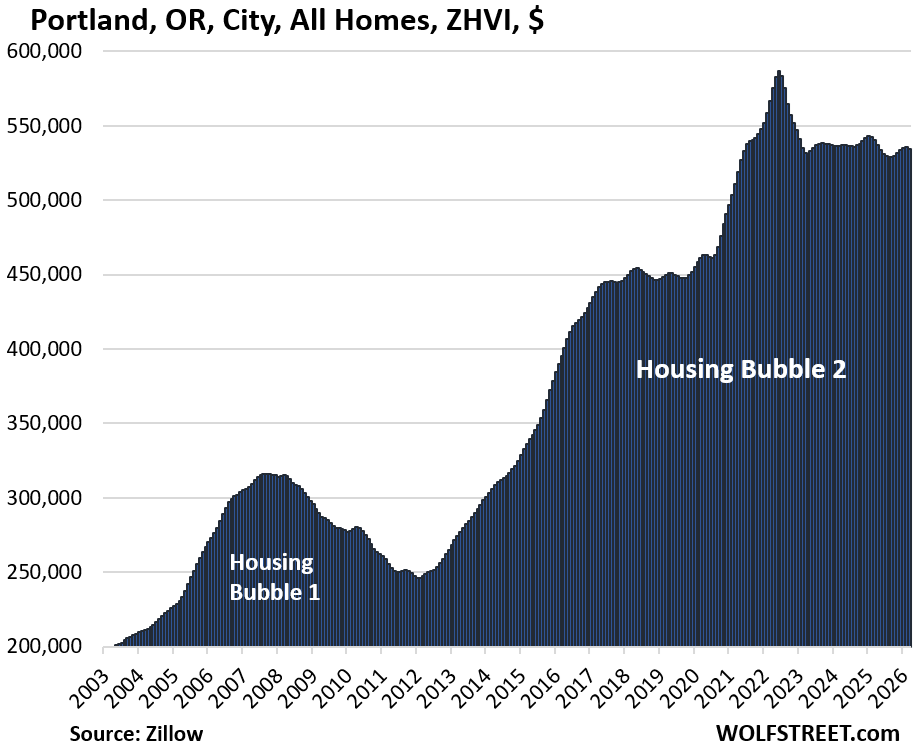

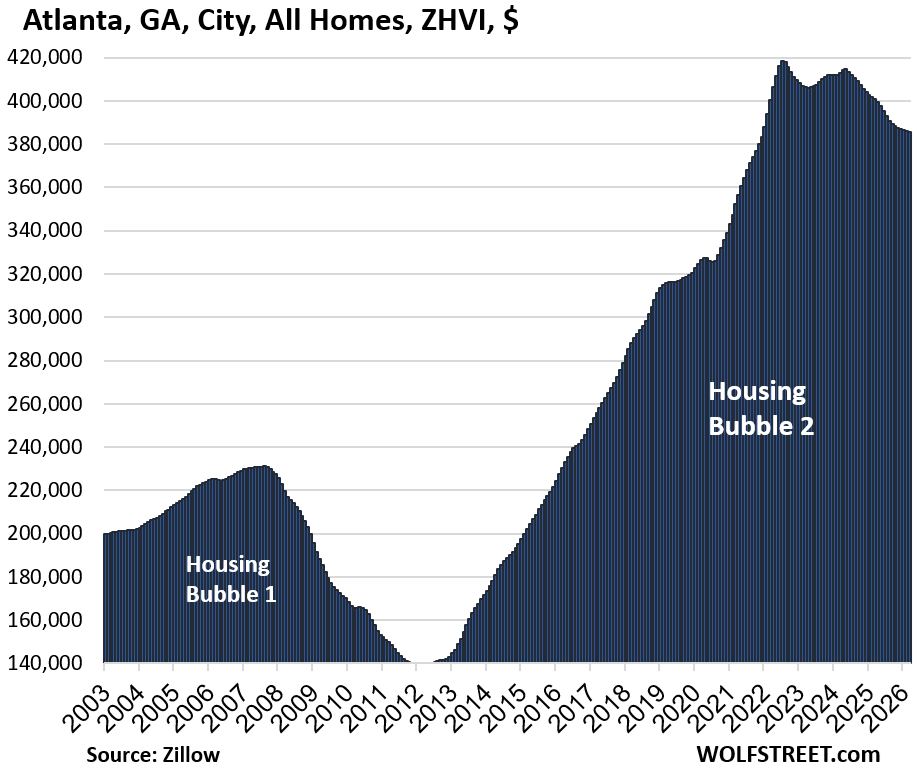

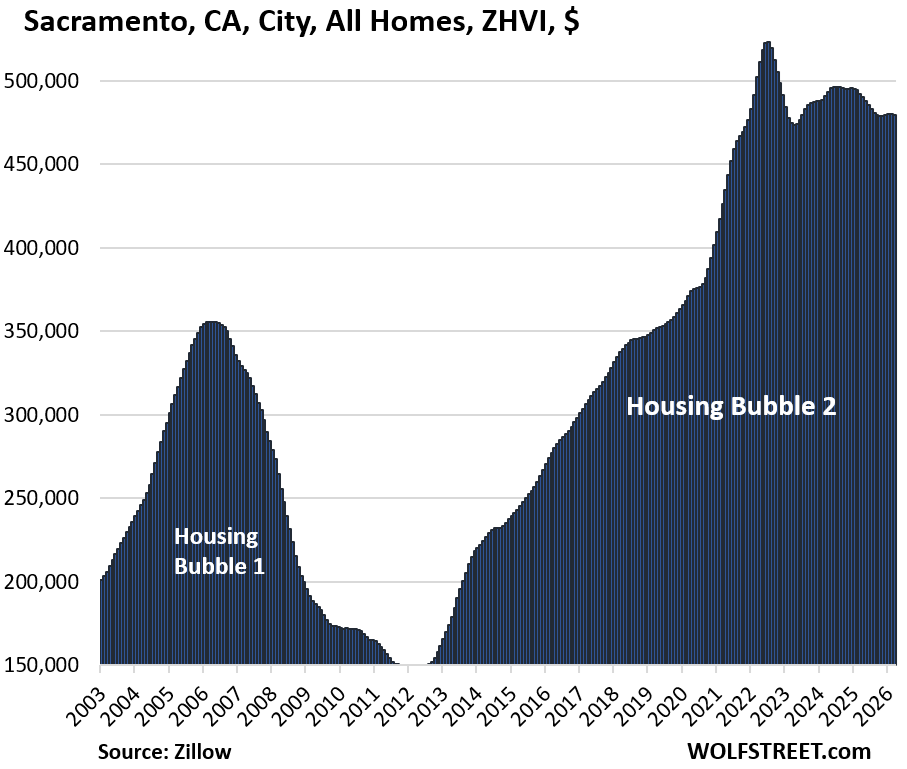

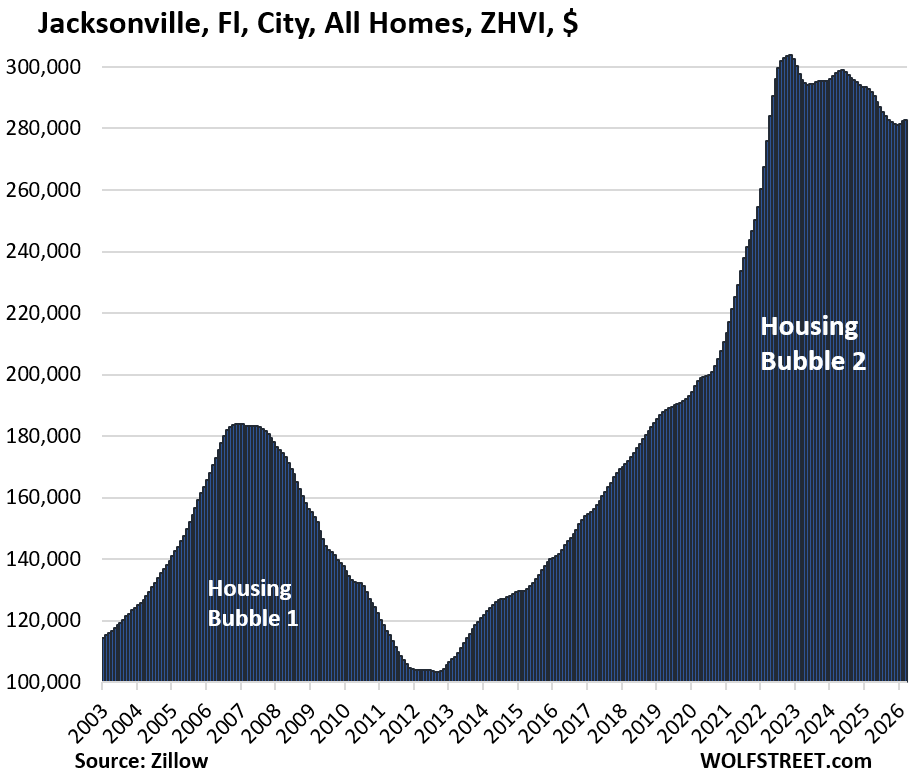

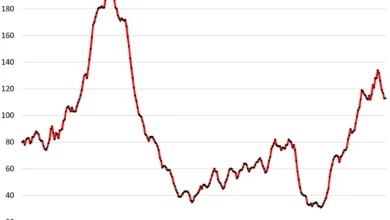

The Most Splendid Housing Bubbles in America: Price Drops & Gains in 33 Big Expensive Cities, March 2026

