The international financial landscape underwent a historic transformation this week as major indices not only recovered from recent geopolitical shocks but surged to unprecedented heights. The S&P 500 concluded the week at a record-breaking 7,125.06, marking a 13.1% rally from its March lows in less than three weeks. This performance represents one of the most aggressive V-shaped recoveries in the post-Global Financial Crisis era, propelled by a convergence of diplomatic breakthroughs in the Middle East, robust corporate earnings, and a massive reversal in institutional positioning. The Nasdaq Composite similarly made history, logging its 13th consecutive daily gain—its longest winning streak since 2009—while the Russell 2000 reached a new all-time high, signaling that the rally has moved beyond a narrow technology-led squeeze into a broad-based market expansion.

Geopolitical Breakthrough: The Reopening of the Strait of Hormuz

The primary catalyst for this week’s surge was a dramatic de-escalation of tensions between the United States and Iran. Following weeks of volatility that saw global oil prices skyrocket, a report from Axios on Friday confirmed that the two nations are negotiating a three-page memorandum of understanding (MOU). This framework reportedly includes the release of $20 billion in frozen Iranian funds in exchange for Tehran surrendering its enriched uranium stockpile and agreeing to a moratorium on further nuclear enrichment.

The immediate market reaction was triggered by a social media post from Iran’s foreign minister confirming that the Strait of Hormuz—a vital artery for global energy transit—was once again "completely open." This development effectively neutralized the "stagflation" narrative that had gripped markets since late February. WTI crude oil plunged by more than 11% following the news, and Brent crude dropped 9.1% to settle near $94 per barrel. By removing the primary driver of energy-driven inflation, the reopening of the Strait has fundamentally altered the Federal Reserve’s potential path, reopening the door for interest rate cuts later this year as the March Consumer Price Index (CPI) is now expected to be the final "ugly" print of this cycle.

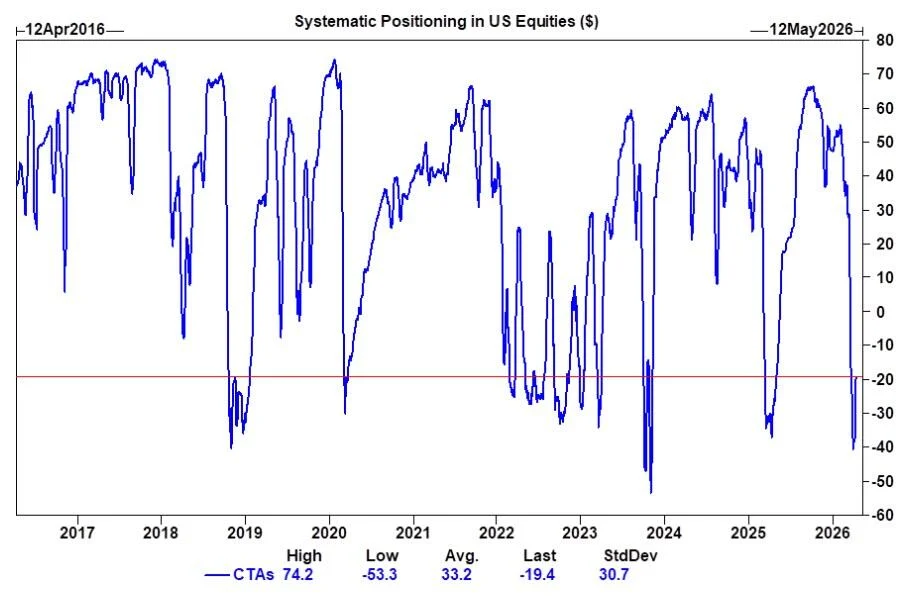

Institutional Mechanics: The $156 Billion CTA Pivot

While sentiment was driven by headlines, the rally’s velocity was fueled by the mechanical behavior of systematic investors. Commodity Trading Advisors (CTAs), which are programmatic trend-following funds, had aggressively shorted the market as it hit lows on March 29. As the market reversed, these funds were forced into a "violent" covering cycle. Data suggests that CTAs purchased an estimated $86 billion in equities last week alone to cover short positions and flip to long exposure.

Market analysts point out that this is not discretionary optimism but rather forced momentum-chasing. According to current positioning data, systematic funds have an additional $70 billion in programmatic buying to deploy over the next five trading sessions. This provides a significant mechanical tailwind for the market heading into next week, creating a floor for prices even if geopolitical progress momentarily stalls. Hedge fund gross exposure remains near all-time highs of 307%, suggesting that while the "coiled spring" has partially released, the market remains highly sensitive to further positive developments.

