Fuel for the 2nd Wave of Inflation: Import Prices of Manufactured Goods, Driven by Computers & Electronic Products

According to the latest BLS report, import prices for all goods have surged by 6.6% during the first six months of 2024, reaching a new record high. On a year-over-year basis, the increase stands at 7.1%. It is important to note that these figures are measured at the "water’s edge," meaning they represent the price of goods as they arrive at U.S. ports and do not include the additional costs of domestic tariffs. This upward trajectory signals a potent "second shock" to the economy, following the initial disruptions caused by the global pandemic.

The Statistical Reality of Rising Import Costs

To understand the current inflationary environment, one must look beyond the aggregate numbers. While the overall index is up, the internal components of the data reveal a shift in the primary drivers of inflation. In previous decades, the importation of electronics and manufactured goods served as a deflationary force, helping to keep overall U.S. consumer prices low. However, that trend has reversed sharply.

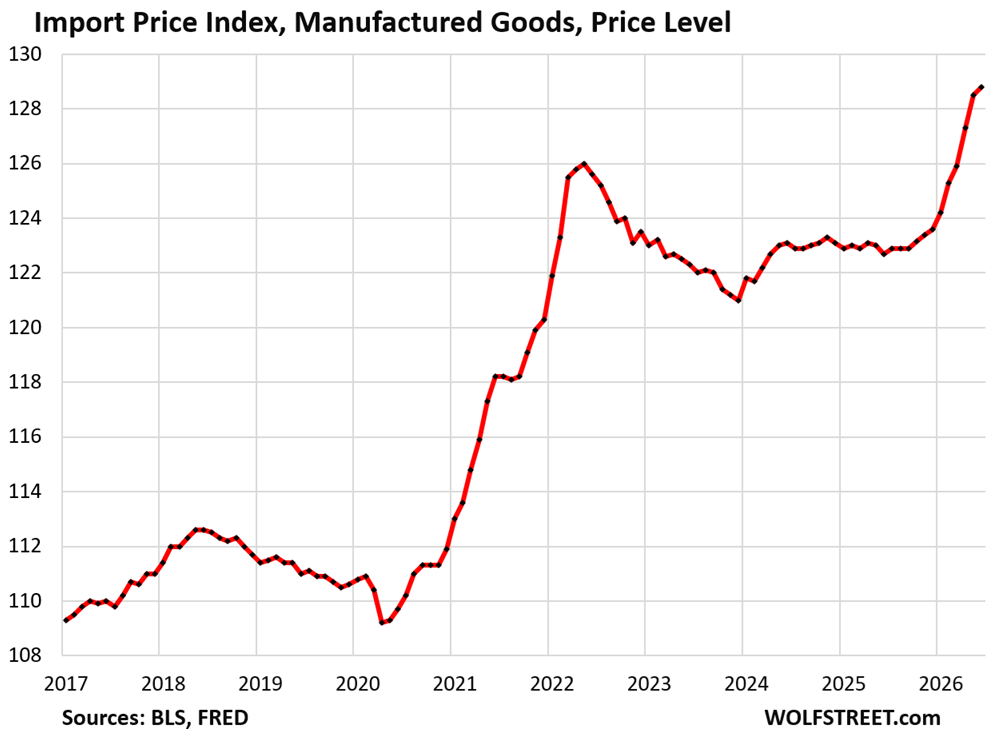

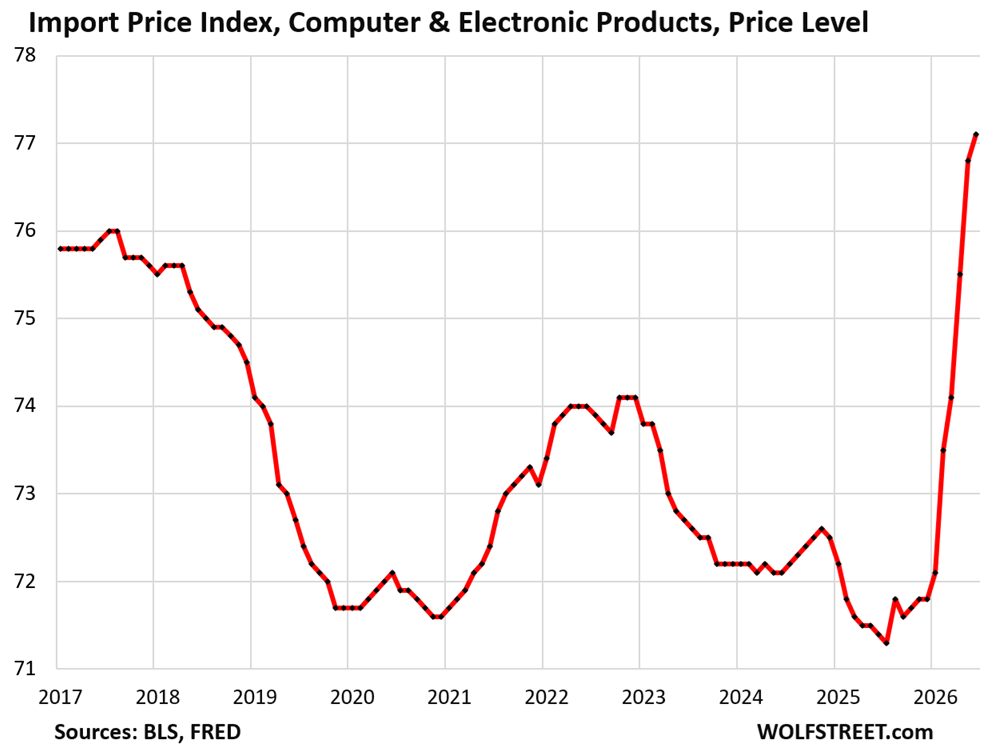

The price level of manufactured goods—which accounts for a massive $2.9 trillion of U.S. imports over the last 12 months—has risen by 4.2% in the first half of this year. Year-over-year, this sector has seen a 5.0% increase. Within this category, the most striking escalation is found in computer and electronic products. This subgroup has witnessed a 7.4% price jump over the first six months of 2024 and an 8.0% increase compared to the same period last year.

This data is particularly noteworthy because it contradicts nearly two decades of historical pricing trends. Between 2006 and 2019, the import price index for computers and electronic products declined by nearly 30%. During that era, rapid advancements in manufacturing efficiency and the globalization of tech supply chains meant that consumers and businesses received more computing power for less money every year. The current reversal suggests that the structural "tech deflation" that the U.S. economy relied upon for years has, at least temporarily, vanished.