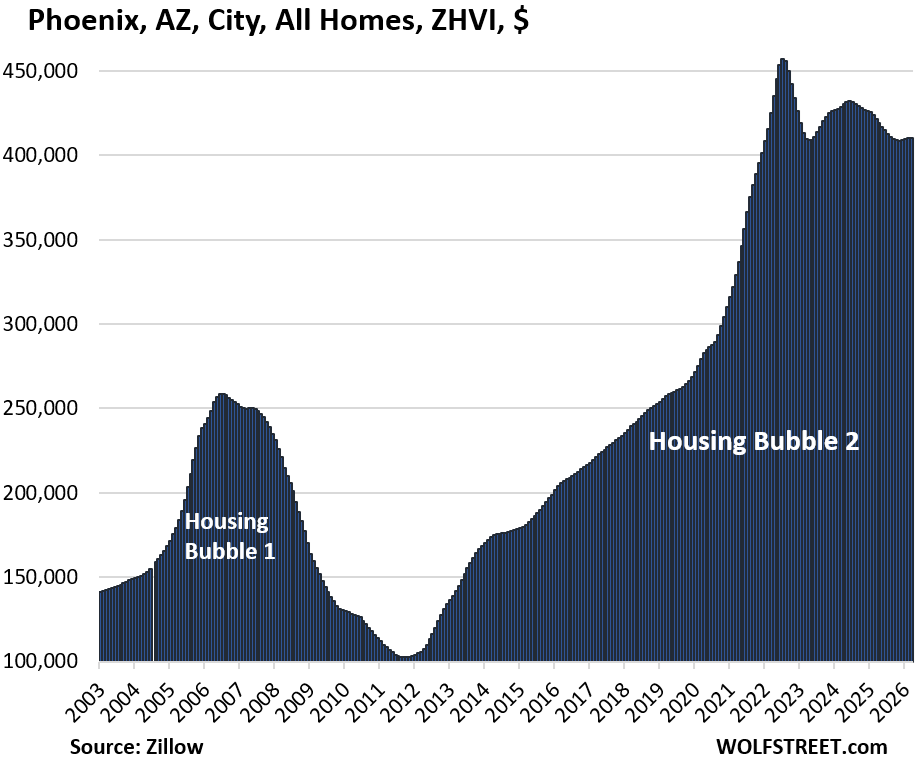

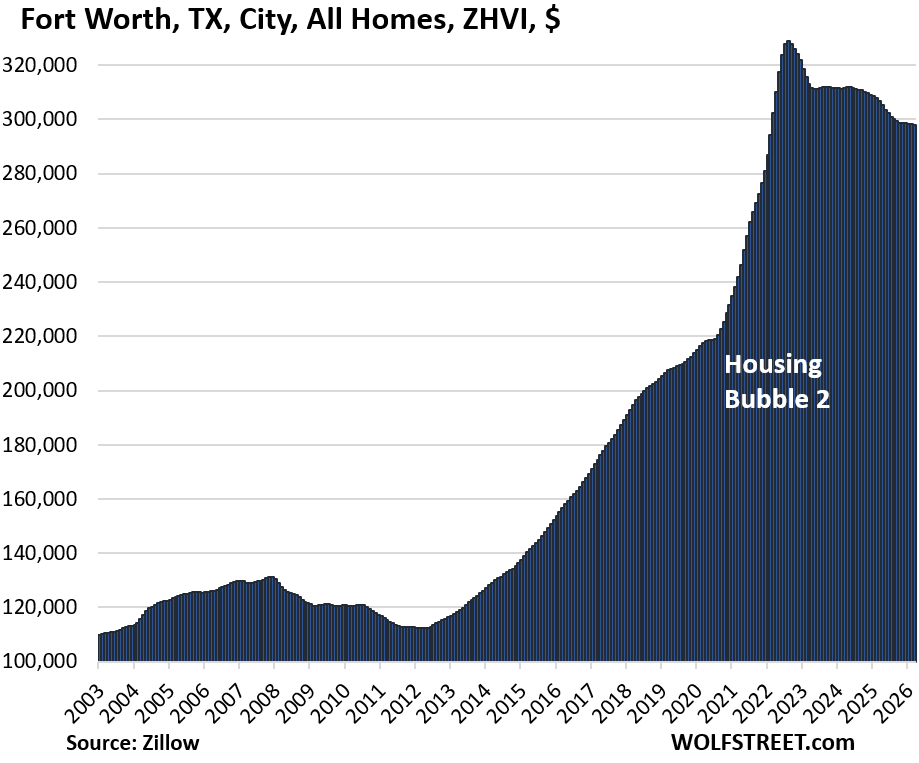

The current market correction serves as a sobering counterpoint to the "price explosions" witnessed between mid-2020 and mid-2022. During that two-year window, cities like Austin (+62%), Phoenix (+60%), Fort Worth (+50%), and Raleigh (+49%) saw valuations soar to levels that many economists now define as classic speculative bubbles. These gains were largely predicated on the Federal Reserve’s aggressive monetary easing, which saw trillions of dollars in Treasury and mortgage-backed securities purchases drive mortgage rates below the 3% threshold. This "free-money" environment ignited a period of frantic "Fear of Missing Out" (FOMO) buying, even as broader consumer inflation surged toward 9%. By March 2026, the legacy of that era is one of price recalibration as the market adjusts to a higher interest rate environment and more normalized demand.

