Foreign demand for the ballooning US Treasury debt is an increasingly important issue. But how much of that demand is actually “foreign?”

As the United States federal debt surpasses the staggering milestone of $39 trillion, the composition of the investor base holding this liability has become a focal point for global economists, policy analysts, and market participants. The mechanics of the Treasury market dictate that if the appetite for this debt wanes, yields must rise to attract new capital. These higher yields, in turn, escalate borrowing costs for the government, further widening the federal deficit in a self-reinforcing cycle. While historical focus has remained on sovereign entities like central banks, recent data suggests a fundamental shift in the nature of "foreign" demand, one that is increasingly driven by private financial entities and complex cross-border investment strategies rather than traditional state reserves.

Record Holdings and the Shift Toward Private Capital

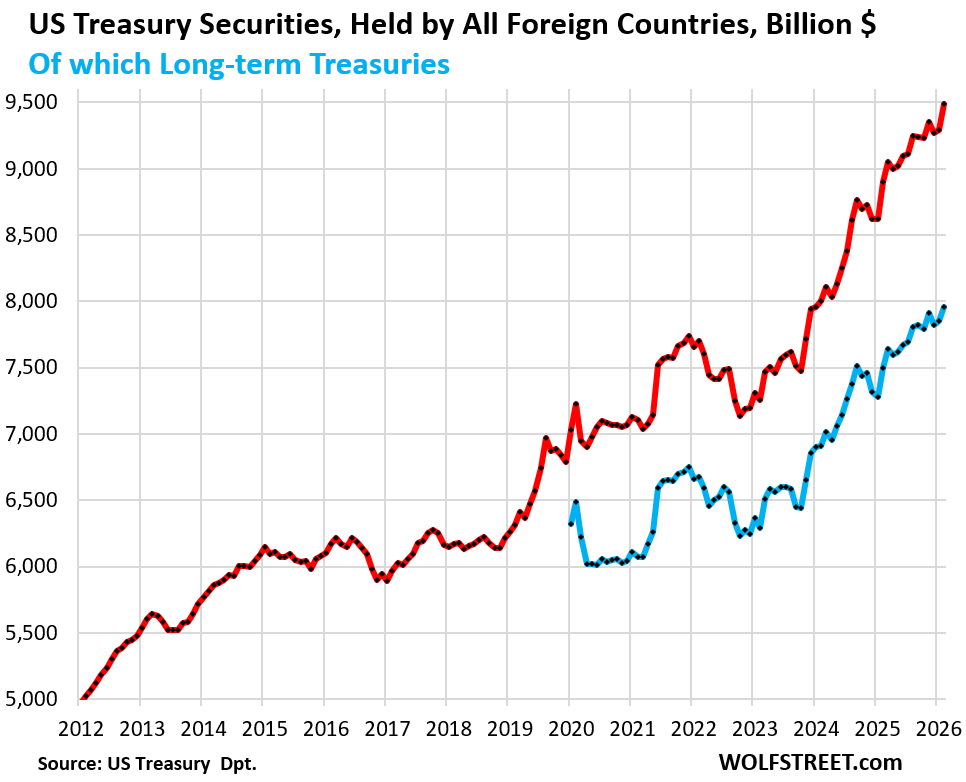

According to the latest Treasury Department data, total foreign holdings of US Treasury securities reached a record $9.49 trillion in February. This represents a significant influx of $198 billion during that month alone and a total increase of $587 billion over the preceding 12-month period. Of this nearly $9.5 trillion total, the vast majority—approximately $7.76 trillion, or 84%—is concentrated in long-term Treasury securities, with the remainder held in short-term Treasury bills.

