Oracle Stock’s AI Ascent and Its Cost: A Deep Dive into Fundamentals and Future Prospects

Oracle’s market capitalization, which flirted with the $1 trillion mark last year, has experienced a significant correction, shedding approximately 60% from its peak. Despite this substantial pullback, the company remains a focal point for investors anticipating long-term gains driven by the artificial intelligence (AI) revolution. The recent retreat of Oracle’s stock (ORCL) to a key technical support level has prompted a renewed examination of its underlying financial health and growth trajectory. This analysis delves into Oracle’s fundamental strengths, the costs associated with its AI ambitions, future growth projections, valuation metrics, and the inherent risks and rewards for investors.

Oracle operates as a global provider of enterprise IT products and services, with a strategic emphasis on cloud software, infrastructure, and database technologies. Its comprehensive suite of offerings includes crucial business applications such as Enterprise Resource Planning (ERP), Human Capital Management (HCM), and NetSuite, alongside robust infrastructure solutions, hardware, and consulting services. The company’s relevance in the burgeoning AI landscape stems from its role in furnishing the essential cloud infrastructure, sophisticated data platforms, and enterprise software that empower businesses to develop, deploy, and scale their AI applications effectively.

The Double-Edged Sword of AI-Driven Growth

Oracle has undeniably demonstrated significant AI-driven growth, underscored by its ability to secure substantial long-term contracts with prominent technology leaders. However, this aggressive expansion has not come without its financial implications. The pursuit of these ambitious growth initiatives has necessitated massive infrastructure investments, placing considerable pressure on the company’s debt levels and free cash flow. In essence, investors in Oracle may need to adopt a longer-term perspective, potentially enduring short-term financial headwinds in anticipation of sustained future returns.