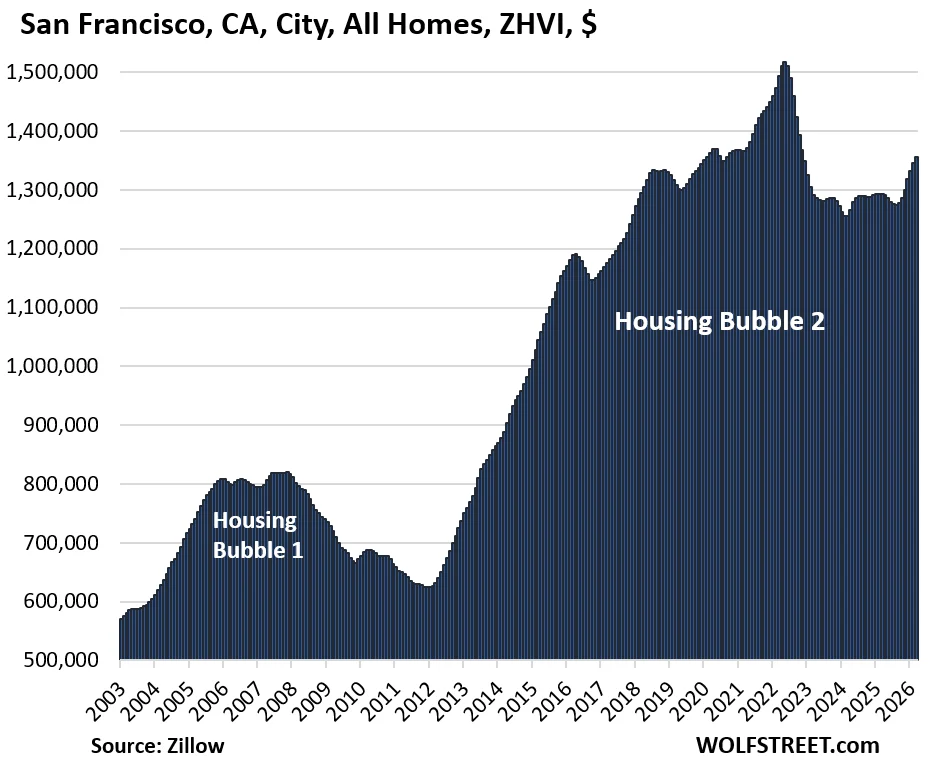

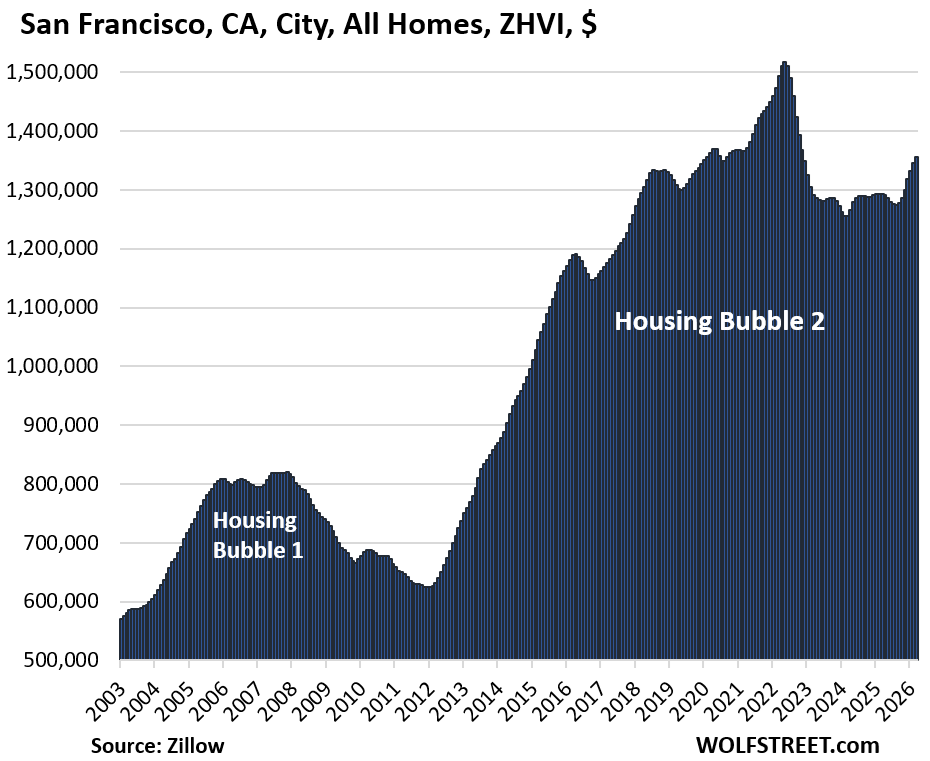

The San Francisco Paradox: AI Wealth and the Mansion Shortage

San Francisco remains the most complex case study in the 2026 housing market. While the city has faced broader economic headwinds, including a drop in total employment and a slight uptick in the unemployment rate, the mid-tier housing segment is experiencing an unexpected price infection. This phenomenon is being driven by what local analysts term the "mansion shortage." As the epicenter of the global artificial intelligence investment bubble, San Francisco has become a magnet for a relatively small but exceptionally well-compensated cohort of AI professionals.