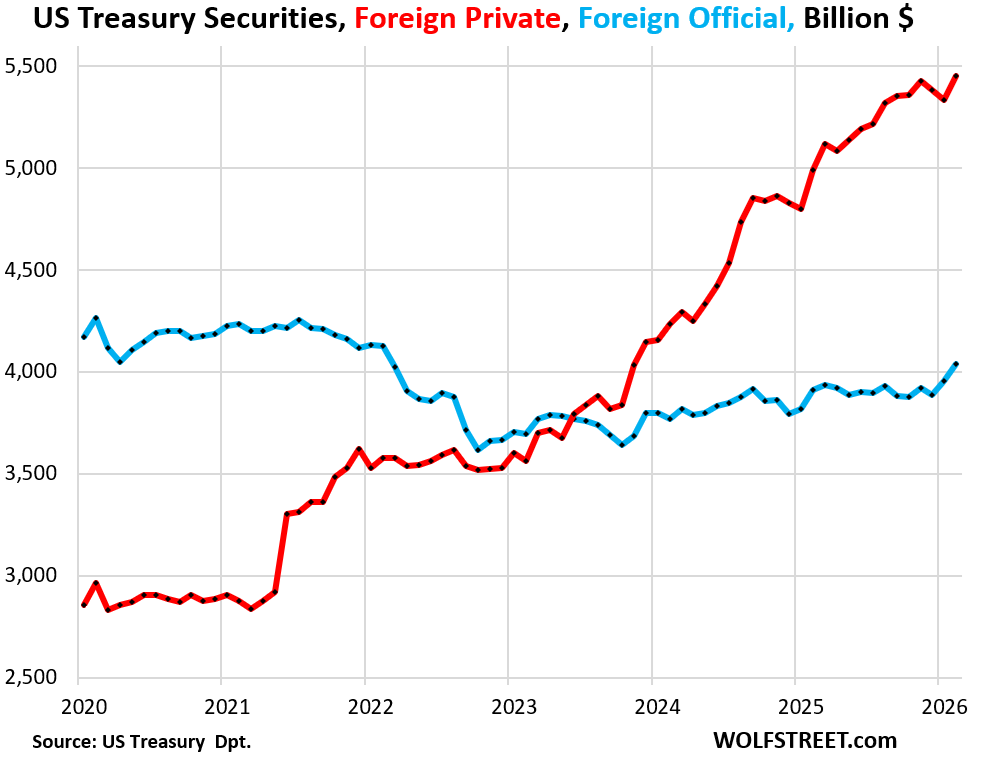

The primary catalyst behind this multi-year upward trajectory is the "private foreign" investor category. These holders increased their positions by $117 billion in February, bringing their total to a record $5.45 trillion. This category is a diverse mosaic of international finance, encompassing foreign bond funds, insurance companies, private corporations, and high-net-worth individuals. However, it also includes a significant "circular" component: US-managed hedge funds domiciled in jurisdictions like the Cayman Islands and American multinational corporations utilizing Irish subsidiaries for tax optimization.

In contrast, "foreign official" holders—the central banks and sovereign wealth funds that were once the dominant force in the Treasury market—have shown a more tempered appetite. While they added $81 billion in February to reach $4.04 trillion, their total holdings remain notably below the peaks seen several years ago. This divergence highlights a transition from a market supported by diplomatic and reserve-management mandates to one increasingly influenced by profit-seeking private capital and algorithmic trading.

