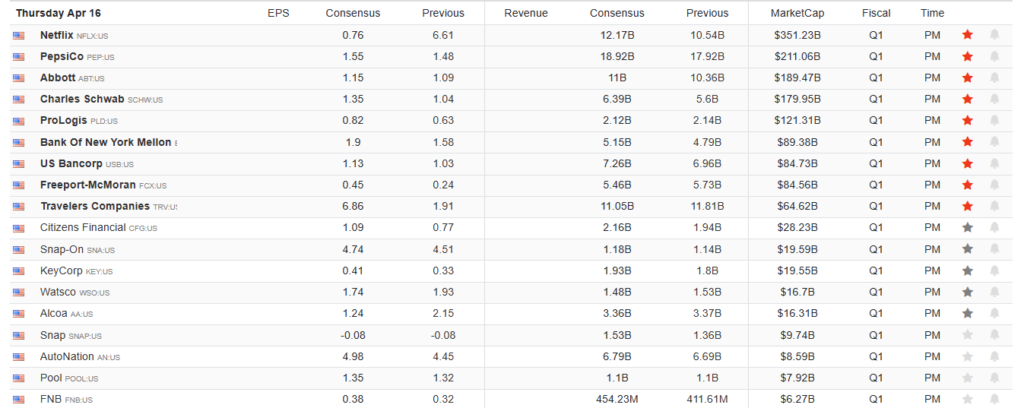

The Market Knows Best: Geopolitical Shifts, Tech Valuations, and the Growing Shadow of Private Credit

Global financial markets have once again demonstrated a remarkable capacity to anticipate geopolitical shifts well before they are codified in official diplomatic announcements. As of Wednesday, April 15, 2026, the S&P 500 has not only erased the entirety of the losses sustained during the recent period of heightened tensions between the United States and Iran but has also achieved a new all-time high. This recovery, occurring over a mere two-week window, serves as a potent reminder of the "efficient market hypothesis" in action—the principle that market prices aggregate all available information, including insights that may not yet be accessible to the general public.

The rally began in earnest following the market lows of late March. On March 30, investor sentiment was at a nadir, characterized by aggressive rhetoric from the Trump administration and Iranian spokespersons. At that time, energy analysts and market pundits warned of a potential catastrophe in the commodities sector, with some forecasting oil prices to surge toward $150 or even $200 per barrel. Despite these dire projections, the S&P 500 began a stealthy ascent, rising approximately 7% in the days leading up to the announcement of a tentative ceasefire. By the time President Trump unofficially declared on Wednesday that the conflict was "close to over," the market’s reaction was tellingly muted; the S&P 500 opened flat and crude oil prices remained stable. The "good news" had already been baked into the price action long before the news cycle caught up.

A Chronology of De-escalation and Market Resilience

The timeline of the recent volatility reveals a distinct pattern of sentiment-driven selling followed by a technically supported recovery. In late March, the geopolitical backdrop appeared increasingly fractured. Military maneuvers in the Middle East and threats to the Strait of Hormuz led to a sharp spike in the Volatility Index (VIX) and a significant increase in short interest as hedge funds bet on a prolonged conflict.

However, the tide began to turn in early April. Even as military actions continued, subtle diplomatic signals—later identified as talks in Islamabad—began to filter through to institutional desks. While the general public remained focused on the potential for war, the market began to price in a de-escalation. By the second week of April, the Nasdaq Composite had embarked on a 10-session winning streak, its longest in several years. This momentum was further bolstered by reports of commercial vessels clearing the Strait of Hormuz without incident, a physical signal that the maritime blockade feared by energy traders was not materializing.

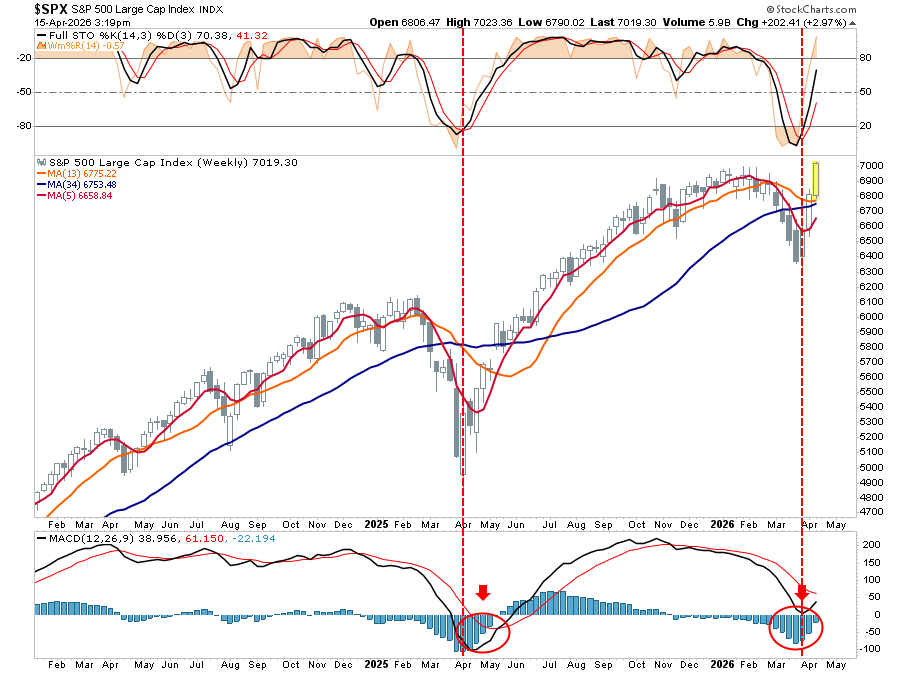

The recovery was not merely a product of diplomatic optimism but was also driven by structural market mechanics. The high level of short interest entering April provided the fuel for a "short squeeze." As the index crossed key resistance levels, traders who had bet against the market were forced to buy back positions to cover their losses, creating a self-reinforcing upward cycle. By April 14, the S&P 500 had tagged its January 27 peak, effectively closing the "war gap" and setting the stage for the current all-time high.