These individuals, armed with significant capital and "easy-come-easy-go" liquidity from the tech sector, are finding a severe lack of inventory in the luxury "mansion" category. Consequently, this high-end demand is cascading down into the mid-tier market. Wealthy buyers, unable to secure ultra-premium properties, are aggressively outbidding traditional buyers for mid-tier homes, effectively inflating the middle-third of the market. Despite this recent upward pressure, mid-tier prices in San Francisco remain 11% below their 2022 all-time highs. Interestingly, this trend has not fully crossed the South Bay; in San Jose, where mid-tier homes are even more expensive than in San Francisco, prices have continued to dip as the market struggles with extreme affordability constraints.

The Correction in the Sunbelt and Tech Hubs

The most dramatic reversals have occurred in markets that were the primary beneficiaries of the "Zoom town" migration during the early 2020s. Austin, Texas, once the poster child for the pandemic real estate boom, has seen the most significant deflation. Its 26% drop from the June 2022 peak brings valuations back to levels not seen since March 2021. This suggests that the entirety of the gains made during the peak speculative months of 2022 has been erased.

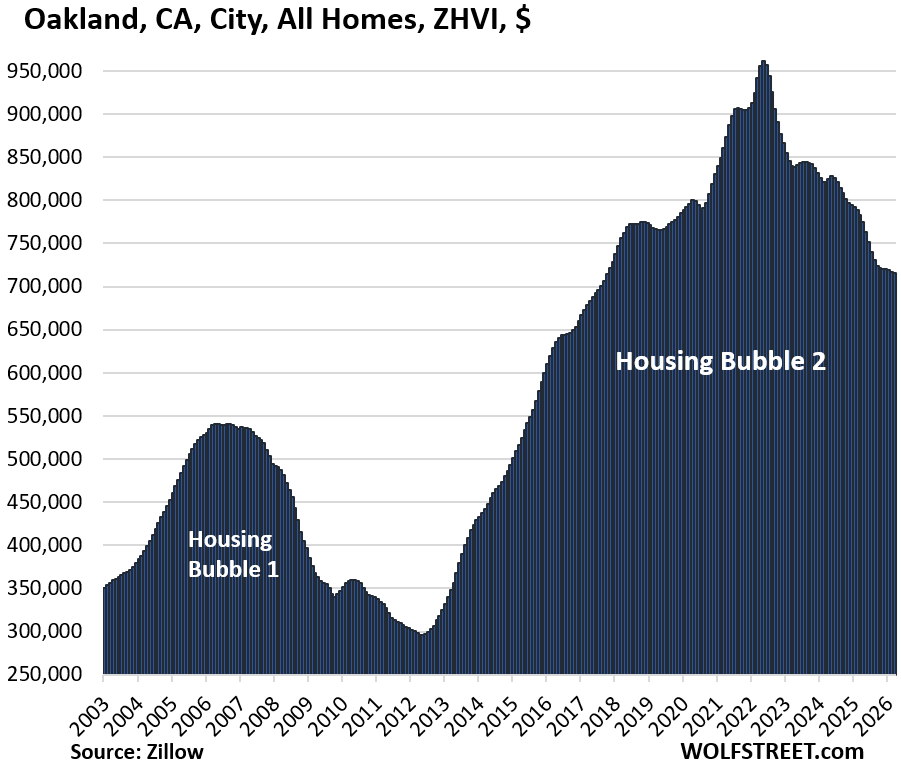

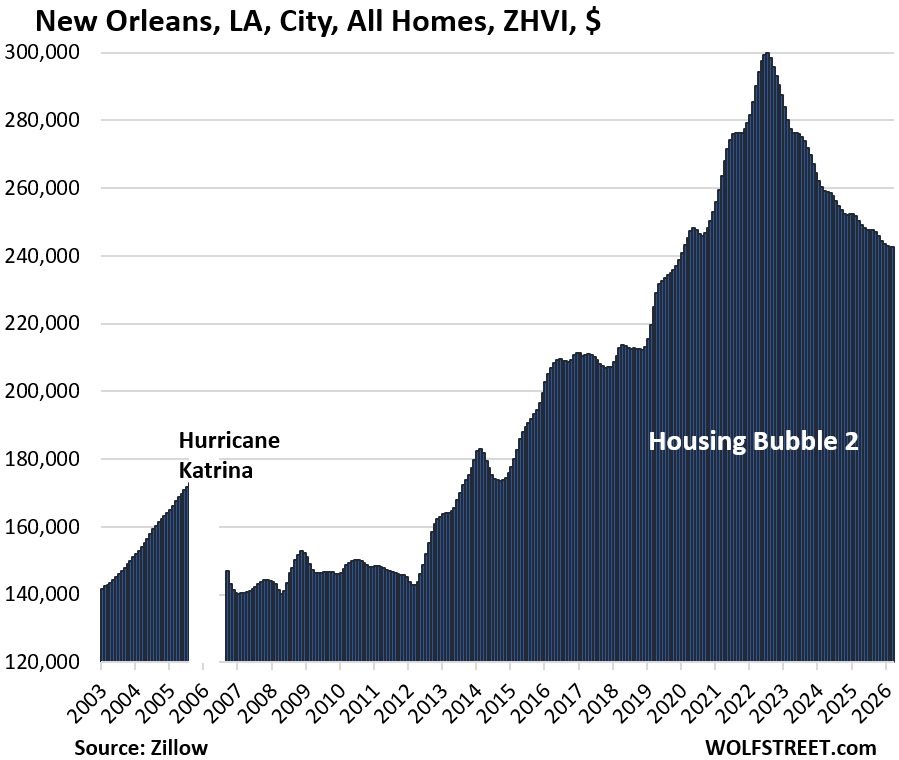

Similarly, Oakland has seen a 25% correction from its May 2022 peak, marking its lowest price levels since October 2017. The Bay Area’s East Bay market is feeling the combined pressure of high interest rates and a shift in remote work preferences that has reduced the urgency for suburban expansion. In the South, New