Eli Lilly’s Dominance in Pharmaceuticals: A Deep Dive into Growth, Innovation, and Market Valuation

Eli Lilly and Company, a titan in the global pharmaceutical landscape, commands a market capitalization of approximately $1.1 trillion. The company’s extensive research and development efforts span critical therapeutic areas including diabetes, obesity, oncology, immunology, and neuroscience. However, its current trajectory is overwhelmingly defined by the remarkable success of Mounjaro and Zepbound, its blockbuster treatments for diabetes and weight management, respectively. These medications have ascended to become the primary engines of Eli Lilly’s considerable growth, further bolstered by a portfolio of established products such as Verzenio, Jardiance, Taltz, and the Alzheimer’s treatment Kisunla. The company’s forward-looking strategy is heavily invested in the development of next-generation obesity drugs, with retatrutide at the forefront, alongside initiatives to explore tirzepatide’s efficacy in a wider range of metabolic and cardiovascular conditions. Furthermore, Eli Lilly is actively pursuing novel therapeutic approaches for Alzheimer’s disease, cancer, and various inflammatory disorders, underscoring its commitment to addressing unmet medical needs across a broad spectrum of human health.

A Trajectory of Sustained Revenue Growth and Evolving Profitability

Eli Lilly has demonstrated a consistent upward trend in revenue, achieving eight consecutive years of expansion, with projections indicating a continuation of this growth. While revenue has been a story of steady ascent, the company’s profitability has exhibited a more dynamic pattern. Sharp increases in profit have, at times, been succeeded by periods of stabilization or modest decline. This ebb and flow in profit generation is a common characteristic within the pharmaceutical industry, often influenced by the timing of new drug launches, the cost of research and development, and competitive pressures.