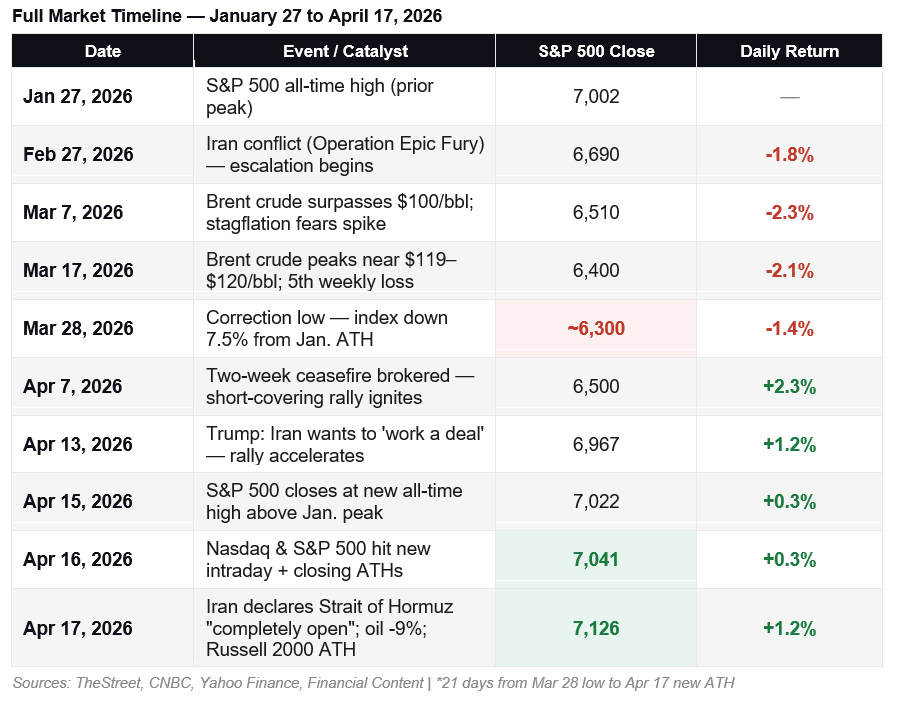

A Chronology of the Recovery: From War to Record Highs

To understand the magnitude of the current rally, one must look at the timeline of the preceding two months. The market reached a previous peak of 7,002 on January 27 before entering an eight-week decline triggered by the launch of Operation Epic Fury in late February. This geopolitical shock caused Brent crude to surge from $72 toward $120, leading major investment banks to raise recession probabilities from 25% to 50%.

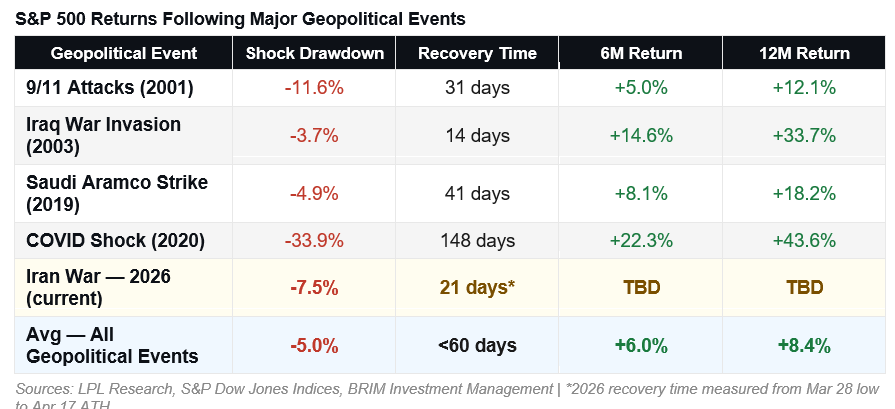

The market suffered five consecutive weekly losses, bottoming near 6,300 in late March. The tide began to turn on April 7 with the first credible reports of a ceasefire. The recovery accelerated on April 13 following comments from the Trump administration indicating a willingness to reach a permanent deal with Tehran. The culmination occurred this Friday, April 17, with the formal announcement of the Strait’s reopening. The speed of this "round-trip" to new highs—just 21 days—is historically rare, comparable to the post-Iraq War recovery of 2003 and the initial 2020 post-COVID bounce.

Earnings Season: Fundamental Support Amidst Cautionary Notes

The rally was further validated by a strong start to the first-quarter earnings season. JPMorgan Chase exceeded analyst expectations across the board, reporting earnings per share (EPS) of $5.45 on revenue of $50.54 billion. However, CEO Jamie Dimon tempered the market’s enthusiasm by lowering net interest income guidance and citing an "increasingly complex set of risks" in the global macro environment.