Orleans has experienced a 19.1% decline, returning to price levels last seen in early 2020. These corrections highlight a broader trend: the cities that grew the fastest during the period of reckless monetary policy are now the ones experiencing the most painful "reversion to the mean."

Regional Resilience: The East Coast and Midwest

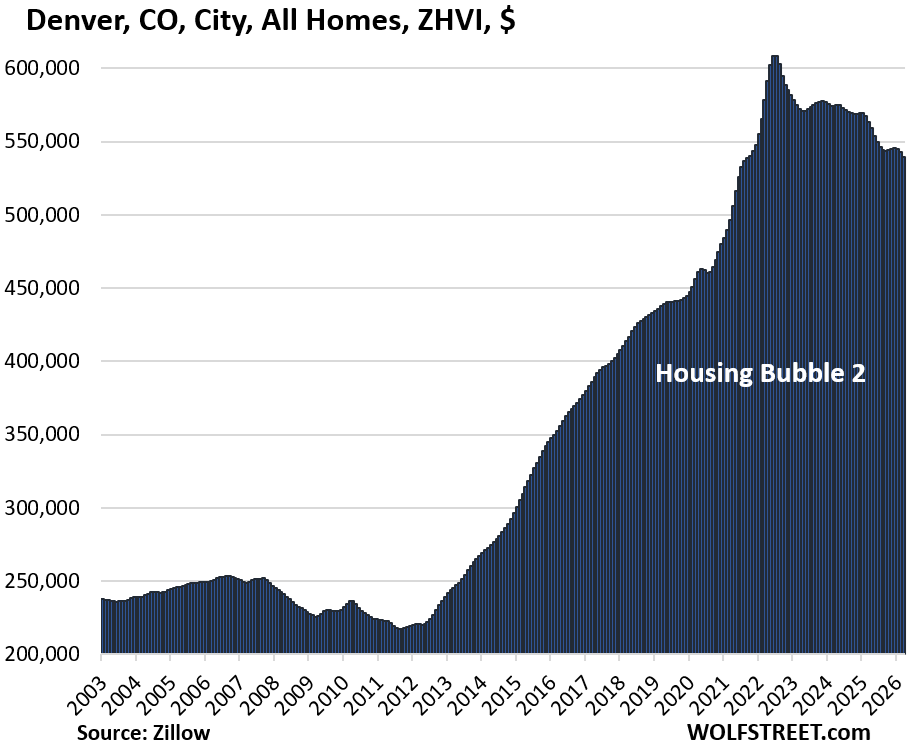

In contrast to the volatility of the West and the Sunbelt, several legacy hubs and Midwestern cities are showing remarkable resilience. In five of the 33 cities tracked—New York City, Chicago, Philadelphia, Minneapolis, and Omaha—prices reached new seasonally adjusted highs in March 2026. However, the pace of growth in these markets is markedly slower than the double-digit surges seen in 2021.

New York City saw a year-over-year increase of 4.5%, while Chicago followed with a 2.8% gain. Philadelphia and Minneapolis saw more modest growth at 2.0% and 1.4%, respectively. Omaha, Nebraska, has emerged as the most expensive major city in the center of the United States, with prices holding steady and reaching new highs. These markets generally avoided the extreme "price explosions" of 2020-2022, which has left them less vulnerable to the current correction. They are characterized by more stable inventory levels and a buyer base less reliant on the speculative tech-wealth cycles that dominate the West Coast.

Boston remains a statistical outlier. While prices in March 2026 were down by approximately 1% from the all-time high set in April 2025, the year-over-year decline was negligible. Analysts suggest the "jury is still out" on whether Boston will enter a sustained correction or maintain its current plateau.