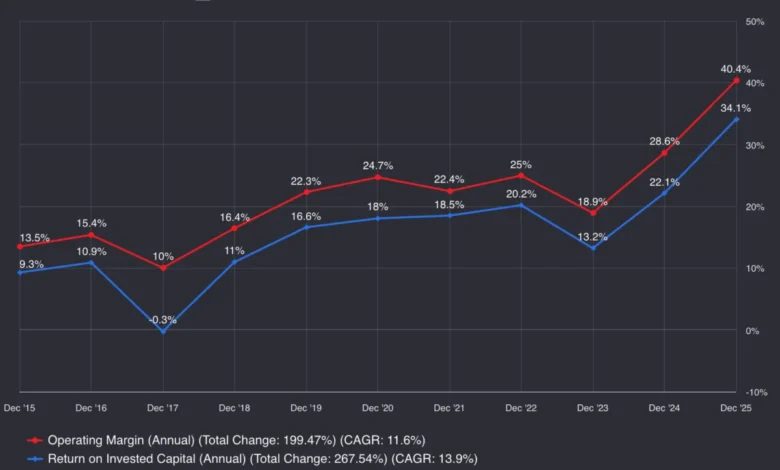

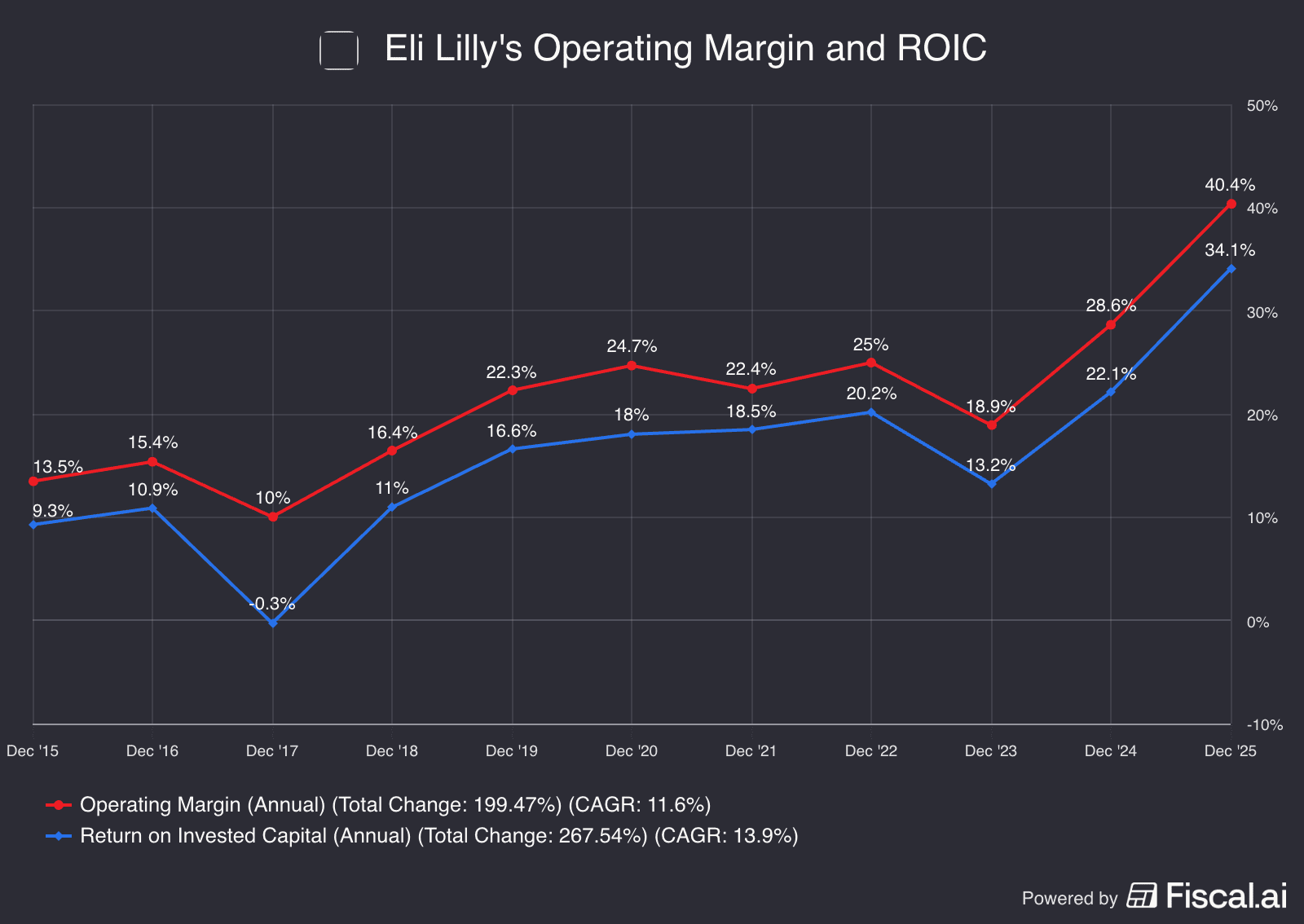

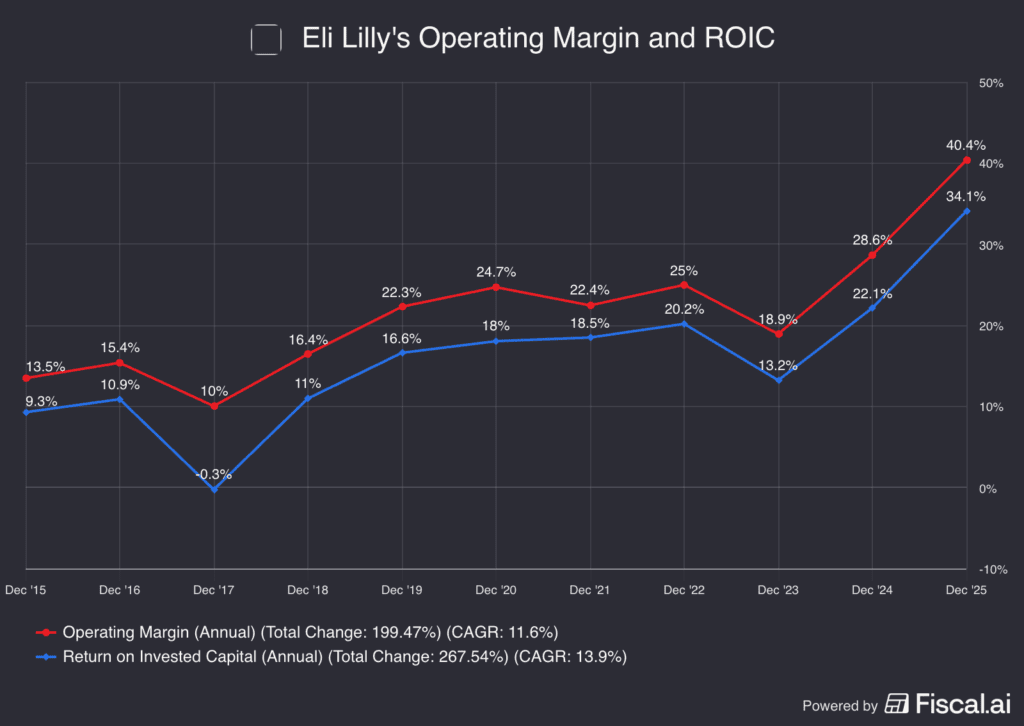

To provide a more granular understanding of Eli Lilly’s financial health and operational efficiency, an examination of its operating margins and Return on Invested Capital (ROIC) is crucial. Operating margins reflect a company’s profitability from its core business operations, while ROIC measures how effectively a company generates profits from the capital it has invested. Recent trends indicate a strengthening of Eli Lilly’s margin profile over the past few years, suggesting improved operational efficiency and pricing power. Concurrently, the company has witnessed an enhancement in its returns on investment, signifying a more productive deployment of its capital resources. This dual improvement in profitability metrics paints a picture of a company that is not only growing its top line but also becoming more adept at converting its investments into profits.

Future Growth Projections: Analyst Optimism and Market Potential

The outlook for Eli Lilly’s future financial performance remains decidedly optimistic, as reflected in the upward revisions of earnings estimates. Over the past three and six months, analyst consensus for earnings per share has been revised upwards by 4.3% and 7.1%, respectively. This positive recalibration by financial analysts underscores a growing confidence in the company’s ability to sustain its impressive revenue and earnings growth trajectory.

According to data compiled by Bloomberg, analysts project continued expansion for Eli Lilly. While specific numerical projections can fluctuate, the general consensus points towards robust year-over-year growth driven by the continued success of its key products and the potential of its pipeline. The company’s strong performance in recent years, characterized by increasing revenues and improving profitability, has fostered an environment where analysts anticipate this momentum to persist.