Other major financial institutions, including Citigroup and BlackRock, also topped estimates. In contrast, Goldman Sachs saw its stock decline by nearly 2% after disappointing results in its Fixed Income, Currencies, and Commodities (FICC) division, despite record equities trading. Outside the banking sector, Netflix reported a beat on both top and bottom lines, yet its stock faced pressure after guidance failed to meet high investor expectations. Overall, 80% of S&P 500 companies that have reported thus far have topped EPS estimates by an average of 15.7%, supporting FactSet’s projection for a sixth consecutive quarter of double-digit earnings growth.

Market Internals and Sector Rotation

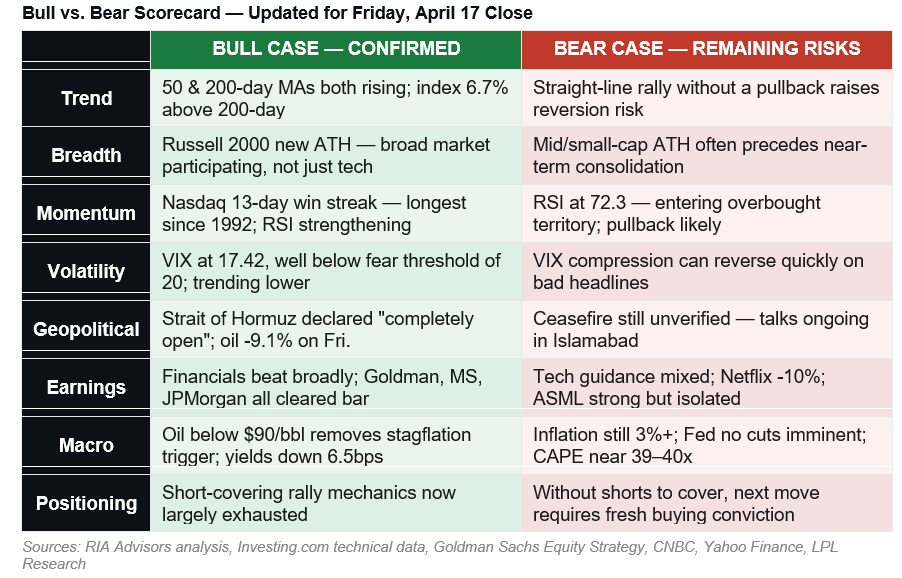

A critical distinction in this rally is the improvement in market breadth. Two weeks ago, only 27.6% of S&P 500 constituents were trading above their 50-day moving average. As of Friday’s close, that figure has surged to 71%, well above the 50% threshold that typically separates a "dead cat bounce" from a genuine trend reversal.

The rotation of capital has also shifted from "wartime beneficiaries" to "recovery leaders." Energy, which outperformed during the crisis, has given back its premium. Meanwhile, Technology and Consumer Discretionary sectors have led the charge. The travel and leisure sub-sectors saw a significant boost on Friday, with cruise lines such as Royal Caribbean and Carnival surging over 9% as investors bet on a return to global normalcy. Retail participation has also rebounded, rising from the 10th to the 55th percentile according to JPMorgan flow data, indicating that individual investors are beginning to overcome their previous hesitation.

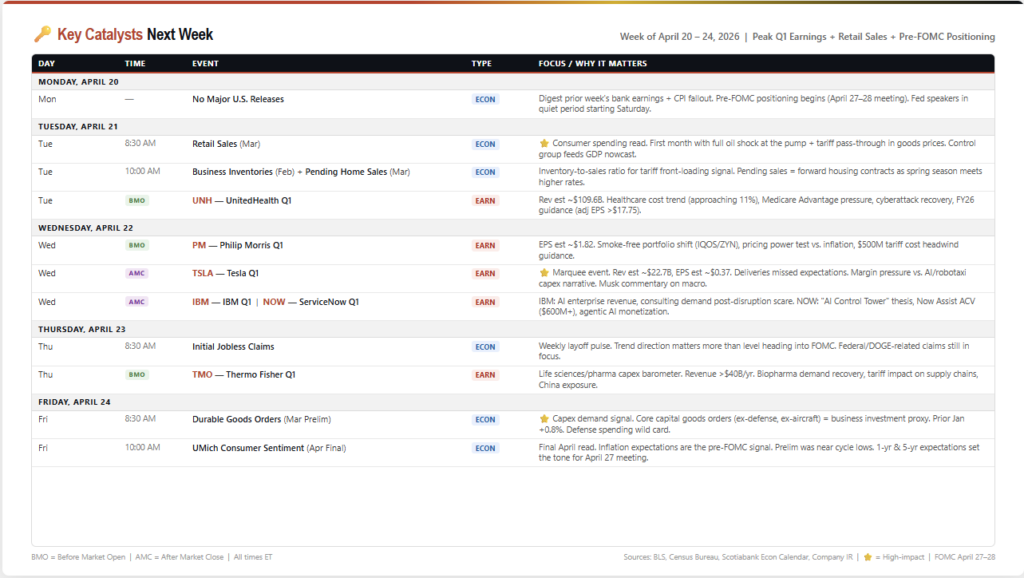

Looking Ahead: Key Catalysts for Next Week

The focus now shifts from banking results to the consumer and "Big Tech." Tuesday’s March Retail Sales report will be the first economic anchor, providing a clear picture of how much the recent oil price spike and tariff concerns impacted consumer spending. If the data shows a contraction, it may strengthen the narrative of an economic slowdown heading into the Federal Open Market Committee (FOMC) meeting on April 27–28.