The Shrinking and Expanding Share of Foreign Ownership

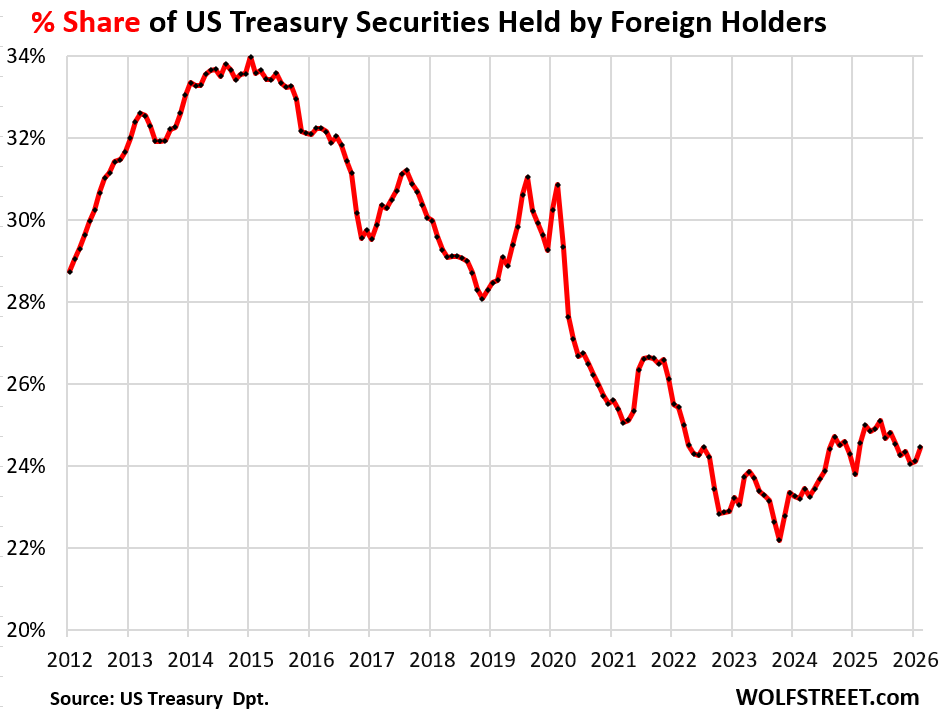

While the absolute dollar value of foreign-held debt is at an all-time high, the relative share of the total Treasury market held by foreign entities tells a more nuanced story. This share peaked at roughly 34% in 2015. Since then, the pace of US debt issuance has frequently outstripped foreign demand, leading to a decline in the foreign-held percentage, which bottomed out at 22% in October 2023.

A recovery in this share began in late 2023 and continued through early 2026. In February, the foreign share of the Treasury market rose to 24.5%. This fluctuation was influenced by the unique fiscal environment of 2025, particularly during the "Debt Ceiling" period from January through June. During those months, the total US debt remained static while foreign investors continued their steady accumulation, causing their relative share to rise. When the ceiling was lifted in July 2025, the Treasury Department issued a flood of new debt to replenish its cash accounts and fund ongoing deficits, which temporarily diluted the foreign share before it began its most recent climb.