A Chronology of Two Shocks

The current price environment is best understood as the second of two distinct waves of disruption. The first wave, occurring between 2021 and early 2023, was characterized by "supply-chain chaos." This period saw global logistics networks paralyzed by pandemic-related lockdowns, labor shortages, and a sudden, massive shift in consumer spending from services to goods. As families transitioned to remote work and distance learning, demand for laptops, monitors, and home office equipment spiked just as factories in Asia were struggling to maintain production. This mismatch led to widespread shortages and the first major spike in import prices in the modern era.

By mid-2023, it appeared that the worst had passed. Import prices began to retreat as supply chains normalized and the "shortage of everything" turned into a glut of inventory for many retailers. However, this period of relative stability was short-lived.

The second shock, which began in early 2024, is arguably more profound because it is driven not by a temporary logistics failure, but by an unprecedented explosion in capital investment. The catalyst is the Artificial Intelligence (AI) boom. Unlike the pandemic-era shock, which was driven by retail consumers buying gadgets, the current shock is driven by massive corporations and venture-backed startups racing to build out the physical infrastructure required to support generative AI.

The AI Investment Boom: Sucking Up Global Capacity

The sheer scale of the AI investment boom is difficult to overstate. Hyperscale cloud providers, including Microsoft, Alphabet (Google), Amazon, and Meta, have committed hundreds of billions of dollars to capital expenditures (CAPEX) aimed specifically at AI data centers. This "arms race" for AI supremacy has created a massive demand for high-end semiconductors, specialized servers, and advanced electronic components.

