Federal Reserve Chair Kevin Warsh Signals Resolute Stance on Inflation as Market Leadership Rotates Toward Value and Small-Cap Equities

Federal Reserve Chairman Kevin Warsh completed his inaugural semiannual monetary policy testimony before Congress this week, delivering a message defined by a rigorous commitment to price stability and a notable departure from the policy communication strategies of his predecessors. Speaking before both the House Financial Services Committee and the Senate Banking Committee, Warsh utilized the platform to underscore the central bank’s singular focus on returning inflation to its long-term 2% target. His rhetoric was characterized by a lack of ambiguity, asserting that the Federal Reserve has "no tolerance for persistently elevated inflation" and making the bold prediction that "inflation will be a thing of the past" under the current committee’s stewardship.

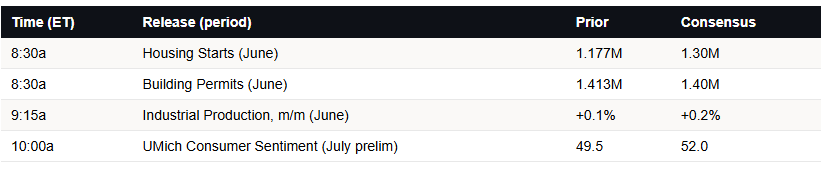

The timing of the testimony coincided with the release of the June Consumer Price Index (CPI) report, which arrived just 90 minutes before Warsh began his House testimony on Tuesday. The report provided a favorable backdrop for the Chairman, revealing a 0.4% monthly decline in consumer prices. While the data suggested a cooling of inflationary pressures, Warsh exercised caution, resisting the urge to declare a premature victory or signal an immediate shift in interest rate policy. He characterized the report as a "single data point" and warned against the dangers of "cherry-picking" information to suit a specific narrative. This disciplined approach suggests a central bank that is determined to see a sustained trend before adjusting its restrictive monetary stance.

A New Philosophy: The Rejection of Forward Guidance

One of the most significant takeaways from Warsh’s testimony was his explicit aversion to "forward guidance," a communication tool heavily utilized by the Federal Reserve over the last two decades. Forward guidance involves the central bank providing explicit signals about the future path of interest rates to influence market expectations. However, Warsh argued that this practice is fundamentally flawed due to human behavioral tendencies.

Warsh posited that when a policy committee publishes a specific projection or "dot plot," members inevitably become psychologically anchored to those forecasts. He explained that once a projection is public, there is a natural human tendency to favor information that supports the prior forecast while rejecting data that contradicts it. This cognitive bias, known as confirmation bias, can lead to policy errors by making the committee less responsive to shifting economic realities. By moving away from forward guidance, Warsh intends to foster a committee that is "more circumspect" and truly data-dependent. This shift suggests that market participants should expect less predictability from the Fed and more volatility in response to incoming economic releases.

Market Dynamics and the "Great Rotation"

While the Federal Reserve signaled a steady hand, the equity markets experienced a period of internal turbulence. On the surface, major indices like the S&P 500 appeared stable, remaining near record highs. However, a deeper analysis of market internals reveals a significant shift in leadership—a phenomenon often referred to by analysts as "money changing seats."

