Kulipa: Bridging the Divide Between Stablecoins and Everyday Spending for Modern Fintechs

Kulipa has emerged as a pivotal infrastructure provider in the rapidly evolving landscape of digital finance, offering a robust "stablecoin engine" that enables fintechs, neobanks, and crypto wallets to seamlessly integrate stablecoin-backed cards and accounts into their offerings. Founded with the ambitious goal of making digital dollars spendable in the real world, Kulipa’s B2B payment infrastructure addresses a critical gap: the inherent friction in converting on-chain stablecoin value into usable fiat currency for everyday transactions. This review, current as of June 2026, delves into Kulipa’s product, operational mechanics, regulatory strategy, market traction, and competitive positioning, offering a comprehensive assessment for potential builders and industry observers.

The Unmet Need: Stablecoins in the Real World

The cryptocurrency market has witnessed an explosion in the adoption and capitalization of stablecoins like USDC, which are designed to maintain a stable value pegged to fiat currencies, typically the U.S. dollar. These digital assets have become essential tools for remittances, cross-border payments, and a safe haven during crypto market volatility, with trillions of dollars in value transacted monthly on various blockchains. However, despite their utility as a store and transfer of value, the practical application of stablecoins for everyday purchases at traditional merchants remains largely cumbersome. Most crypto wallets and decentralized applications lack the necessary regulatory licenses, compliance frameworks, and direct integrations with card networks like Visa and Mastercard to facilitate real-time, compliant stablecoin-to-fiat conversions at the point of sale.

This is precisely the challenge Kulipa aims to solve. By bundling the complex layers of card issuance, payment processing, fiat conversion, and regulatory compliance into a single, developer-friendly API, Kulipa empowers fintech companies to launch their own branded stablecoin-backed debit cards and banking services with unprecedented speed and efficiency. Instead of spending a year or more navigating the intricate web of scheme memberships, banking partnerships, and country-specific regulations, a fintech can leverage Kulipa’s infrastructure to go to market in a matter of weeks. The end-user experience remains seamless: they receive a card branded by their preferred app or wallet, unaware of the underlying Kulipa technology facilitating their stablecoin spending.