Manufacturing capacity for high-performance chips, such as NVIDIA’s H100 and B200 GPUs, is currently the most significant bottleneck in the global economy. These products, along with the high-bandwidth memory (HBM) and advanced packaging solutions they require, are being produced at near-maximum capacity. Because demand far outstrips supply, and because the buyers are some of the wealthiest corporations in history, price sensitivity has effectively disappeared.

Startups and established tech giants alike are "blowing money left and right," according to market analysts, in a desperate bid to secure the hardware necessary to train large language models. This corporate spending spree is directly reflected in the 8% year-over-year jump in imported computer and electronic prices. When the world’s largest companies compete for a limited pool of manufactured goods, the price of those goods inevitably moves toward record highs.

The Energy Context: 2024 vs. The 1970s

While rising import prices often evoke memories of the 1970s oil crises, the current economic landscape features a critical difference: the United States’ role as an energy powerhouse. In the 1970s, high fuel prices acted as a direct tax on the U.S. economy, siphoning wealth to foreign oil-producing nations. Today, the situation is more nuanced.

While fuel import prices rose earlier this year, the U.S. is currently the world’s largest producer of crude oil, natural gas, and petroleum products. The nation runs significant trade surpluses in energy, exporting vast quantities of gasoline, diesel, jet fuel, and propane. Consequently, while higher fuel prices hurt individual American consumers at the pump, they bolster the U.S. economy as a whole by increasing export revenues. This provides a structural cushion that was absent during previous inflationary cycles.

Similarly, while the price of nonmonetary gold saw volatility and a spike earlier in the year, its impact on broader inflation remains marginal compared to the systemic shift in manufactured goods and technology components.

Implications for Businesses and Consumers

The surge in import prices is not staying confined to the corporate balance sheets of tech giants. There are growing indications that these costs are migrating "downstream" to the average consumer. As the cost of components and servers rises, service providers are beginning to adjust their pricing models for cloud storage, software subscriptions, and digital services.

More tangibly, the increased cost of imported electronics is expected to impact the retail prices of consumer goods. Smartphones, laptops, home appliances, and even modern automobiles—all of which rely heavily on the same semiconductor ecosystems currently being squeezed by AI demand—are likely to see price hikes or a lack of promotional discounting in the coming quarters.

Retailers who had previously benefited from falling import costs in 2023 are now facing a renewed squeeze on their margins. For the Federal Reserve, this "second shock" presents a significant challenge. The central bank has been looking for "sticky" inflation to cool, but the surge in import prices for essential tech and manufactured goods suggests that the path back to a 2% inflation target may be more arduous than previously anticipated.

Broader Economic Analysis and Future Outlook

The current trend in import prices represents a fundamental shift in the global trade dynamic. For decades, the "China Price"—the ability to manufacture goods cheaply overseas and import them into the U.S.—acted as a ceiling on domestic inflation. The combination of geopolitical tensions, the "near-shoring" of supply chains, and now the AI-driven demand for high-end technology has shattered that ceiling.

Industry analysts suggest that the AI investment boom is in its "build-out" phase, which typically involves the highest level of capital intensity. As long as the race for AI dominance continues, the demand for electronic components will likely remain at levels that test the limits of global manufacturing capacity.

Furthermore, the data suggests that the U.S. economy is experiencing a transition from "consumer-led inflation" to "investment-led inflation." While the 2021 shock was about people wanting more stuff than the world could ship, the 2024 shock is about the world’s most powerful companies wanting more technology than the world can build.

As the U.S. continues to import $3.3 trillion in goods annually, the 7.1% year-over-year increase in prices will remain a formidable headwind for the economy. If the "second shock" proves as persistent as the first, the era of cheap imported electronics may be officially over, replaced by a new reality where the cost of technology is a primary driver of the cost of living. For now, the "huge" impact of the AI boom is written clearly in the import price data, signaling that the battle against inflation is far from won.

{kind=link}