgency to generational wealth planning. Economists suggest that AI could automate a significant percentage of entry-level professional roles within the next decade, potentially creating a "bleak future" for new college graduates. In this scenario, providing children with a substantial financial safety net acts as a form of "career insurance," allowing them to navigate a disrupted economy without the immediate pressure of debt or housing instability.

The Behavioral Economics of Workplace Resilience and Autonomy

Aggressive investing is often fueled by negative professional experiences, which serve as a catalyst for high savings rates. Workplace dynamics, particularly those involving micromanagement and cultural friction, frequently drive individuals to seek financial independence as a means of escape.

In a documented scenario typical of high-pressure corporate environments, an employee may face intense scrutiny and "microaggressions" from senior management. Such friction often stems from a lack of cultural competency or a fundamental misalignment of professional values. When a supervisor exhibits dismissive or derogatory behavior—mocking an employee’s heritage or demanding unrealistic response times—the affected individual faces a choice: endure the toxicity for decades or accelerate their path to freedom.

By increasing a savings rate from a standard 10-15% to an aggressive 50% or higher, an individual can effectively compress a 20-year retirement timeline into five to seven years. This requires a drastic re-evaluation of lifestyle expenses, including downsizing residences, transitioning from private to public education for children, and liquidating luxury goods. While these sacrifices are significant, the resulting "severance from the grind" provides a level of psychological relief that consumer goods cannot replicate. The goal is to reach a point where passive income—generated from rental properties, dividends, and interest—covers all living expenses, thereby rendering the behavior of a toxic employer irrelevant.

Social Dynamics and the Competitive Drive Toward Capital Accumulation

The pursuit of financial independence is also influenced by social comparison and the desire for long-term stability following personal upheavals, such as divorce. Sociological observations of the "newly single" demographic often reveal two divergent paths: "conspicuous consumption" and "intentional accumulation."

In the conspicuous consumption model, individuals attempt to project an image of success through high-interest leases on performance vehicles, luxury timepieces, and expensive travel. This "performance of wealth" often masks deep financial fragility. In contrast, the intentional accumulator adopts a "stealth wealth" approach. By maintaining a high savings rate and investing in tax-advantaged accounts like Roth IRAs and 401(k)s, this individual builds a robust balance sheet.

Over a five-to-ten-year period, the divergence between these two paths becomes stark. The individual who prioritizes investment typically achieves a net worth in the millions, allowing for a lifestyle dictated by choice rather than necessity. Meanwhile, the individual focused on appearances often remains trapped in a cycle of "living paycheck to paycheck," vulnerable to market shifts and personal financial crises. The "best revenge" in a social or personal rivalry is not the display of wealth, but the quiet confidence that comes from genuine financial autonomy.

Strategic Frameworks for Sustained Investment Discipline

To maintain the discipline required for aggressive investing, financial experts recommend the development of an "underdog narrative." This psychological tool involves identifying a personal grievance or a perceived disadvantage and using it as a motivational engine. Whether it is a fear of being replaced by AI, a desire to prove detractors wrong, or the need to provide for family members who lack financial literacy, these narratives help investors resist the "You Only Live Once" (YOLO) mentality that leads to impulsive spending.

Furthermore, the use of financial technology has become essential for tracking progress. Tools that aggregate net worth, monitor cash flow, and analyze investment fees provide the clarity necessary to make informed decisions. A professional financial review can often uncover "hidden" costs, such as high expense ratios in 401(k) plans or tax inefficiencies in brokerage accounts, which can shave percentage points off an investor’s long-term returns.

Broader Implications and Future Outlook

The shift toward aggressive investing and the FIRE movement has broader implications for the global economy and the future of work. As more individuals achieve financial independence at a younger age, the traditional "linear" career path is being replaced by "cyclical" or "portfolio" careers. This labor market flexibility allows individuals to pursue high-impact, low-pay roles in the non-profit sector or to start entrepreneurial ventures that they otherwise could not afford to risk.

However, the trend also highlights growing wealth inequality. Those with the ability to save 50% of their income are typically high earners in the technology, finance, or legal sectors. For the broader population, achieving such rates is a significant challenge. Nevertheless, the underlying principles of the movement—understanding opportunity cost, respecting market history, and prioritizing long-term security over short-term status—remain universally applicable.

In conclusion, aggressive investing is a rational response to an unpredictable world. By leveraging the 73% probability of annual market gains and maintaining a disciplined approach to capital allocation, individuals can insulate themselves from professional humiliation, economic shifts, and social volatility. The transition from a consumer-driven lifestyle to an investment-focused one is not merely a financial strategy; it is a fundamental shift in how one values time and freedom. As the data suggests, those who stay invested through the "bear" periods are the only ones positioned to fully harvest the "bull" markets of the future.

{kind=link}