How Kulipa Functions: On-Chain Settlement and Fiat Conversion

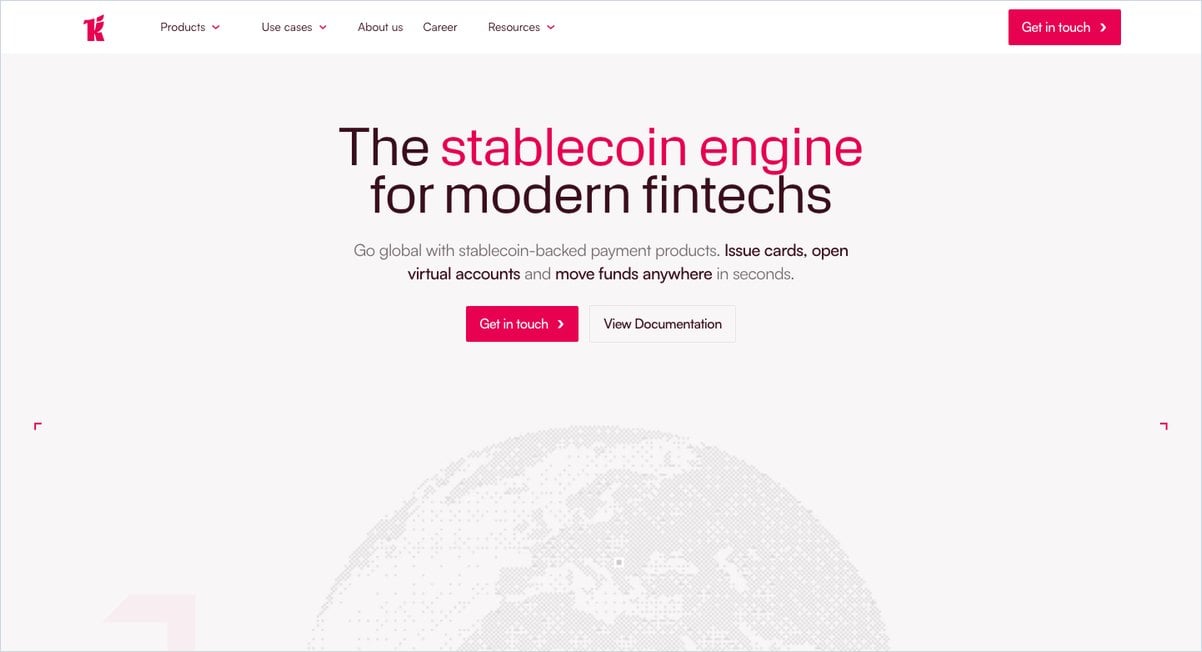

At its core, Kulipa’s innovation lies in its sophisticated settlement mechanisms, which connect a user’s on-chain stablecoin balance to traditional fiat payment rails. The company offers three distinct models, each with specific trade-offs regarding speed, security, and custodial assumptions, allowing clients to choose the best fit for their product and user base:

-

Just-in-Time (JIT) Settlement: This model is designed for speed, requiring a blockchain network capable of near-instantaneous transaction finality (sub-second). When a user initiates a card payment, Kulipa’s system triggers an immediate on-chain transaction to debit the user’s stablecoin balance, convert it to the local fiat currency, and settle with the merchant via the card network. This provides the most direct link between on-chain funds and off-chain spending, but its viability depends heavily on the underlying blockchain’s performance.

-

Cooperative Multi-signature Settlement: In this innovative model, Kulipa acts as a limited co-signer within a user’s self-custodial multi-signature wallet. When a payment is made, Kulipa co-signs the transaction to authorize the stablecoin debit, but the user retains ultimate control over their funds and can revoke Kulipa’s co-signing permissions at any time. This approach maintains the ethos of self-custody prevalent in the crypto community while enabling compliant card spending. It does, however, introduce a shared security assumption, which clients must carefully consider.

-

Prefunded Settlement: This is the most straightforward, though less "self-custodial," option. Users prefund a dedicated wallet managed by Kulipa or a partner, from which card payments are then debited. While simpler to implement and compatible with a wider range of blockchains, this model means users temporarily relinquish direct control over the funds held in the prefunded wallet, softening the "non-custodial" pitch.

In all scenarios, Kulipa manages the complex backend processes: real-time stablecoin-to-fiat conversion, compliance checks (Know Your Customer/Business (KYC), Anti-Money Laundering (AML) monitoring), and fraud prevention. This comprehensive abstraction layer frees fintechs from the burden of building and maintaining these critical but complex financial and regulatory functions in-house. The transparency with which Kulipa outlines the trade-offs of each settlement model is a notable strength, enabling builders to make informed decisions tailored to their specific use cases and risk appetites.

A Comprehensive Product Suite: Cards, Wallets, and Virtual Accounts

Kulipa’s infrastructure is segmented into three primary product offerings, designed to provide a near-complete neobanking stack for its clients:

-

Cards: This is Kulipa’s flagship offering, enabling clients to issue physical and virtual debit cards on major networks like Visa and Mastercard. These cards are fully brandable, support integrations with Apple Pay and Google Pay, and offer features such as instant card freezing for security. Crucially, they function as true debit cards, settling directly from stablecoin balances. Kulipa handles the entire lifecycle for physical cards, from production and packaging to shipping. The platform supports both consumer and business card programs, opening avenues for payroll solutions, expense management, and other corporate financial tools beyond individual spending.

-

Wallets: Kulipa’s wallet infrastructure allows clients to embed bank-account-style balances directly within their applications. This enables users to hold and manage their stablecoin assets within a familiar interface, preparing them for card spending or other financial services offered by the client.

-

Virtual Accounts: Complementing the spending side, Virtual Accounts provide white-labeled bank account details to users. This critical "on-ramp" functionality allows users to receive standard fiat bank transfers (e.g., ACH, SEPA) that are automatically converted into stablecoins and deposited into their in-app wallet balances. Together, these three components form a powerful ecosystem: users can fund their accounts via traditional bank transfers, hold their value in stablecoins, and spend seamlessly with a branded card—effectively creating an on-chain alternative to conventional banking services, as envisioned by partners like Ready.

Technological Agnosticism and Network Reach

Kulipa boasts a chain-agnostic design, asserting its capability to deploy on "any blockchain, from EVM chains to L2 or Solana, and many more." While this flexibility is a significant technical advantage, current practical implementations primarily focus on USDC and its wrapped versions, alongside Paxos-issued stablecoins. This narrower scope for supported tokens, compared to the broader "any stablecoin" impression sometimes conveyed by marketing, necessitates confirmation for specific token support before integration.