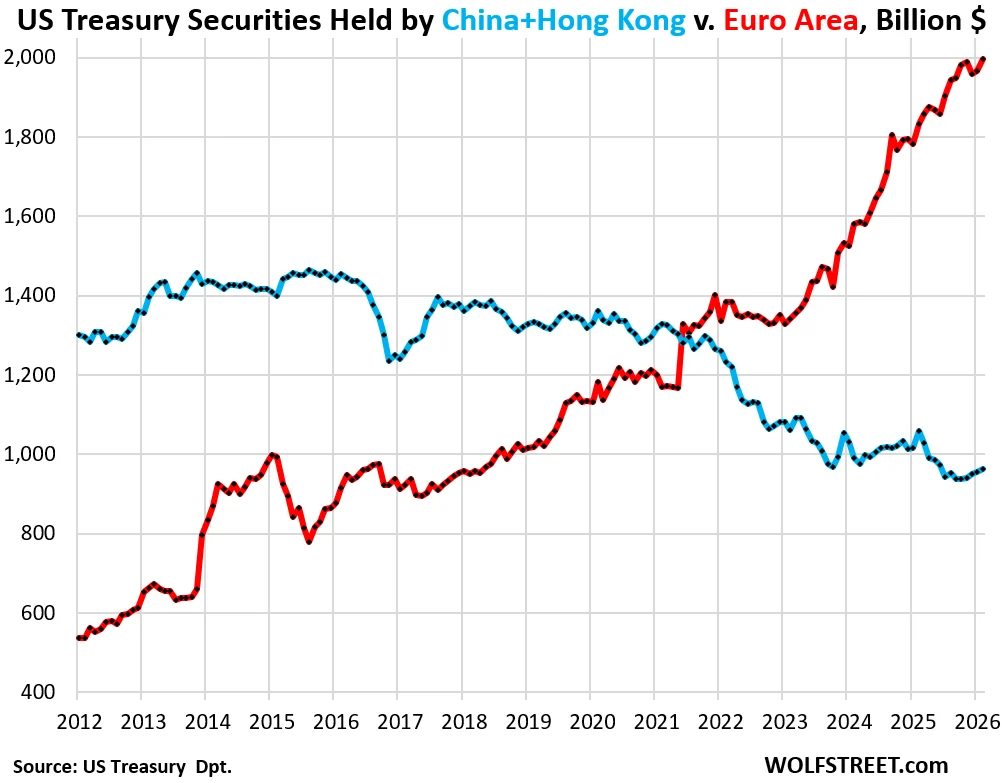

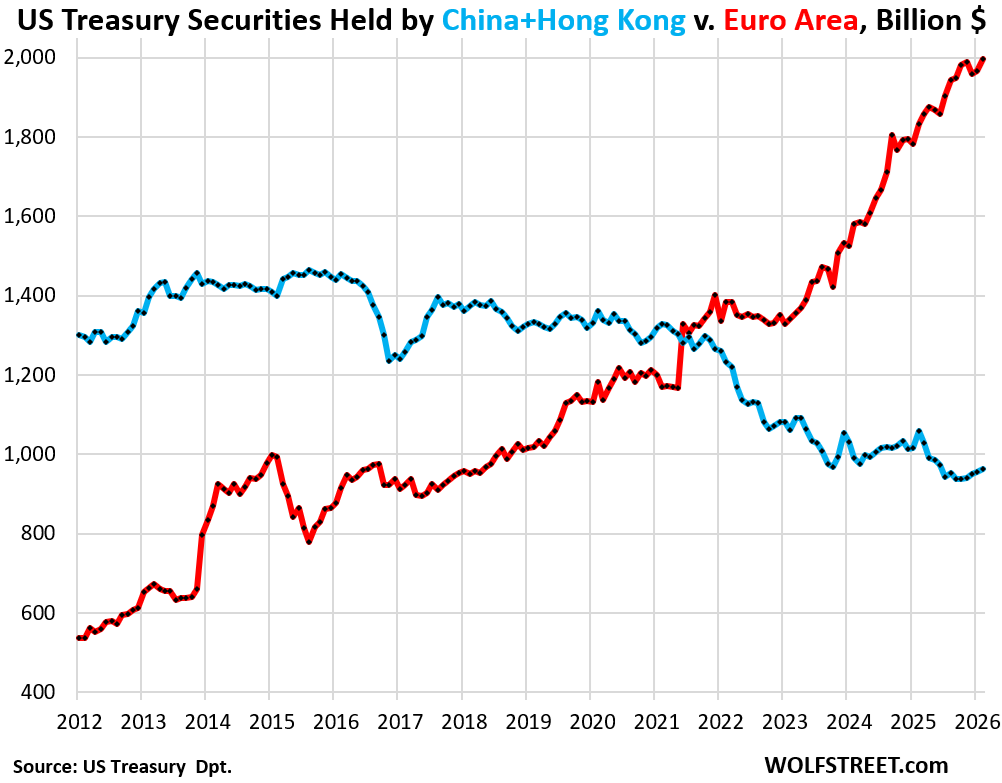

Geopolitical Realignment: The Euro Area vs. China

The geographic distribution of Treasury holdings is currently undergoing a historic realignment. For decades, China and Hong Kong were viewed as the essential pillars of foreign demand. However, these entities have been systematically reducing their exposure. In the 12 months ending in February, China and Hong Kong shed $96 billion in Treasuries, bringing their combined holdings to $962 billion. Over the last decade, China has cut its holdings by more than one-third, a move widely interpreted by analysts as a strategic effort to diversify reserves away from the US dollar amid escalating geopolitical tensions.

