Canada’s Inflation Outlook: Key CPI Data Looms as Bank of Canada Holds Steady

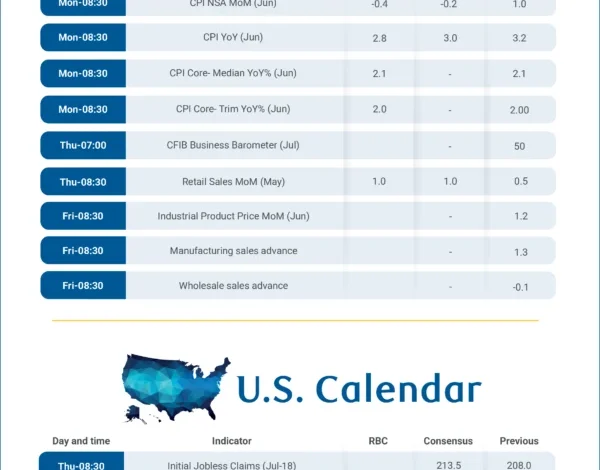

Canada’s upcoming June Consumer Price Index (CPI) report, slated for release on Monday, is poised to offer a crucial snapshot of inflation trends, arriving just weeks after the Bank of Canada’s sixth consecutive decision to maintain its key interest rate at 5.0%. Economists and market watchers will be scrutinizing the data for signs of whether inflationary pressures are continuing to recede, particularly in light of the central bank’s cautious monetary policy stance.

Anticipated Moderation in Headline Inflation Driven by Energy Prices

Analysts widely anticipate a noticeable easing in headline inflation for June, with projections pointing to a year-over-year figure of 2.8%. This would represent a significant deceleration from the 3.2% recorded in May. The primary driver behind this expected moderation is a anticipated sharp decline in energy prices. Specifically, gasoline prices are forecast to have fallen by approximately 10% month-over-month in June, while fuel oil prices are expected to be down by about 6.3%.

While these energy price drops are expected to contribute to a lower overall inflation rate, it’s important to note that energy prices are still projected to remain higher when compared to the same period last year. Nevertheless, their upward pull on the headline inflation figure should diminish.

In contrast to the energy sector, food price inflation is expected to exhibit more resilience. Projections suggest food prices will remain firm, settling around 3.6% year-over-year, a modest decrease from the 3.8% observed in May. This sustained elevated level of food inflation continues to be a significant concern for Canadian households, impacting household budgets and discretionary spending.

Underlying Inflation Shows Stability, Core Measures Near Target

Beyond the more volatile components of food and energy, broader inflation pressures are anticipated to remain relatively stable. Economists forecast that inflation excluding food and energy—often referred to as "core inflation" in a broader sense—will hold steady around 1.6% year-over-year. This figure is expected to be largely unchanged from May, indicating that underlying inflationary forces are not significantly accelerating.

Further bolstering this view, the Bank of Canada’s preferred measures of core inflation, which strip out the most volatile items, are likely to remain consistent with inflation running close to the central bank’s 2% target. These measures are closely watched by policymakers as they are considered more indicative of the persistent inflationary pressures in the economy.

Divergence Between Headline and Underlying Inflation: A Central Focus for the BoC

Recent inflation reports have consistently highlighted a divergence between headline inflation, which includes all goods and services, and underlying inflation, which attempts to smooth out volatile price swings. While elevated energy prices have been a primary contributor to higher headline readings, broader price pressures have remained comparatively contained.

This distinction is expected to remain a central element in the Bank of Canada’s assessment of the inflation outlook. Policymakers have repeatedly emphasized their focus on whether higher energy costs are spilling over into broader consumer prices, leading to a sustained increase in the cost of living across the economy, rather than solely on the direct impact of fluctuating commodity prices. The concern is that temporary spikes in energy prices could embed themselves into wage demands and business pricing strategies, leading to a more persistent inflation problem.

Limited Evidence of Second-Round Effects Supports Central Bank’s View

To date, there has been limited empirical evidence to suggest significant "second-round effects" stemming from the elevated energy prices. This lack of broad-based price increases beyond the energy sector provides crucial support for the central bank’s view that underlying inflation remains consistent with price stability. This aligns with both the Bank of Canada’s latest projections and the base case forecasts from many economic analysts, which anticipate a gradual return of inflation towards the 2% target over the coming years. Many such forecasts also suggest that the Bank of Canada will likely maintain its current interest rate through 2026, signalling a period of prolonged monetary policy stability.

Resilient Household Spending Amidst Inflationary Headwinds

The economic landscape is further illuminated by recent retail sales data. Statistics Canada’s preliminary estimate indicates a 1% increase in nominal retail sales for June. This growth was primarily fueled by stronger sales at gasoline stations, a direct reflection of higher energy prices, and increased motor vehicle purchases.

When adjusted for price effects, to provide a truer measure of consumer spending volume, retail sales are estimated to have rebounded by approximately 0.5%. This figure is consistent with tracking that suggests household spending has remained resilient, even in the face of higher energy costs. This resilience in consumer demand is a key factor that the Bank of Canada will be monitoring, as sustained strong spending could potentially exert upward pressure on inflation.