On the fiat spending side, Kulipa leverages the unparalleled global reach of Visa and Mastercard. With acceptance at over 150 million merchant locations across more than 100 countries, users of Kulipa-powered cards can spend their stablecoins virtually anywhere traditional cards are accepted, rendering the underlying crypto mechanics invisible to both the merchant and the consumer.

The "Local-First" Regulatory Imperative

One of Kulipa’s most compelling differentiators is its "local-first" regulatory strategy. Unlike many global payment providers that attempt to passport a single license across multiple jurisdictions, Kulipa meticulously pursues regulated coverage market by market, tailoring its product and compliance frameworks to specific local requirements. CEO Axel Cateland emphasized this approach: "We’ve focused on being as local as possible by understanding regulations."

This strategy is particularly insightful given the fragmented and rapidly evolving global regulatory landscape for cryptocurrencies and digital assets. By securing local licenses and building on-the-ground teams, Kulipa mitigates regulatory risk and enhances trust in key markets. Currently, Kulipa holds live issuing capabilities across the European Union, Argentina, and Nigeria, with significant progress being made in the United States.

The selection of these initial markets is strategic:

- European Union: Represents a mature, highly regulated financial market with a robust framework for electronic money institutions and payment services.

- Argentina: A country with high stablecoin adoption driven by economic volatility and a strong demand for inflation-resistant digital assets. Kulipa’s presence here directly addresses a clear market need.

- Nigeria: One of Africa’s largest and most dynamic crypto economies, demonstrating immense potential for digital payments and financial inclusion through stablecoins.

Kulipa’s establishment of local teams in Buenos Aires and Lagos, alongside its head offices in Paris and London, underscores its commitment to this localized approach. The flip side, however, is that "local-first" implies uneven global coverage. Fintechs targeting markets where Kulipa has not yet secured licensing must wait, making the availability of U.S. issuing a deciding factor for many American-based clients. This deliberate, methodical expansion prioritizes compliance and depth over rapid, potentially riskier, global breadth.

Rapid Traction and Credible Backing

Despite only launching its infrastructure in February 2025, Kulipa has demonstrated remarkable early traction. Within months, it had issued over 120,000 cards and secured approximately 20 enterprise clients. Transaction volume was reported to be growing at an impressive rate of roughly 70% month-over-month.

Kulipa’s client roster is not merely decorative; it includes significant players in the fintech and crypto spaces:

- Flutterwave: A leading African payments technology company.

- nSave: A platform focused on cross-border savings.

- Solflare: A major Solana-based wallet.

- Ready (formerly Argent): A prominent smart-wallet provider.

- Privy: A wallet-infrastructure provider, which has publicly documented its integration with Kulipa for self-custodial wallets.

This collection of partners lends considerable credibility to Kulipa’s technology and market fit, especially for a company in its nascent stages. However, as with any young venture, these numbers, while promising, are still early indicators. 120,000 cards issued does not equate to 120,000 active, heavy users, and the payments industry, particularly regarding issues like fraud, chargebacks, and edge-case compliance, often reveals its true challenges at much larger scale over longer operating histories.

Kulipa’s rapid growth has been supported by substantial financial backing. The company raised a $6.2 million seed round in 2025, co-led by Flourish Ventures and 1kx, with additional participation from White Star Capital and Fabric Ventures. This followed a $3 million pre-seed round in July 2024, bringing its publicly reported funding to approximately $9.2 million (or around €10.5 million according to Kulipa’s own statements). The investor profile is telling: Flourish Ventures, a fintech fund focused on financial inclusion, and 1kx, a serious crypto-native investor, together validate Kulipa’s vision of bridging traditional finance with decentralized assets. Flourish Ventures explicitly stated its rationale: stablecoins move trillions monthly on-chain, yet spending them conventionally remains a hurdle, and Kulipa is positioned to build the essential layer to overcome this.

An Experienced Leadership Team

The strength of Kulipa’s leadership team is a significant asset. CEO Axel Cateland brings extensive experience from Mastercard’s digital payments division and as a banking lead at the French unicorn Spendesk. CTO Michael Shynar spent eight years as a staff engineer at Google and contributed to WhatsApp’s commerce platform at Meta. Benoit Roger, Head of Compliance, offers a crucial blend of expertise from mainstream fintech (Nickel, Lemonway) and crypto regulation (Binance France). Diego Sánchez, LATAM GM, is an alumnus of Bitso. This unique combination of traditional payments, deep technological expertise, and specialized crypto regulatory knowledge is precisely what is required to navigate the complex challenges of stablecoin card infrastructure. The company’s diverse team of over 20 professionals is strategically distributed across Paris, London, New York, Buenos Aires, and Lagos, reflecting its global ambitions and local-first strategy.

