Federal Thrift Savings Plan Implements In-Plan Roth Conversions Marking a Significant Shift in Retirement Strategy for Federal Employees

The Federal Thrift Savings Plan (TSP), the primary retirement savings vehicle for approximately 7 million federal employees and members of the uniformed services, has officially launched in-plan Roth conversions as of 2026. This administrative milestone allows participants to transfer existing tax-deferred balances into Roth accounts within the plan, a feature that has been available in private-sector 401(k) plans for over a decade. While the move represents a modernization of the federal government’s $800 billion retirement system, the implementation includes specific regulatory nuances and structural limitations that distinguish it from private-sector counterparts.

Historical Evolution of the Thrift Savings Plan

The Thrift Savings Plan was established by the Federal Employees’ Retirement System Act of 1986. For decades, it was lauded as the "gold standard" of retirement plans due to its exceptionally low administrative fees and the unique G Fund, which offers government-backed security without the risk of principal loss. However, the TSP has historically been conservative in adopting features permitted by the Internal Revenue Service (IRS) for private-sector 401(k) plans.

The trajectory of Roth features within the TSP illustrates this deliberate pace. Although the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) first authorized Roth 401(k) contributions, the TSP did not implement this feature until May 2012. Similarly, while the Small Business Jobs Act of 2010 first allowed in-plan Roth conversions for 401(k) participants, it took sixteen years for the Federal Retirement Thrift Investment Board (FRTIB) to integrate this functionality into the TSP’s record-keeping system. This 2026 update follows a major technological overhaul of the TSP platform, intended to bring federal benefits in line with modern financial services.

Technical Specifications of In-Plan Conversions

Under the new 2026 guidelines, TSP participants are permitted to execute up to 26 in-plan Roth conversions per calendar year. This frequency aligns with bi-weekly pay periods, although the current system does not yet support the automation of these conversions. Participants must manually initiate each transaction through the TSP online portal or mobile application.

A critical logistical detail involves tax withholding. Unlike some private-sector plans that offer to withhold a percentage of the converted amount to cover the resulting tax liability, the TSP will not withhold taxes on these conversions. This requires participants to plan for increased tax obligations at the end of the fiscal year. Financial analysts suggest that participants manage this by either increasing their elective tax withholding from their federal salary or making quarterly estimated tax payments to the IRS to avoid underpayment penalties.

Structural Limitations and the Mega Backdoor Roth IRA

In the private sector, in-plan Roth conversions are frequently utilized as a component of the "Mega Backdoor Roth" strategy. This strategy allows high-income earners to contribute up to the total defined contribution limit—$69,000 as of 2024, adjusted for inflation by 2026—by making after-tax (non-Roth) contributions and then immediately converting them to a Roth subaccount.

However, the 2026 TSP rollout does not facilitate a "clean" Mega Backdoor process for two primary reasons:

Lack of Voluntary After-Tax Contributions

Most federal employees are restricted to two types of contributions: traditional tax-deferred and Roth. The TSP does not currently permit "voluntary after-tax" contributions, which are the engine of the Mega Backdoor strategy. The only exception applies to military members serving in designated combat zones, who can contribute tax-exempt pay that exceeds the standard elective deferral limits.

Absence of Isolated Subaccounts

Unlike modern 401(k) plans that maintain separate "buckets" for tax-deferred, Roth, and after-tax money, the TSP’s internal accounting remains more integrated. In a standard 401(k) that allows the Mega Backdoor, a participant can convert only the money in the after-tax subaccount. In the TSP, any conversion must be drawn from the tax-deferred balance. For military members with tax-exempt combat pay, the TSP applies a pro-rata rule. If a participant’s account consists of 80% tax-deferred money and 20% tax-exempt money, any conversion will be taxed proportionally. A $10,000 conversion would result in $8,000 of taxable income and $2,000 of tax-free conversion, preventing the surgical conversion of only tax-exempt funds.

