Nearly two decades have passed since the 2008 Global Financial Crisis (GFC) reshaped the landscape of modern finance, yet the mechanics of that collapse remain a subject of intense debate and occasional misunderstanding. Despite the cultural footprint of the era, cemented by investigative journalism and cinematic retellings like The Big Short, a cloud of uncertainty persists regarding the specific triggers of systemic failure. Today, as the private credit market surges to a valuation exceeding $1.7 trillion, many investors and analysts are drawing parallels between the subprime mortgage era and contemporary lending practices. To determine whether these fears are justified, it is necessary to deconstruct the anatomy of the GFC and examine how the layering of leverage and derivatives transformed localized defaults into a global catastrophe.

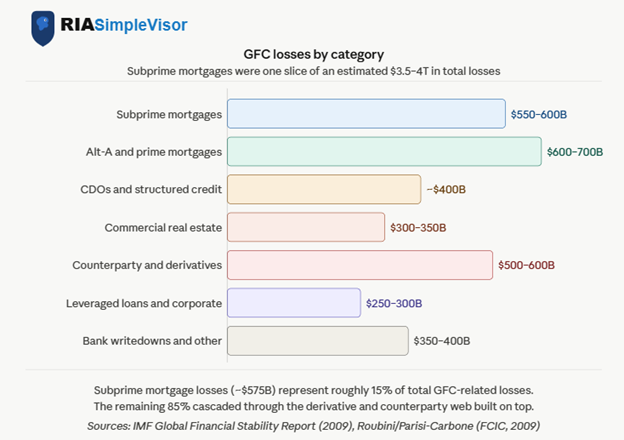

The fundamental misconception regarding the GFC is that subprime mortgage defaults alone were sufficient to topple the global banking system. In the years leading up to 2008, the outstanding volume of subprime loans reached approximately $1.3 trillion. While the loss rates on these loans eventually peaked at over 40%, resulting in a roughly $600 billion loss, this figure—while substantial—represented only a fraction of the total equity held by global financial institutions at the time. In a vacuum, a $600 billion loss should have been absorbable by the collective capital of the world’s largest banks and brokerages. The reason the crisis became an existential threat to the global economy was not the loans themselves, but the extraordinary web of leverage, complexity, and interconnected counterparty risks built atop them.

The Architecture of the Leverage Tree

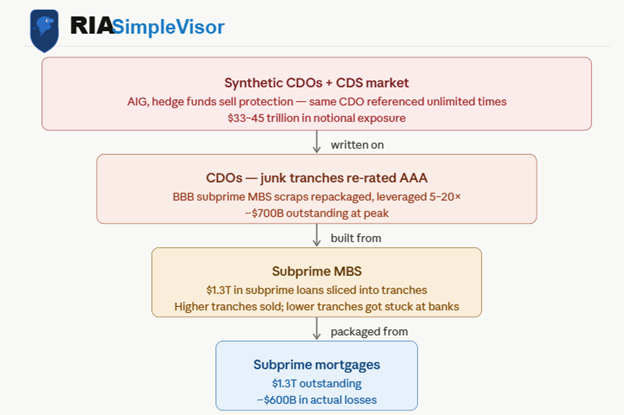

To understand the systemic risk of the 2000s, one must view the financial structure as a "leverage tree" where subprime loans served merely as the roots. The growth of this tree began when investment banks purchased individual subprime mortgages and packaged them into Mortgage-Backed Securities (MBS). These securities were structured into "tranches," which prioritized the distribution of cash flows. The AAA-rated tranches were the first to be paid and the last to absorb losses, making them attractive to conservative institutional investors such as pension funds and insurance companies. Conversely, the lower-rated "equity" or "mezzanine" tranches offered higher yields but were the first to be wiped out if homeowners defaulted.

By 2006, as housing prices began to stagnate and default rates ticked upward, the market for lower-rated MBS tranches evaporated. Banks and brokers found themselves holding billions of dollars in "toxic" debt that they could not sell at par value. Their solution was the creation of Collateralized Debt Obligations (CDOs). In this process, the unwanted, lower-rated tranches from various MBS were pooled together and repackaged into a new vehicle. Through the alchemy of financial engineering, rating agencies were persuaded to assign AAA ratings to the senior tranches of these CDOs, despite the fact that they were composed entirely of sub-investment-grade debt. This allowed banks to clear their balance sheets by selling junk-rated risks to investors who believed they were purchasing high-quality, safe assets.

The Multiplier Effect of Synthetic Exposure

The risk profile of the GFC was further compounded by the advent of synthetic exposure. When the demand for subprime-linked yields outstripped the supply of actual mortgages, Wall Street created synthetic CDOs. Unlike traditional CDOs, which were backed by the cash flows of physical mortgages, synthetic CDOs were derivatives backed by nothing more than a promise to pay based on the performance of a "reference" index of mortgages.