Background Context: The Inflationary Surge and the BoC’s Response

The current economic juncture is a consequence of a significant inflationary surge that began in 2021, driven by a confluence of factors including supply chain disruptions stemming from the COVID-19 pandemic, strong consumer demand fueled by fiscal stimulus, and, more recently, the impact of geopolitical events on global commodity prices, particularly energy and food.

In response to escalating inflation, the Bank of Canada embarked on an aggressive monetary tightening cycle. Beginning in March 2022, the central bank systematically raised its policy interest rate, moving from an emergency low of 0.25% to its current level of 5.0%. This rapid increase in borrowing costs was designed to cool demand, bring inflation back to the 2% target, and anchor inflation expectations.

The decision to hold rates steady for the past six consecutive meetings reflects the central bank’s assessment that its cumulative rate hikes are working to curb inflation. However, policymakers have maintained a data-dependent approach, emphasizing that further rate increases remain a possibility if inflation proves more persistent than anticipated.

Timeline of Key Inflationary Events and Central Bank Actions

- Early 2021: Inflation begins to pick up globally as economies reopen post-pandemic and supply chain issues emerge.

- Late 2021 – Early 2022: Inflationary pressures intensify, driven by a combination of demand, supply, and energy price shocks.

- March 2022: Bank of Canada raises its policy interest rate for the first time in the current tightening cycle, from 0.25% to 0.50%.

- Throughout 2022: A series of aggressive rate hikes follow, as the Bank of Canada strives to bring inflation under control.

- Early 2023: Inflation begins to show signs of moderation, particularly headline inflation.

- June 2023: The Bank of Canada pauses its rate hikes for the first time, holding the policy rate at 4.75%.

- July 2023: Inflation data shows a slight uptick, prompting the Bank of Canada to resume rate hikes, raising the policy rate to 5.0%.

- September 2023 – Present: The Bank of Canada maintains its policy interest rate at 5.0%, signaling a period of careful observation. The June 2024 CPI report is the latest key economic indicator to be assessed.

Supporting Data and Economic Indicators

The analysis of inflation trends is often supported by a range of economic data points. Beyond the CPI itself, economists monitor:

- Producer Price Index (PPI): This index measures the average selling prices received by domestic producers for their output. Changes in PPI can be a leading indicator of future CPI movements.

- Wage Growth: Strong wage growth can contribute to inflation if it outpaces productivity gains, leading to higher labor costs for businesses that are then passed on to consumers.

- Consumer Confidence Surveys: These surveys gauge consumers’ willingness to spend, which influences overall demand in the economy.

- Manufacturing and Services PMIs (Purchasing Managers’ Indexes): These surveys provide insights into the health of the manufacturing and services sectors, including price pressures faced by businesses.

- Housing Market Data: Shelter costs, including mortgage interest, rent, and property taxes, are a significant component of the CPI and are closely watched.

Potential Implications of the June CPI Report

The implications of Monday’s CPI report are far-reaching:

- Bank of Canada’s Monetary Policy: A lower-than-expected inflation reading would reinforce the central bank’s decision to hold rates steady and potentially increase confidence that further tightening is not required. Conversely, a higher reading could reignite concerns about inflation persistence and put pressure on the BoC to reconsider its current stance.

- Market Expectations: The report will influence expectations for future interest rate movements, impacting bond yields, currency exchange rates, and stock market performance.

- Household Budgets: The inflation rate directly affects the purchasing power of Canadian households. A continued easing of inflation would provide some relief, while persistent high inflation would continue to strain family finances.

- Business Investment and Planning: Businesses will use inflation data to inform pricing strategies, wage negotiations, and investment decisions. Stable and predictable inflation is generally conducive to long-term business planning.

Official Responses and Forward-Looking Statements

While specific statements regarding the upcoming June CPI report are unlikely before its release, the Bank of Canada has provided consistent guidance on its inflation mandate. Governor Tiff Macklem and his colleagues have repeatedly stated their commitment to returning inflation to the 2% target. They have also highlighted their focus on distinguishing between temporary price shocks and more entrenched inflationary pressures.

The central bank’s communication strategy typically involves press conferences following interest rate decisions and the publication of the Monetary Policy Report, which outlines their economic projections and inflation outlook. These communications will be crucial in interpreting the significance of the June CPI data.

Broader Economic Context and Outlook

Canada’s economy is navigating a complex environment. While inflation has shown signs of cooling, the impact of higher interest rates is still filtering through the economy, potentially slowing growth. The resilience of the labor market and consumer spending has been a notable feature, but there are concerns about the sustainability of this strength as borrowing costs remain elevated.

The upcoming CPI report will be a key piece of the puzzle, helping to shape the narrative around Canada’s economic trajectory. A confirmed trend of moderating inflation would provide a welcome sign of economic stability, allowing the Bank of Canada to potentially shift its focus towards supporting sustainable economic growth. However, any resurgence in price pressures would necessitate continued vigilance and a data-driven approach to monetary policy. The interplay between energy prices, food costs, and underlying inflationary momentum will be closely watched by policymakers, businesses, and consumers alike.

{kind=link}