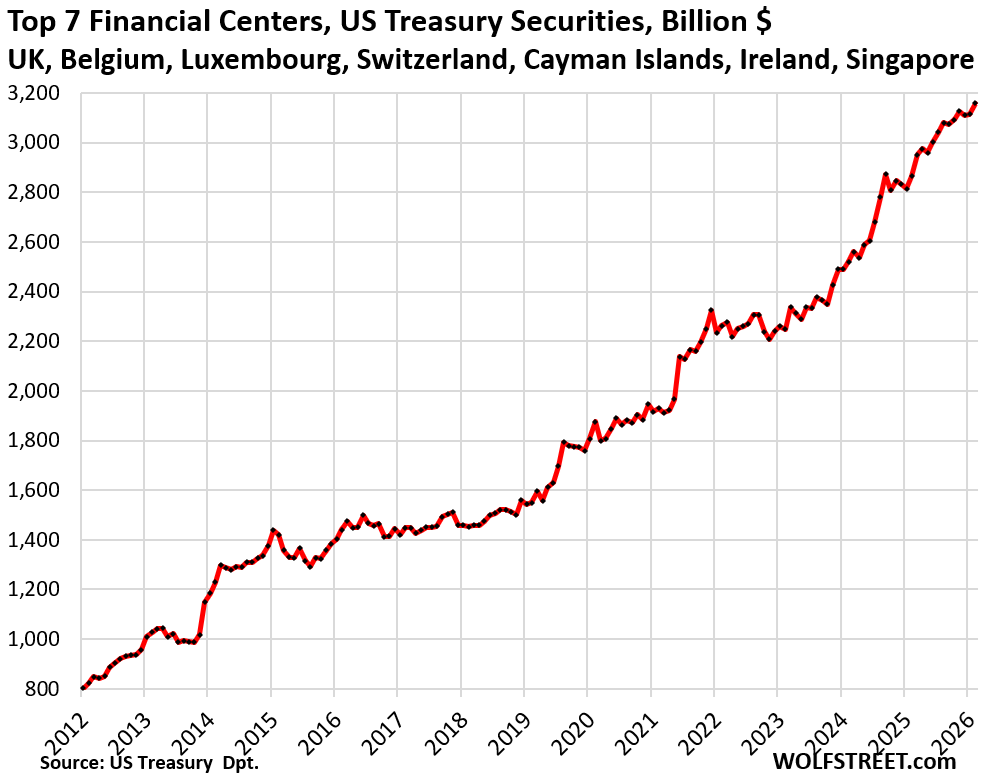

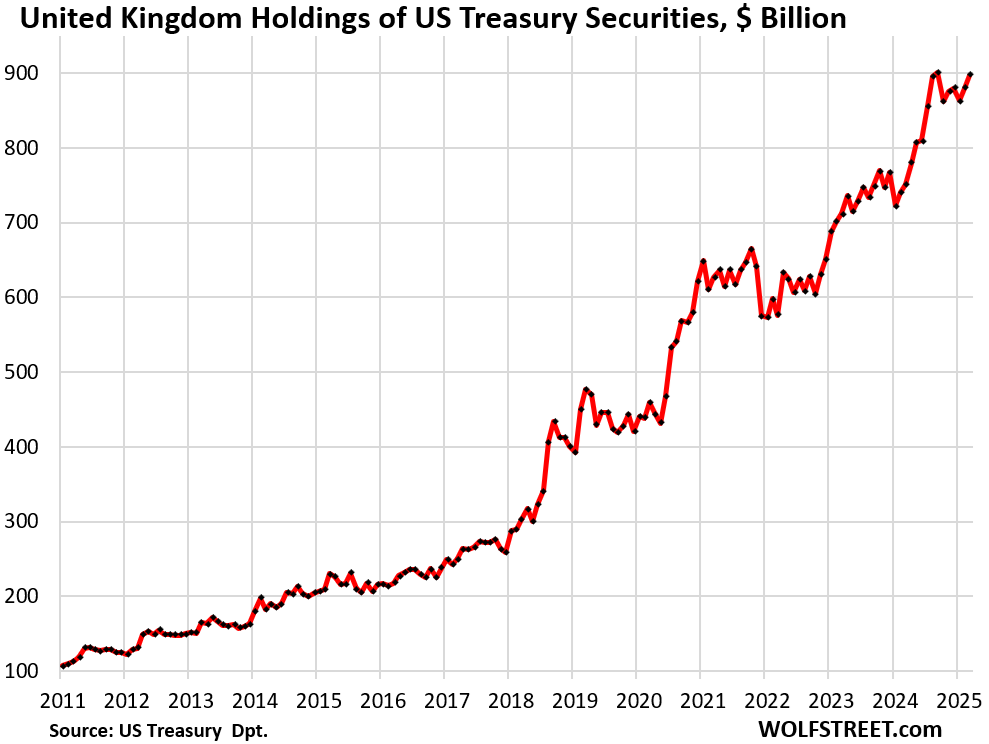

Conversely, the Euro Area has emerged as a voracious buyer. European holdings reached a record $2.0 trillion in February, following a $164 billion increase over 12 months. Interestingly, this demand is not driven by the region’s largest economy, Germany, which holds a relatively modest $109 billion. Instead, the accumulation is concentrated in global financial hubs: Luxembourg, Ireland, and Belgium. Together with France—whose banking sector functions as a global intermediary—these jurisdictions account for 82% of the Euro Area’s total Treasury holdings.