This optimism is further translated into market expectations for Eli Lilly’s stock. Analysts currently maintain a consensus price target of approximately $1345 for LLY stock. This target suggests an implied upside of around 14% from its current trading price. Such a target implies that the market, as represented by analyst consensus, believes the stock has further room to appreciate, driven by the company’s fundamental strengths and future growth prospects.

Diving Deeper into Valuation: A Complex but Promising Picture

Eli Lilly’s current valuation presents a nuanced and compelling investment narrative. Its forward earnings multiple, a key metric used to assess a company’s stock price relative to its expected future earnings, remains significantly below the peaks it reached during the zenith of the GLP-1 enthusiasm. During that period, Eli Lilly and its peers, most notably Novo Nordisk, experienced an unprecedented surge in stock valuations, reaching historic highs. This past exuberance has since moderated, but the current valuation range for Eli Lilly is still in a state of formation.

Over the past year, the stock has consistently found support in the range of 23 to 25 times forward earnings. This price zone, which previously acted as a resistance level, now appears to be a foundational support for the stock. The upper bounds of its valuation, however, remain less clearly defined, indicating potential for further appreciation. Earlier in the year, Eli Lilly’s shares encountered resistance and stalled as its valuation multiple approached 35 times forward earnings, suggesting a ceiling that the market perceived at that time.