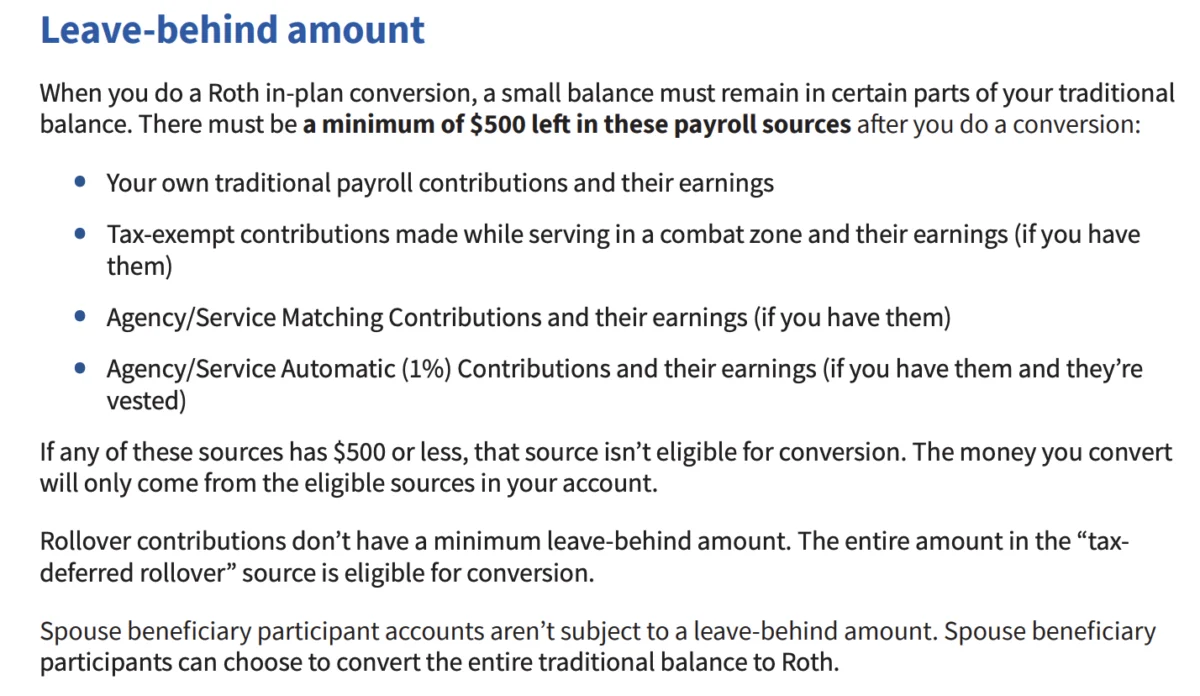

The "Leave Behind" Requirement and Administrative Rules

The FRTIB has introduced what is colloquially referred to as the "$500 Rule" or the "leave behind" amount. According to the 2026 TSP In-Plan Roth Conversion Handbook, participants are prohibited from converting their entire tax-deferred balance if it falls below a certain threshold, or they must maintain a minimum balance of $500 in the original source account. While the administrative justification for this rule has not been explicitly detailed by the Board, it is viewed by industry experts as a measure to prevent the accidental closure of subaccount records within the TSP’s legacy architecture.

Furthermore, the plan maintains strict rules regarding unvested funds. Specifically, the "Agency/Service Automatic (1%) Contribution" provided to employees under the Federal Employees’ Retirement System (FERS) or the Blended Retirement System (BRS) does not vest until an employee has completed two years of federal service. These unvested amounts are ineligible for Roth conversion until the vesting period is satisfied.

Conflicts with the Mutual Fund Window

In 2022, the TSP introduced a "mutual fund window," allowing participants to invest a portion of their savings in thousands of external mutual funds. However, assets held within this window are ineligible for direct Roth conversion. To convert these funds, a participant must first sell the mutual fund positions, transfer the cash back into the core TSP funds (the G, F, C, S, or I funds), execute the conversion, and then—if desired—re-purchase the mutual fund positions within the Roth side of the window. This multi-step process introduces market timing risks and administrative friction that may deter some participants from utilizing the window in conjunction with Roth strategies.

Strategic Implications for Federal Personnel

The introduction of in-plan conversions is particularly significant for military officers and federal employees who anticipate being in a higher tax bracket during retirement.

Military Physicians and High-Earners

For military doctors and senior officers, Roth conversions are often strategically advantageous. These individuals frequently transition into high-paying civilian roles after their service, or they remain in the military long enough to secure a pension. A federal pension, combined with Social Security, often fills the lower income tax brackets in retirement. By converting tax-deferred TSP funds to Roth during years where their marginal tax rate is lower than it will be in the future, these employees can lock in current tax rates and ensure tax-free withdrawals later in life.

The Impact of Tax-Exempt Combat Pay

For active-duty personnel who have accumulated significant tax-exempt balances while deployed, the in-plan conversion offers a rare opportunity to move those funds into a Roth environment where the growth—not just the principal—becomes tax-free. Despite the pro-rata complications, the ability to eventually shift these funds into a Roth account is a significant benefit that was previously unavailable without separating from service and rolling the funds into an external Roth IRA.

Broader Economic Context and Reactions

The shift toward Roth options in the federal sector mirrors a broader trend in American retirement policy. Legislative actions such as the SECURE Act and SECURE 2.0 have incentivized "Rothification" as a means of generating immediate federal tax revenue. By encouraging federal employees to convert tax-deferred balances now, the government realizes tax revenue in the current fiscal year that would otherwise have been deferred for decades.

Reactions from federal employee unions and advocacy groups have been cautiously optimistic. While many welcome the added flexibility, there are concerns regarding the complexity of the rules. "The TSP is a vital tool for the federal workforce, but these new conversion rules require a high level of financial literacy to navigate without incurring unexpected tax bills," noted a representative from a federal management association.

Conclusion and Future Outlook

The implementation of in-plan Roth conversions in 2026 marks a new era for the Thrift Savings Plan, transitioning it from a simplified, rigid system to a more complex, flexible investment vehicle. While the TSP still lags behind the most innovative private-sector 401(k) plans—particularly regarding the Mega Backdoor Roth and automated conversions—it remains one of the most efficient retirement plans in the world.

For the 7 million individuals who rely on the TSP, the bottom line is a new level of control over their tax destiny. As the FRTIB continues to refine the "Converge" system, participants may see further easing of the current restrictions, potentially including the automation of conversions or the creation of dedicated after-tax subaccounts. Until then, federal employees must weigh the immediate tax costs of conversion against the long-term benefits of tax-free growth in a Roth account.

{kind=link}