Methodology: Tracking the 33 "Splendid Bubbles"

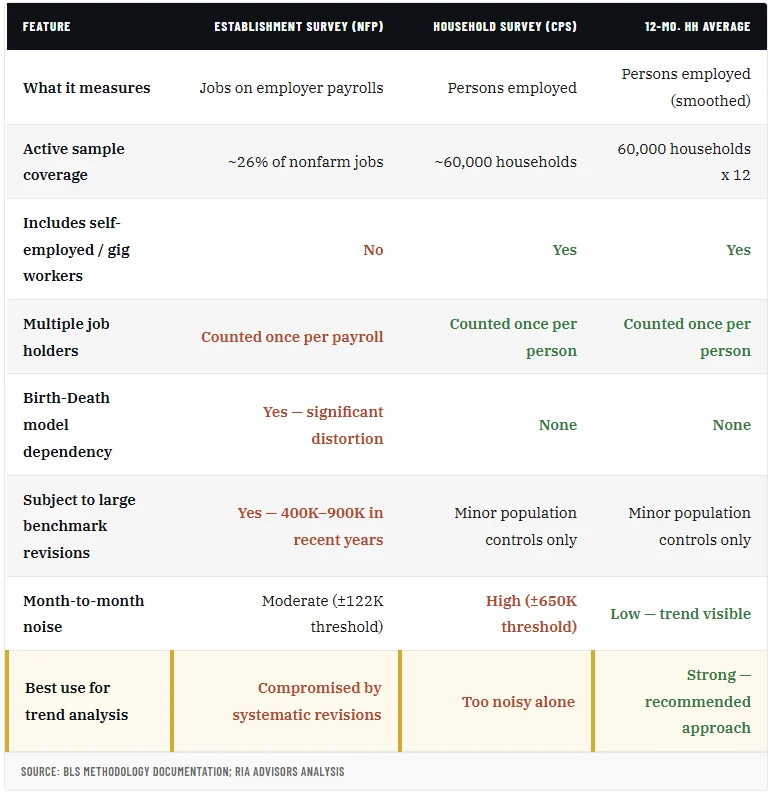

The data for this analysis is derived from the seasonally adjusted three-month-average Zillow Home Value Index (ZHVI). This index tracks the "mid-tier" segment of the market, representing the middle third of home prices for single-family residences, condos, and co-ops. The ZHVI utilizes millions of data points from public records, tax data, MLS listings, and brokerages, and uniquely includes off-market and for-sale-by-owner deals.

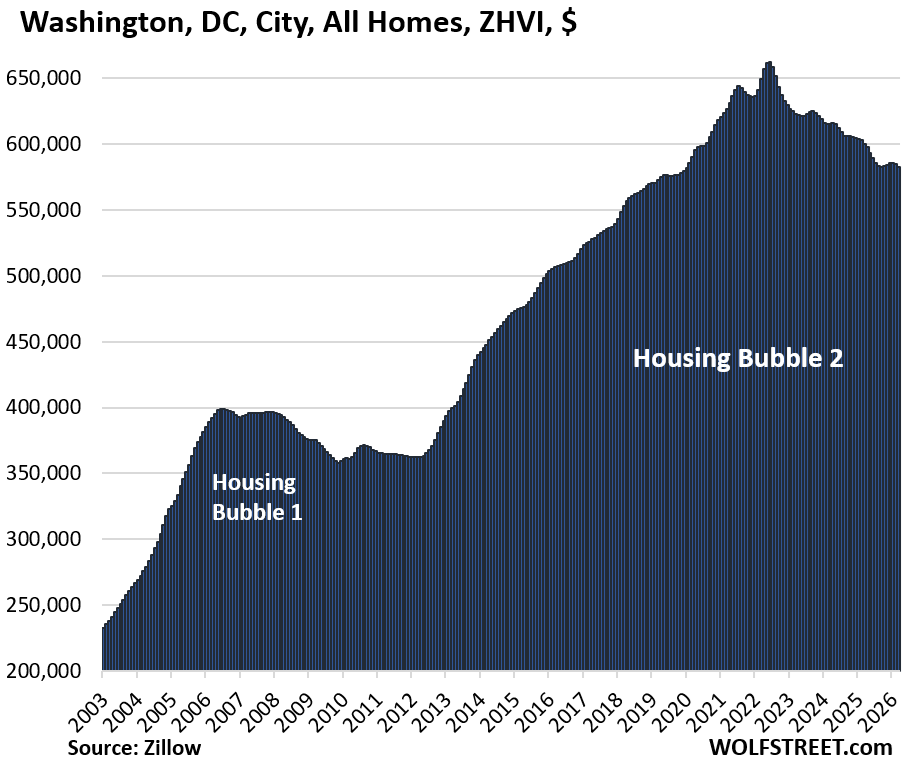

To qualify for the list of the 33 most prominent housing markets, a city must meet specific population thresholds and be considered an "expensive" market, defined as having a mid-tier ZHVI of at least $300,000 at some point in its history. Several major cities, including Houston, Philadelphia, and New Orleans, were included despite not consistently maintaining the $300,000 threshold, due to their sheer size and regional economic importance. Omaha was included as the primary representative of the central U.S. market, as it currently sits at the $300,000 threshold.