What makes the current valuation particularly interesting is the confluence of strong underlying fundamentals with this more tempered, yet still robust, valuation. Eli Lilly has demonstrably improved its profit margins, achieved higher ROIC, and is experiencing solid revenue and earnings growth. The fact that the stock has recently reached record highs, even as its valuation multiple has approached its 2026 low, is a testament to the rapid growth of its earnings – the "E" in the Price-to-Earnings (P/E) ratio. This signifies that the company’s profitability is outpacing the rate at which its valuation multiple is expanding, a healthy sign for investors.

The accompanying chart provides a visual representation of this valuation dynamic, illustrating how the stock’s price has evolved in relation to its forward earnings multiple. This data, sourced from Bloomberg and eToro and dated July 16, 2026, highlights the interplay between market sentiment, company performance, and valuation metrics. It underscores that while past valuations might have been driven by speculative fervor, the current valuation is increasingly anchored by tangible improvements in Eli Lilly’s financial performance and its robust growth prospects.

Risks and Challenges on the Horizon

Despite its impressive growth and strong market position, Eli Lilly is not without its inherent risks and challenges. A primary concern is the company’s increasing reliance on Mounjaro and Zepbound. These two drugs are currently the principal drivers of Eli Lilly’s expansion, making the company’s financial results particularly sensitive to several factors. Competition from rival treatments, potential manufacturing constraints that could limit supply, unforeseen safety concerns, or demand that falls short of expectations could all have a significant impact on the company’s performance. The emergence of new obesity drugs or advancements in rival therapies could also erode Eli Lilly’s market share and exert downward pressure on pricing.

Furthermore, access to these groundbreaking medications remains a significant hurdle. Many insurance providers and employers continue to impose limitations on coverage for weight-loss drugs, restricting the number of patients who can readily access these potentially life-changing treatments. This dynamic introduces a layer of complexity to market penetration and revenue realization.

Beyond the specific challenges related to its blockbuster drugs, Eli Lilly faces the standard array of risks inherent in the pharmaceutical industry. These include the possibility of clinical trials failing to yield positive results, delays in regulatory approvals, patent disputes that could challenge exclusivity, and ongoing pricing pressures from healthcare systems and governments worldwide. Given the stock’s premium valuation, which implies high investor expectations, even a minor setback or a less-than-stellar development could trigger a disproportionately negative reaction in the stock price.

The Bottom Line: A Powerful Growth Story with Evolving Dynamics

Eli Lilly has firmly established itself as a formidable growth story within the pharmaceutical sector. Its success is underpinned by a potent combination of rapid revenue expansion, steadily improving profitability, and a comprehensive pipeline of promising drug candidates. The significant growth in its earnings has played a crucial role in keeping the stock’s valuation at a level that, while reflecting its strong performance, remains below some of the historical peaks witnessed during periods of intense market exuberance. This balanced valuation, coupled with its recent ascent to record highs, signifies a company that is delivering on its growth promises.

For investors who are bullish on Eli Lilly, the company’s market leadership in critical therapeutic areas, its consistently improving financial fundamentals, and its extensive runway for continued growth present compelling arguments for investment. The ongoing innovation within its pipeline, particularly in the areas of obesity and metabolic diseases, offers substantial long-term potential.

Conversely, bears might draw attention to the intensifying competitive landscape, the exceptionally high expectations embedded within the stock’s current valuation, and the inherent risks associated with relying heavily on a few key growth drivers. The success of Mounjaro and Zepbound is a double-edged sword, offering immense upside but also concentrating risk.

Ultimately, Eli Lilly represents a dynamic intersection of scientific innovation, market demand, and financial performance. Its ability to navigate the complex regulatory environment, manage competitive pressures, and continue delivering on its pipeline will be critical in determining its long-term trajectory and sustained market leadership. The company’s journey is a compelling case study in how groundbreaking pharmaceutical innovation, when coupled with sound financial management and strategic foresight, can create significant shareholder value while addressing critical global health challenges.

Disclaimer:

Please note that due to market volatility, some of the prices and scenarios discussed may have already been realized or are subject to rapid change. This analysis is for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making any investment decisions.

{kind=link}