The synthetic market allowed for an unlimited multiplication of risk. If a single $200,000 mortgage in a mid-western suburb defaulted, it did not just impact the bank that issued the loan. Because that specific loan could be referenced in dozens of different synthetic contracts, a single default could trigger millions of dollars in losses across a global network of hedge funds, banks, and insurance companies. Estimates from the International Monetary Fund (IMF) and other regulatory bodies suggest that while there were $1.3 trillion in actual subprime loans, the synthetic credit exposure written against them ranged between $33 trillion and $45 trillion. This 30-to-1 ratio of derivative exposure to underlying assets explains why a localized housing downturn resulted in total global losses estimated between $3.5 trillion and $4 trillion.

Chronology of a Collapse: From Defaults to Systemic Freeze

The timeline of the GFC illustrates how a slow-burning fuse eventually reached a massive powder keg of leverage.

- Early 2007: Subprime mortgage lenders, such as New Century Financial, began filing for bankruptcy as early payment defaults spiked.

- Summer 2007: Two Bear Stearns hedge funds with heavy exposure to subprime CDOs collapsed, signaling that the "safe" AAA tranches were at risk.

- Late 2007 to Early 2008: Major banks began reporting multi-billion dollar write-downs. The "monoline" insurers, who provided credit default swap (CDS) protection, saw their credit ratings slashed.

- March 2008: Bear Stearns faced a liquidity crisis and was forced into a fire sale to JPMorgan Chase, backed by Federal Reserve guarantees.

- September 2008: The crisis reached its zenith. Lehman Brothers filed for bankruptcy after the government declined a bailout. Simultaneously, AIG, the world’s largest insurer and a massive issuer of synthetic protection, faced a total collapse and required an $85 billion federal rescue.

The failure of Lehman Brothers triggered a crisis of confidence that paralyzed the "boiler room" of the financial system: the overnight repo and Fed Funds markets. In these markets, banks lend to one another on a short-term basis to ensure daily liquidity. Once trust was lost, and institutions realized they did not know the extent of their counterparties’ exposure to toxic derivatives, they stopped lending entirely. The gears of global commerce seized, leading to the deepest recession since the 1930s.

Private Credit: A Different Structural Paradigm

As the private credit market—defined as non-bank corporate lending—has grown rapidly over the last decade, observers have raised alarms about its lack of transparency and potential for default. However, a structural analysis reveals significant differences between the current state of private credit and the 2008 subprime market.

Unlike the subprime era, where banks used extreme leverage to hold onto mortgage securities, private credit is largely funded by "closed-end" vehicles. These funds typically have long-term capital commitments from institutional investors, meaning they are not subject to the same "run-on-the-bank" dynamics that destroyed Lehman Brothers. Furthermore, the private credit market lacks the massive, interconnected web of synthetic derivatives that characterized the GFC. While a wave of corporate defaults in private credit would certainly result in losses for the specific pension funds and endowments invested in those funds, there is currently no evidence of a $40 trillion synthetic overlay that would transmit those losses into a systemic banking collapse.

Regulatory Responses and Market Implications

In response to the lessons of 2008, global regulators have implemented the Basel III framework, which requires banks to maintain significantly higher capital buffers and lower leverage ratios. The Federal Reserve now conducts annual "stress tests" to ensure that the largest financial institutions can withstand severe economic downturns without requiring taxpayer bailouts.

However, the growth of private credit represents a shift of risk from the regulated banking sector to the "shadow banking" sector. While this may protect the core banking system from a 2008-style contagion, it does not mean the economy is immune to the effects of credit contraction. If private credit funds experience high default rates, they will likely pull back on lending, which could starve small and medium-sized enterprises (SMEs) of the capital they need to operate. This would lead to a traditional economic slowdown or recession rather than a sudden, catastrophic financial implosion.

Conclusion and Broader Impact

The Global Financial Crisis serves as a permanent reminder that the danger in financial markets often lies not in the assets themselves, but in the complexity and leverage built around them. Subprime borrowers provided the match, but it was the $45 trillion derivative market and the fragility of the overnight lending markets that provided the fuel for the bonfire.

In the current environment, the anxieties surrounding private credit are understandable but must be viewed through the lens of structural reality. The private credit market lacks the "interconnectedness" that made subprime mortgages so deadly to the global system. While losses in private credit are likely as interest rates remain elevated, the absence of a massive synthetic multiplier suggests that the "leverage tree" of 2024 is far less precarious than the one that fell in 2008. The risk today is not necessarily a sudden collapse of the global financial architecture, but a protracted period of reduced liquidity and economic friction as the market reprices corporate risk for a new era.

{kind=link}