Technical Indicators and the Bull-Bear Debate

While the rapid ascent has left some analysts skeptical, the underlying technical setup suggests a degree of stability that contradicts the "short-covering only" narrative. Throughout the recent selloff, the 50-day moving average remained comfortably above the 200-day moving average. The absence of a "death cross"—a common technical signal for a long-term bear market—provided a foundation for algorithmic and trend-following investors to maintain long positions.

Furthermore, market breadth has shown marked improvement. Unlike previous rallies that were led by a narrow group of mega-cap technology stocks, the current move has seen participation across various sectors, including financials and industrials. The VIX has retreated below the 20-level, indicating that the "fear premium" has largely evaporated.

Conversely, the bearish contingent argues that this rally is built on "borrowed momentum." They point out that the macro and geopolitical backdrop has softened rather than structurally improved. These skeptics suggest that until there is a clear upward revision in corporate earnings or a significant improvement in global balance sheets, the market remains vulnerable to "harsher realities." The upcoming three weeks of S&P 500 earnings reports will serve as the ultimate litmus test for whether this rally can be sustained by fundamentals or if it will retreat toward its previous support levels.

The AI Arms Race: Anthropic’s Valuation Surge

In the private markets, the fervor surrounding artificial intelligence continues to defy traditional valuation metrics. Anthropic, the developer behind the Claude AI model, is reportedly fielding investor offers that would value the firm at upwards of $800 billion. This represents a staggering doubling of its $350 billion valuation established during a fundraising round just two months ago in February.

The primary catalyst for this valuation spike appears to be an unprecedented acceleration in revenue. Anthropic recently disclosed that its annualized revenue has reached $30 billion, a sharp increase from the $19 billion reported only months prior. This growth trajectory places Anthropic in direct competition with OpenAI, which currently generates approximately $2 billion per month in revenue and was recently valued at $850 billion.

The institutional interest in Anthropic is also being driven by anticipation of a potential initial public offering (IPO) in the fall of 2026. Venture capital firms and sovereign wealth funds are reportedly scrambling for exposure, viewing the current AI boom as a generational shift in the global economy. However, some economists warn that the rapid escalation in AI valuations mirrors the dot-com era, where capital was deployed based on projected dominance rather than current profitability. The discrepancy between the astronomical private valuations and the actual integration of AI into broader industrial productivity remains a point of contention for value-oriented investors.

Systemic Risks: Is Private Credit the Next Subprime?

While the public markets celebrate new highs, a growing chorus of financial historians and risk managers is expressing concern over the rapid expansion of the private credit market. Drawing parallels to the 2008 subprime mortgage crisis, analysts suggest that the next financial contagion may stem from a lack of transparency and trust in non-bank lending.

In the lead-up to the 2008 crisis, the "match" that lit the fire was the default of subprime borrowers. However, the "bonfire" was the complex web of leverage and derivatives that interconnected the world’s largest financial institutions. When trust eroded, the overnight Fed Funds and repo markets—the "boiler room" of the global financial system—seized up.

Today, the private credit market has grown into a multi-trillion-dollar ecosystem, largely operating outside the regulatory scrutiny applied to traditional commercial banks. This sector provides loans to mid-sized companies and private equity-backed firms that may not qualify for traditional bank financing. The concern is that as interest rates remain elevated, the ability of these borrowers to service their debt is diminishing.

If defaults in the private credit sector begin to rise, the lack of a transparent secondary market could lead to a sudden "repricing" of risk. Much like the collapse of Lehman Brothers and the near-failure of AIG, a systemic shock in private credit could lead to a freezing of the repo markets, as counterparties question the solvency of their peers. The "web of leverage" in the 2020s is built on private debt rather than mortgages, but the fundamental risk—the loss of confidence in the overnight repayment of loans—remains the same.

Looking Ahead: Earnings and Economic Anchors

As the market digests the "peace dividend" from the Middle East and the soaring valuations in the AI sector, the focus now shifts to the fundamental health of corporate America. JPMorgan Chase has already reported its quarterly earnings, providing a solid start to the season, but the true test lies in the hundreds of S&P 500 companies scheduled to report over the next 21 days.

Investors are watching for two key themes: margin preservation in the face of persistent inflation and the actual capital expenditure related to AI implementation. While the geopolitical situation has "softened," the structural challenges of the global economy—high debt levels, shifting demographics, and trade fragmentation—have not disappeared.

The market’s current all-time high acts as both a magnet for optimistic capital and a potential ceiling for those wary of overextension. A clean breakout on high trading volume would signal that the market has found a new fundamental floor. Until then, the prevailing wisdom remains rooted in the lesson of the past two weeks: respect the price action, for the market possesses a collective intelligence that consistently outpaces the headlines. As the investment community navigates this complex landscape, the goal remains the management of risk rather than the pursuit of certainty, ensuring that stop levels are maintained and exposure is added only on confirmed technical strength.

{kind=link}