Chronology of the Market Shift (2020–2026)

The current state of the market is the result of a multi-year economic cycle that began with unprecedented stimulus:

- Mid-2020 to Mid-2022 (The Explosion): The Federal Reserve implements zero-interest-rate policies and massive quantitative easing. Mortgage rates drop below 3%. Massive domestic migration fueled by remote work leads to 40-60% price increases in "lifestyle" cities like Austin and Phoenix.

- Late 2022 to 2023 (The Pivot): The Federal Reserve begins aggressive interest rate hikes to combat 9% inflation. Mortgage rates double, then triple. Transaction volumes begin to "deep freeze" as sellers hold onto low-rate mortgages.

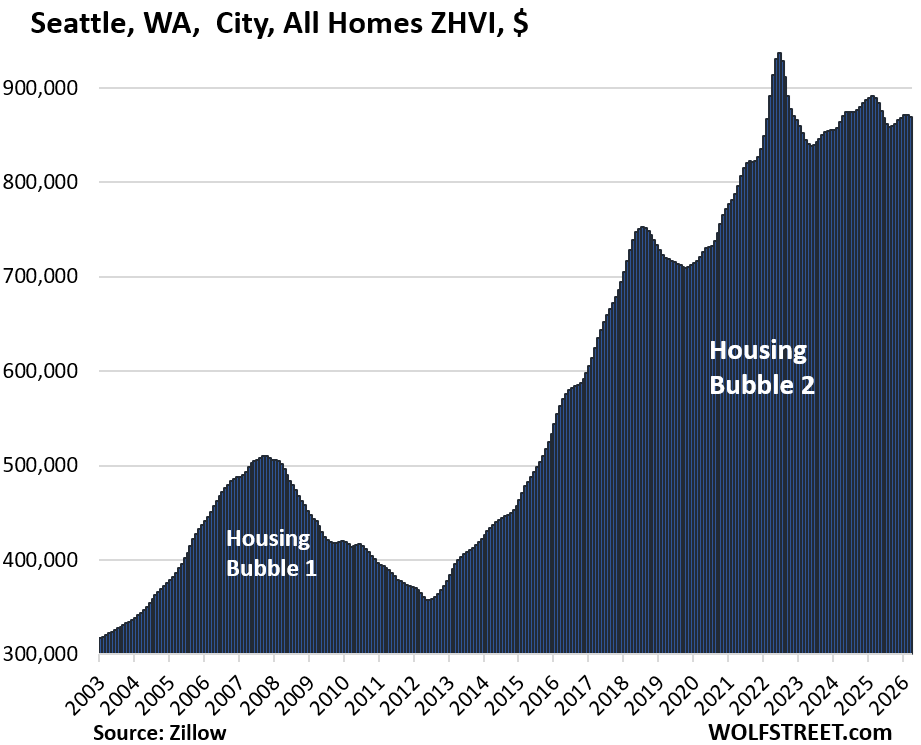

- 2024 to 2025 (The Correction): High-growth markets begin to see price drops as inventory finally builds and affordability hits a wall. Tech-heavy markets like San Francisco and Seattle see initial dips.

- Early 2026 (The Current State): A fragmented market emerges. Most cities are down 5-25% from peaks. The "AI Bubble" creates localized price spikes in San Francisco, while inventory across the nation hits a 10-year high for single-family homes, and condo sales plunge to record lows.

Broader Economic Impact and Implications

The correction in home prices has significant implications for consumer wealth and the broader economy. For homeowners in Austin or Oakland who purchased at the 2022 peak, the loss of 25% in equity represents a substantial hit to household balance sheets. This "reverse wealth effect" is expected to dampen consumer spending in those regions.

Furthermore, the "deep freeze" in transaction volume—where many homeowners are unwilling to sell because they cannot afford to trade their 3% mortgage for a 7% or 8% rate—has led to a stagnation in the real estate services sector. While single-family inventory has reached a 10-year high, it is largely due to homes sitting on the market longer rather than a surge in new listings.

Market analysts suggest that the "mansion shortage" in San Francisco is a warning sign of how concentrated wealth in a single sector (AI) can distort local economies, making "mid-tier" housing unattainable for the very service workers and middle-class professionals the city requires to function. Looking ahead to the remainder of 2026, the trajectory of the U.S. housing market will likely depend on whether the Federal Reserve maintains its restrictive stance or begins to ease rates in response to the softening employment data seen in cities like San Francisco. Until a significant shift in affordability occurs, the "Splendid Bubbles" appear to be in a period of sustained deflation, bringing a definitive end to the era of easy-money real estate gains.

{kind=link}