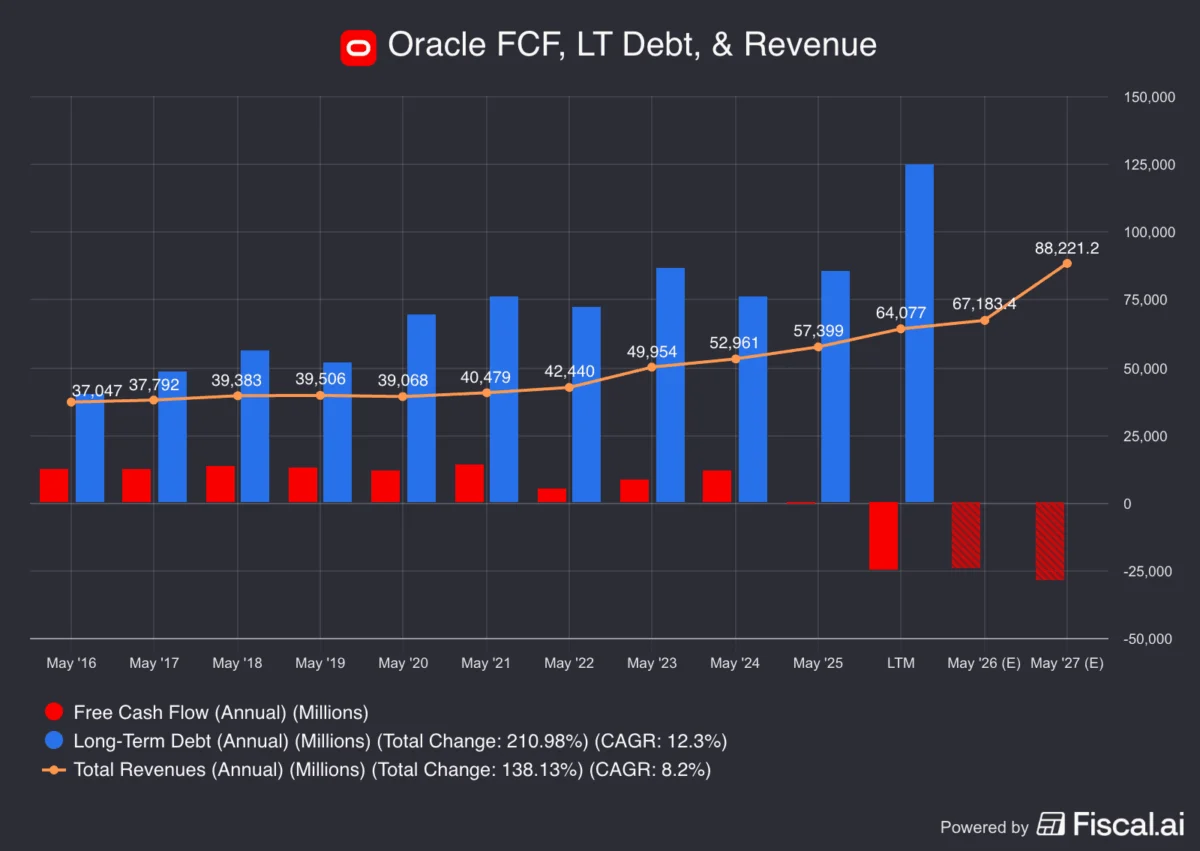

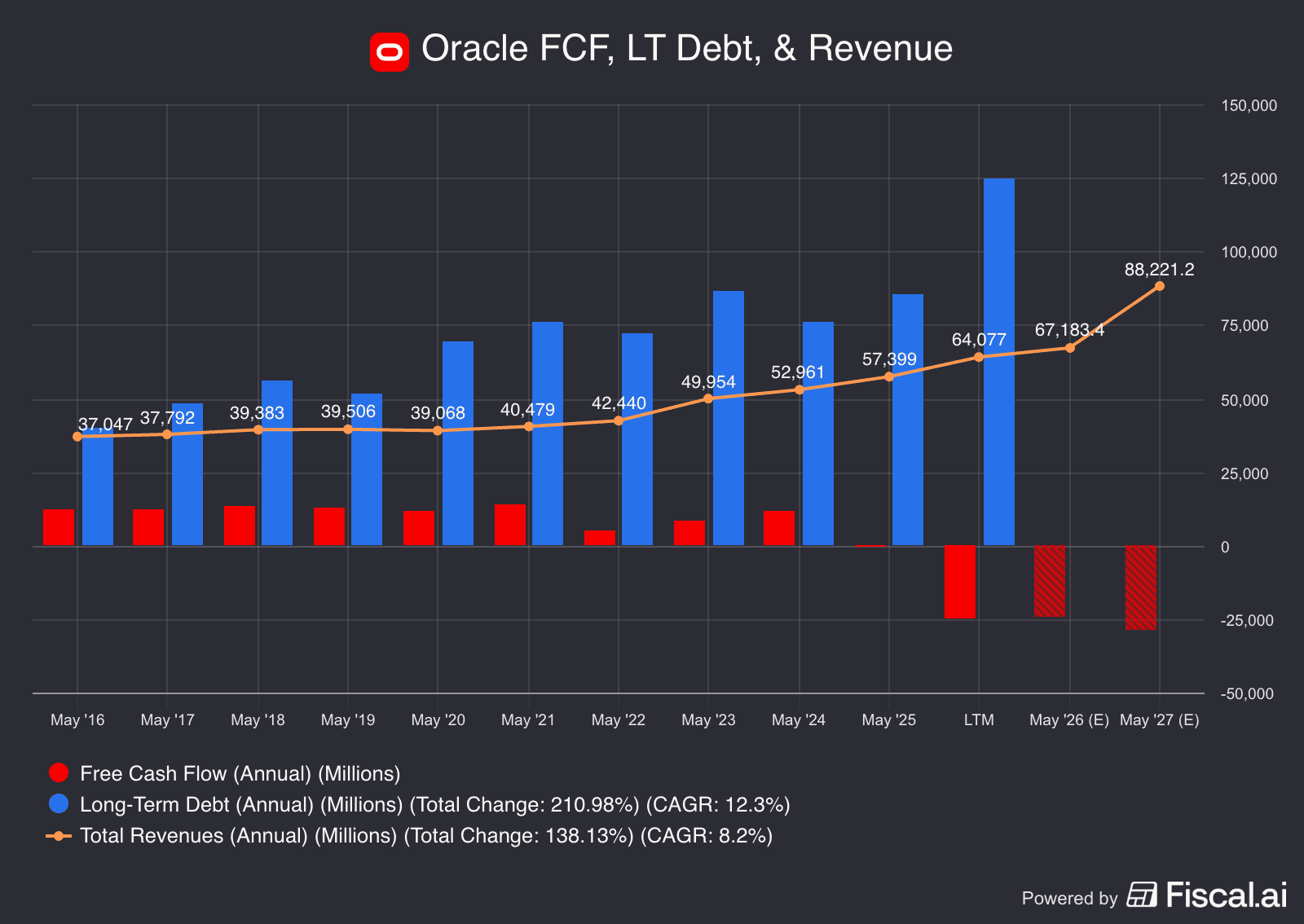

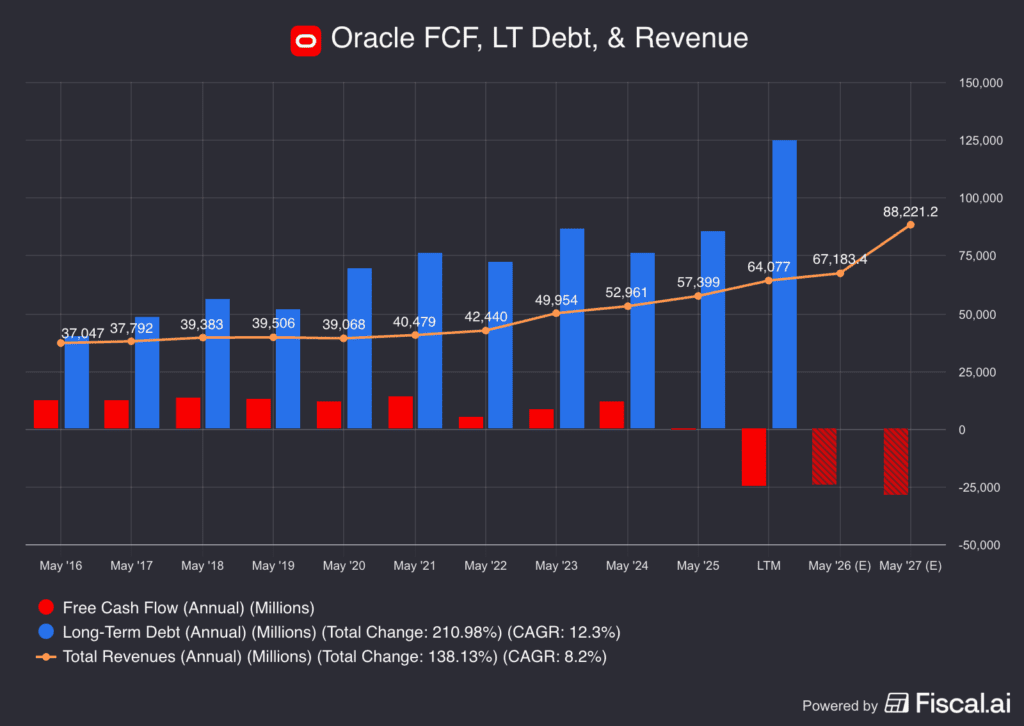

A closer examination of Oracle’s financial performance, as visualized in recent data, reveals a stark picture: free cash flow has turned negative, while long-term debt has escalated significantly. This trend is directly attributable to the substantial capital expenditures required to support the burgeoning demand for its cloud infrastructure and AI-related services. While revenue has shown an upward trajectory, it has been achieved at a considerable financial cost in the interim.

For instance, the period leading up to Oracle’s market cap surge likely saw substantial upfront investment in data centers, specialized hardware, and personnel to meet projected AI demand. These investments, while strategically vital for future market capture, impact immediate profitability and cash generation. The company’s fiscal year concludes in May, and the beginning of fiscal year 2027, commencing June 1st of the current year, will be a critical period for assessing the sustainability of its growth strategy and its impact on financial metrics.

Future Growth Projections and Analyst Outlook

Looking ahead, financial analysts are projecting a mixed but generally optimistic outlook for Oracle. According to data compiled by Bloomberg, projections indicate continued revenue growth. While specific figures are subject to revision, the consensus among analysts points towards a positive trajectory for Oracle’s top line.