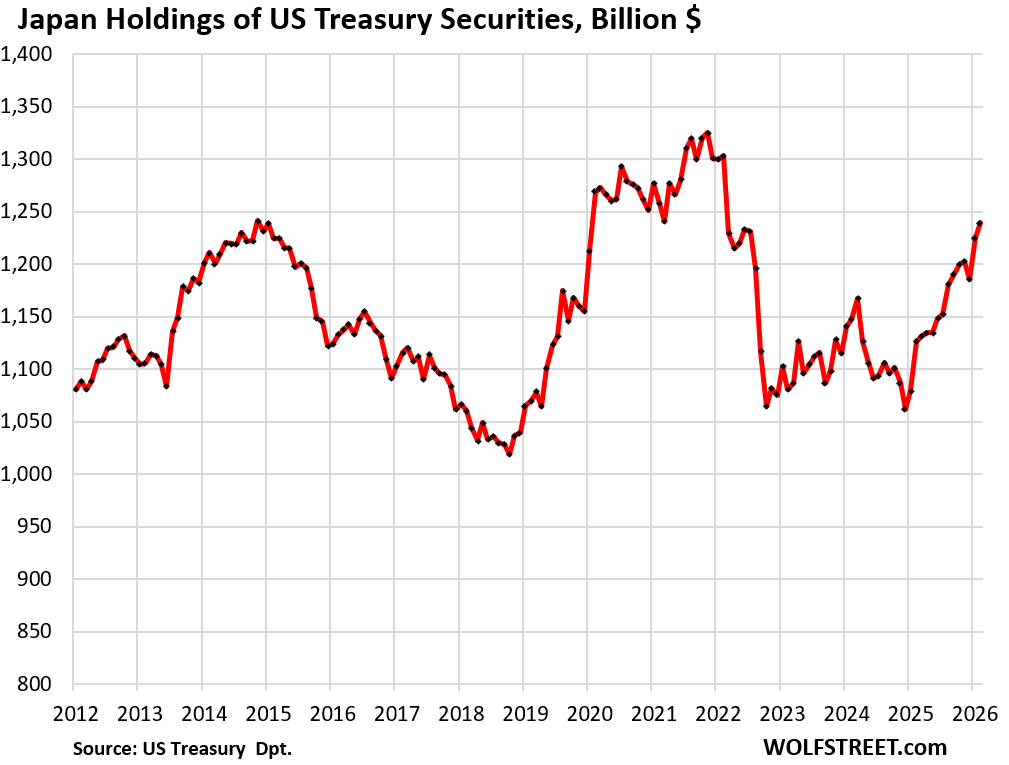

Japan remains the largest single-country holder of US debt, with $1.24 trillion in securities. Japan’s holdings have fluctuated between $1.0 trillion and $1.3 trillion for years. This stability is maintained despite periodic, aggressive sell-offs by the Japanese Ministry of Finance, which occasionally liquidates Treasury holdings to acquire Yen in an effort to stabilize its domestic currency against the dollar.

The Cayman Islands and the "Basis Trade" Phenomenon

One of the most significant revelations in recent Treasury analysis is the extent to which "foreign" demand is actually a reflection of US-based financial activity. The Cayman Islands officially hold $443 billion in Treasuries, but this figure is widely considered a massive undercount. A report from the Federal Reserve Board of Governors suggested that Treasury holdings by Cayman-domiciled US hedge funds were undercounted by as much as $1.4 trillion at the end of 2024.

This discrepancy arises from the "Basis Trade," a sophisticated arbitrage strategy employed by large US hedge funds. In this trade, funds buy Treasury securities (going long) while simultaneously selling Treasury futures (going short). Because these funds are domiciled in the Cayman Islands for regulatory and tax purposes, their massive long positions should be categorized as foreign. However, the Treasury International Capital (TIC) data often fails to capture these positions correctly, misclassifying them as domestic.

If the Cayman Islands’ holdings were adjusted to include these missing billions, their total would approach $2 trillion, making the territory the largest "foreign" holder of US debt. This realization fundamentally alters the understanding of market risk. The basis trade is highly leveraged; while it provides essential liquidity during stable periods, it can become a source of systemic instability during market volatility. This was evidenced in March 2020, when a breakdown in the basis trade forced the Federal Reserve to intervene with massive liquidity injections to prevent the Treasury market from seizing up.