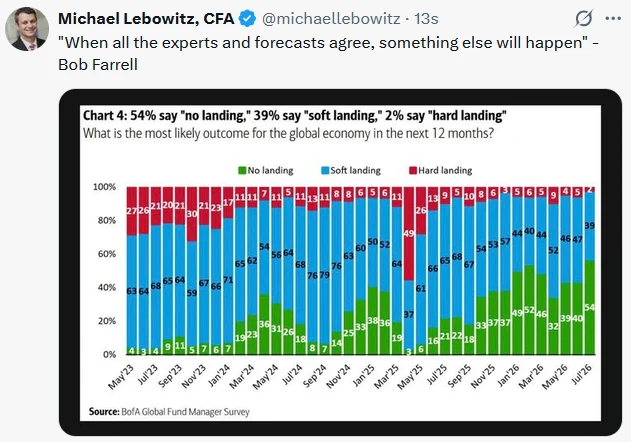

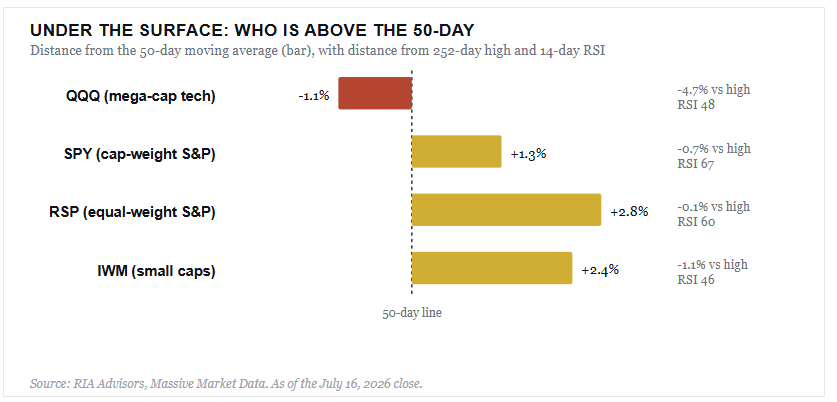

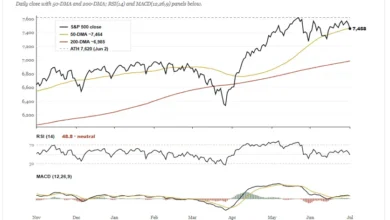

For much of the year, the market’s gains have been concentrated in a handful of mega-cap technology and semiconductor stocks. This concentration reached what some analysts described as a "historic extreme." This week, however, that leadership began to crack. The VanEck Semiconductor ETF (SMH) saw a sharp decline of approximately 3%, and the Nasdaq 100 slipped below its 50-day moving average for the first time in several months. This technical breakdown suggests that the "AI trade" and the broader technology sector may be entering a period of consolidation or deleveraging.

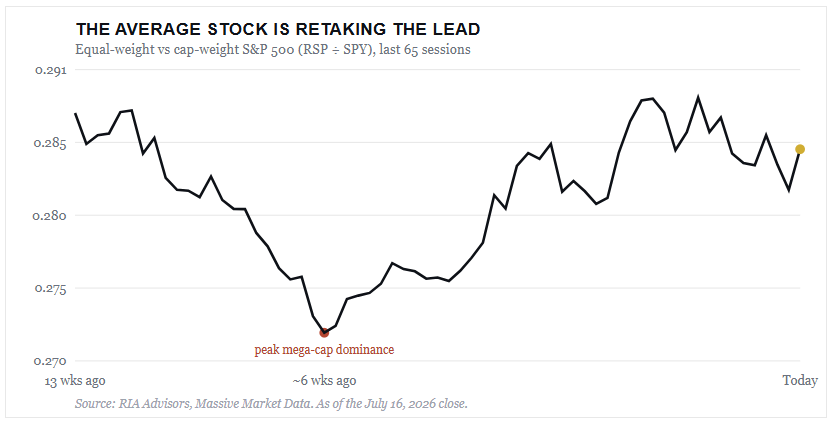

Crucially, the decline in tech did not lead to a broad market sell-off. Instead, capital flowed into previously underperforming sectors. The equal-weight S&P 500 (RSP) actually rose during the tech retreat, maintaining a healthy Relative Strength Index (RSI) of 60. Similarly, the Russell 2000 Small-Cap Index (IWM) and the Dow Jones Industrial Average showed signs of life. This broadening of market participation is generally viewed as a healthy development for the longevity of a bull market, though the catalyst in this instance appears to be a "forced rotation" caused by profit-taking in tech rather than a surge of new optimism regarding economic growth.

The SK Hynix ADR Paradox: Examining the Reverse Kimchi Premium

In the international arena, the listing of South Korean chipmaker SK Hynix on the Nasdaq provided a stark example of market inefficiency and the complexities of cross-border investing. South Korean equities have historically traded at a "Kimchi discount," a term used to describe the lower valuations assigned to Korean firms due to perceived weaknesses in corporate governance and shareholder returns. However, the debut of SK Hynix’s American Depositary Receipts (ADRs) under the ticker SKHY presented the opposite phenomenon: a "Reverse Kimchi Premium."

On its first day of trading, the SK Hynix ADR closed at $193.92, despite each ADR representing only one-tenth of an ordinary share listed in Seoul. With the Seoul-listed shares closing at the equivalent of $1,280, the ADR should have theoretically traded near $128. Instead, U.S. investors paid a premium of nearly 50% for identical ownership rights, earnings, and dividends.

This massive price discrepancy persists due to structural barriers in the arbitrage mechanism. While SK Hynix ADRs can be converted into Seoul-listed shares with relative ease, the conversion of Seoul shares into U.S. ADRs requires complex regulatory approval. This one-way street limits the ability of institutional traders to close the gap by buying the cheaper Korean shares and selling the more expensive U.S. ADRs. A similar trend has been observed with Taiwan Semiconductor Manufacturing Company (TSMC), which has maintained a persistent U.S. premium for years. The SK Hynix case serves as a reminder that liquidity and exchange-specific demand can often override fundamental valuation parity.

Congressional Inquiry and Central Bank Independence

During the testimony, members of Congress pressed Warsh on the issue of the Federal Reserve’s independence from the executive branch. Representative Nydia Velázquez specifically questioned whether Warsh’s policy decisions were influenced by the current administration’s goals. Warsh was firm in his response, stating, "We’re an independent central bank." He committed to following "the law and the data," reinforcing the institution’s mandate to remain insulated from short-term political pressures.