Analysts currently maintain a consensus price target of approximately $245 for ORCL stock. This figure suggests a potential upside of around 38% from current trading levels. This optimistic outlook is likely predicated on the anticipated acceleration of AI adoption across industries and Oracle’s perceived ability to capitalize on this trend through its cloud and data infrastructure offerings. The market’s perception of Oracle as a key enabler of AI development is a significant driver of these future growth expectations.

The narrative of Oracle’s financial future is intricately linked to the broader technological landscape. The increasing reliance on cloud computing for data storage, processing, and AI model training creates a sustained demand for Oracle’s core competencies. Companies worldwide are investing heavily in their digital transformation journeys, with AI at the forefront, and Oracle is strategically positioned to benefit from this secular trend.

Valuation: A More Attractive Entry Point?

Despite concerns surrounding its balance sheet, Oracle’s earnings and revenue streams continue to exhibit a positive trend. The stock’s recent significant drawdown, coupled with rising earnings expectations, has rendered its valuation more appealing to some investors.

Analysis of forward price-to-earnings (P/E) ratios reveals a notable development. The forward P/E ratio for Oracle has recently receded to approximately 18 times earnings. This range, between 18x and 20x, has historically served as a support level for the stock in recent years. Concurrently, earnings estimates, while subject to some volatility, have trended upward. This combination of a lower P/E ratio and increasing earnings projections suggests that the market may be undervaluing Oracle’s future earnings potential relative to its current share price.

The valuation picture is further contextualized by the broader market environment. The technology sector, in particular, has experienced periods of significant re-evaluation, driven by concerns about inflation, interest rates, and the sustainability of high growth valuations. Oracle’s current valuation can be seen as a reflection of these broader market dynamics, as well as company-specific factors related to its investment in AI infrastructure.

Navigating the Risks in the AI Race

Oracle’s ambitious drive to scale its Cloud Infrastructure (OCI) segment to meet the escalating demand for AI capabilities is not without its inherent risks. These challenges are multifaceted and include significant execution hurdles related to the acquisition and deployment of data centers, securing adequate power supplies, sourcing advanced semiconductor chips, and managing the increasing capital intensity of these operations.

Furthermore, Oracle operates within a highly competitive cloud market, facing formidable rivals such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud. Any misstep in terms of service performance, pricing strategies, or customer adoption could have a material adverse impact on Oracle’s growth trajectory. The company’s ability to differentiate its offerings and secure market share against these established giants is a critical determinant of its future success.

The substantial AI-related spending, while necessary for growth, also poses a risk to Oracle’s free cash flow. If demand for AI services softens unexpectedly, or if projects take longer than anticipated to generate revenue, the company could face sustained pressure on its balance sheet. This could exacerbate existing debt levels and potentially reduce shareholder returns, particularly if the company needs to further increase its capital expenditures to maintain its competitive position.

Market-wide downturns, such as the recent sell-off experienced by software stocks, can also exert downward pressure on ORCL stock, irrespective of the company’s specific performance. These systemic risks are an inherent part of investing in the stock market and require careful consideration by investors. The interconnectedness of the technology sector means that a broad market correction can impact even fundamentally sound companies.

The Bottom Line: A Calculated Risk for Long-Term Investors

In conclusion, Oracle presents a compelling investment thesis characterized by AI-driven growth potential, improving earnings expectations, and a more attractive valuation following its recent stock price correction. These factors collectively support a long-term bullish outlook for the company. However, this opportunity is intrinsically linked to significant risks. Oracle must successfully navigate the complexities of heavy infrastructure investment, manage its escalating debt, and mitigate the impact of negative free cash flow. Moreover, the company must contend with intense competition from much larger cloud rivals.

For investors considering an allocation to ORCL, the potential for attractive upside exists, contingent upon effective management execution and sustained strong demand for AI services. Nevertheless, the path forward is likely to remain volatile, with the company’s ability to balance aggressive growth with financial prudence being a key determinant of its long-term success. The recent pullback, while concerning in the short term, may represent a strategic entry point for investors with a long-term horizon and a high tolerance for risk, provided they are confident in Oracle’s ability to execute its ambitious AI strategy.

Disclaimer:

The information provided herein is for informational purposes only and does not constitute financial advice. Investment decisions should be made based on individual financial circumstances and consultation with a qualified financial advisor. Market volatility can lead to rapid price changes, and some of the scenarios discussed may have already occurred.

{kind=link}