Wednesday will be the week’s marquee earnings day, with Tesla reporting after the close. Following a miss in first-quarter deliveries, investors are looking for clarity on Tesla’s margins and its aggressive pivot toward AI and robotaxi infrastructure. IBM and ServiceNow will also report, serving as bellwethers for enterprise AI spending. The week will conclude with the University of Michigan Consumer Sentiment reading. Markets will be particularly sensitive to five-year inflation expectations; a reading above 3% could prompt a hawkish stance from the Fed, while a decline would likely solidify the bull case for rate cuts.

Technical Analysis and Risk Management

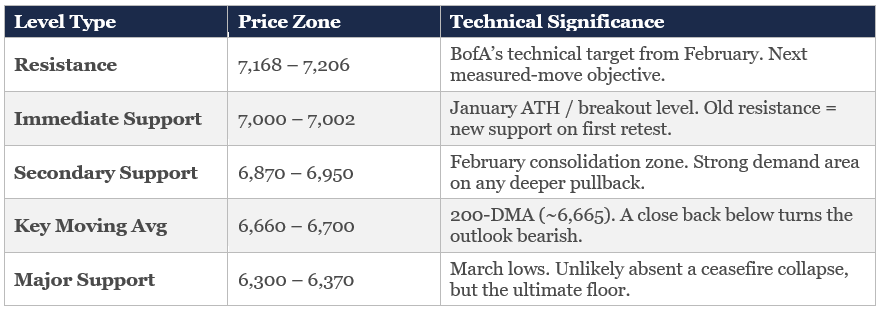

Despite the bullish momentum, technical indicators suggest the market is becoming overextended. The Relative Strength Index (RSI) is currently pushing above 70, a level traditionally associated with overbought conditions. Furthermore, the S&P 500 is trading roughly 7% above its 200-day moving average (approximately 6,683). Historical data suggests that 13-day winning streaks in the Nasdaq are frequently followed by 2% to 5% pullbacks within the subsequent two weeks.

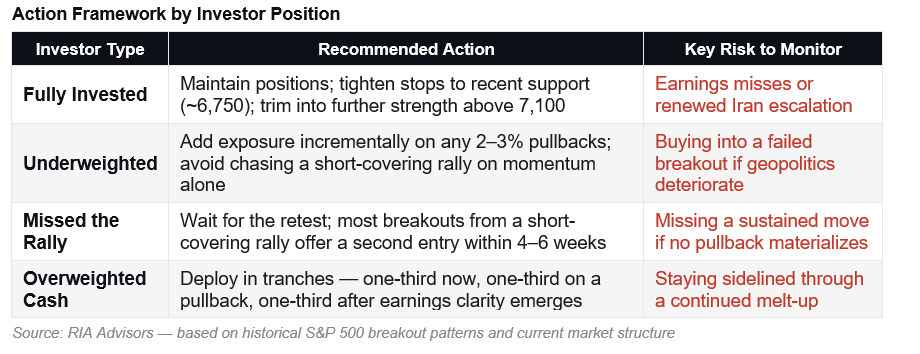

Analysts suggest that while the long-term trend has turned positive, chasing the current highs may carry significant short-term risk. A healthy pullback to the 7,000 level—where old resistance is expected to become new support—would likely provide a more attractive entry point for investors who missed the initial move. The 6,870–6,950 zone remains a secondary area of consolidation that should attract strong buying interest.

Broader Implications and Final Verdict

The events of this week suggest a fundamental shift in the market regime. The transition from a mechanical short-covering rally to a structural bull market is typically marked by four conditions: a return to all-time highs, a collapse in the VIX (which fell from 31 to 17 this week), a reversal of the "fear" catalyst (the Strait of Hormuz), and a broadening of sector participation. With all four conditions now met, the "bear case" has largely been relegated to concerns over valuation and short-term overbought conditions rather than structural weakness.

However, the fragility of the US-Iran MOU remains a primary tailwind risk. Any violation of the enrichment moratorium or a sudden escalation in rhetoric could quickly unwind the progress of the last three weeks. For now, the "inflation math" has shifted in favor of the bulls, and the "easy money" phase of the recovery has concluded. Investors are advised to maintain discipline, rebalance risk where sectors have become overextended, and prepare for a more calculated phase of the bull market as the FOMC meeting approaches.

{kind=link}