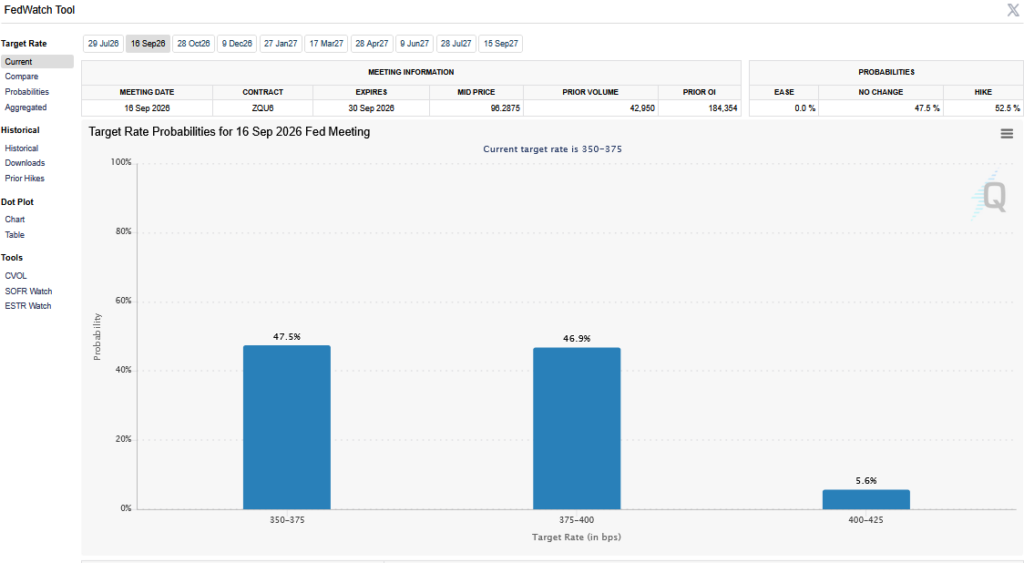

The question of independence is particularly relevant as the market looks toward the September FOMC meeting. Current Fed Funds futures indicate a committee that is sharply divided on the necessity of a rate hike. While the cooling CPI data provides an argument for a pause, Warsh’s "no tolerance" stance on inflation suggests that the bar for a "dovish pivot" remains high.

Chronology of Key Events

- Tuesday, 8:30 AM: The Bureau of Labor Statistics releases the June CPI report, showing a 0.4% decline in prices, the first negative reading in several months.

- Tuesday, 10:00 AM: Chairman Kevin Warsh begins his semiannual testimony before the House Financial Services Committee, emphasizing the 2% inflation target.

- Tuesday, 4:00 PM: SK Hynix ADRs conclude their first day of trading on the Nasdaq with a 50% premium over their domestic South Korean counterparts.

- Wednesday, 10:00 AM: Warsh continues his testimony before the Senate Banking Committee, focusing on the psychological pitfalls of forward guidance and the need for circumspect policy.

- Thursday, Market Close: The Nasdaq 100 finishes below its 50-day moving average, while the equal-weight S&P 500 continues to show relative strength, confirming a shift in market leadership.

- Saturday, July 18: The Federal Reserve enters its official "blackout period" ahead of the July 28–29 FOMC meeting, during which governors and presidents refrain from public comment.

Fact-Based Analysis of Implications

The events of this week suggest a transition period for both monetary policy and financial markets. Chairman Warsh’s rejection of forward guidance marks a return to an older school of central banking, where the "element of surprise" or at least a lack of pre-commitment is seen as a virtue. For investors, this means that macroeconomic data releases—such as employment figures and inflation reports—will carry even greater weight, as the Fed will no longer be providing a roadmap for how it intends to react.

Furthermore, the "forced broadening" of the stock market presents a complex risk-reward profile. While it is positive that capital is rotating into small-cap and value stocks, these sectors are more sensitive to interest rate fluctuations. If Warsh’s hawkish rhetoric translates into higher-for-longer yields, the very stocks that investors are rotating into (like those in the IWM) could face headwinds from rising borrowing costs and a strengthening dollar.

The semiconductor sector’s recent volatility also warrants close monitoring. As the primary engine of the market’s gains over the past year, a sustained downturn in chips could weigh on the headline indices, even if the "average" stock continues to rise. Analysts suggest that the rotation from tech to value may be a deleveraging event rather than a fundamental shift in economic outlook.

As the Federal Reserve heads into its blackout period, the market is left to digest a dual message: a central bank that is uncompromising on inflation and a market that is searching for a new identity beyond the technology giants. With the S&P 500 sitting near its 50-day moving average of 7,456 (in this specific market context), the coming weeks will determine whether the "Great Rotation" has the stamina to lead the market to new highs or if the tech-led retreat will eventually pull the broader indices lower. For now, the strategy among institutional desks appears to be one of cautious diversification—keeping quality high and maintaining liquidity as the "Warsh Fed" begins its new era of data-driven uncertainty.

{kind=link}