Broad Implications for the US Fiscal Outlook

The increasing reliance on private, leveraged, and "synthetic" foreign demand has profound implications for the US government’s fiscal sustainability. Unlike central banks, which often hold Treasuries for long-term stability and reserve requirements, private investors and hedge funds are highly sensitive to price fluctuations and interest rate trajectories.

As the US government continues to run multi-trillion-dollar annual deficits, the need for a stable and diverse buyer base is paramount. The current trend suggests that while the world is not yet "abandoning" the dollar, the nature of the relationship has changed. Demand is no longer driven solely by the dollar’s status as a global reserve currency but by its utility in complex financial engineering and tax-advantaged corporate structures.

Market analysts warn that if yields continue to rise to accommodate the massive supply of new debt, the "interest expense" portion of the federal budget will eventually eclipse other major spending categories. By the end of 2025, interest payments on the debt had already begun to consume a record percentage of federal tax receipts. If the "foreign" demand—which we now know is largely composed of private financial centers and US-managed funds—wavers due to a shift in the risk-reward profile of the basis trade or a change in global tax laws, the US Treasury may find itself facing a significantly more expensive and volatile borrowing environment.

In summary, the record $9.49 trillion in foreign holdings is a testament to the continued depth of the US capital markets, but it masks a fragile reality. With China retreating and the "Basis Trade" masking the true origins of demand, the "foreign" label has become more of a geographic technicality than a reflection of genuine international confidence. As the debt continues to balloon toward $40 trillion and beyond, the transparency and stability of this investor base will remain the most critical variable in the global financial system.

{kind=link}