Competitive Landscape and Market Differentiation

The stablecoin card infrastructure market has become increasingly competitive and well-funded through 2025, with several key players vying for market share. Kulipa faces competition from:

- Rain: A full-stack issuer and Visa Principal Member, primarily targeting enterprise clients with direct issuance capabilities.

- Reap: Similar to Rain, Reap operates as a full-stack issuer and Visa Principal Member, focusing on larger corporate entities.

- Baanx: Perhaps Kulipa’s closest direct competitor, Baanx also offers white-label, self-custodial crypto card solutions. Its acquisition for approximately $175 million in November 2025 underscores the significant value and strategic importance of this market segment.

Kulipa differentiates itself through several key factors:

- Local-First Licensing: Its deliberate, market-by-market regulatory strategy in emerging markets (e.g., Argentina, Nigeria) gives it a unique wedge into regions with high stablecoin adoption but often complex local regulatory environments.

- Truly Self-Custodial Settlement: The cooperative multi-signature model stands out by preserving the self-custody ethos, a critical selling point for many crypto users and projects. This contrasts with some rivals that might rely more heavily on prefunded or custodial models.

- API-First Approach for Fintechs: While competitors like Rain and Reap focus on being full-stack principal members for large enterprises, Kulipa specifically targets fintechs and crypto wallets looking for an agile, API-driven solution to launch branded products without the overhead of becoming a licensed issuer themselves.

Strategic Considerations for Potential Integrators

For fintech builders considering Kulipa, several strategic factors warrant close attention:

Pros:

- Accelerated Time-to-Market: The API-first approach and bundled compliance significantly reduce the time and resources required to launch a stablecoin-backed card program.

- Strong Regulatory Foundation: The "local-first" licensing model provides robust compliance and reduces regulatory risk in supported jurisdictions, fostering greater trust and long-term viability.

- Genuine Self-Custody Option: The cooperative multi-signature settlement model appeals strongly to crypto-native audiences who prioritize control over their digital assets.

- Comprehensive Product Suite: The combination of cards, wallets, and virtual accounts offers a holistic platform for building neobank-like services.

- Experienced Leadership: The founding team’s deep expertise in traditional payments, crypto, and regulation is crucial for navigating this complex domain.

- Proven Early Traction: Rapid card issuance and client acquisition, alongside significant investor backing, demonstrate strong market validation.

- Strategic Market Focus: Targeting high-growth, stablecoin-hungry markets like Argentina and Nigeria provides early access to underserved populations.

Cons:

- Geographical Limitations: The "local-first" model means coverage is uneven; critical markets like the U.S. are still "in progress," delaying entry for many potential clients.

- Limited Stablecoin Diversity: While chain-agnostic, practical support is currently concentrated on USDC and Paxos-issued stablecoins, which might not suffice for projects requiring broader token support.

- Early-Stage Maturity: Despite rapid growth, Kulipa is a young company (launched February 2025). The long-term challenges of fraud, chargebacks, and scaling complex payment infrastructure are yet to be fully tested over several years.

- Opaque Pricing: Kulipa does not publicly disclose its pricing, requiring direct engagement with its sales team for cost estimates. This lack of transparency can be a hurdle for initial assessments.

- Settlement Model Nuances: Integrators must carefully understand the implications of each settlement model, especially the security assumptions inherent in the cooperative multi-signature setup and the latency requirements for JIT.

Expert Tip: Before committing to Kulipa, prospective clients should thoroughly discuss which settlement model is applicable to their chosen blockchain and specific use case, paying close attention to the security implications of co-signing arrangements and the performance requirements for JIT. Furthermore, a detailed understanding of the exact licensing coverage for each target market is paramount, as the "local-first" approach means regulatory capabilities vary significantly by country. These two areas represent the most critical integration risks and require explicit confirmation.

Conclusion: A Credible Bridge to the Future of Finance

Kulipa represents one of the most credible and strategically sound bets in the burgeoning stablecoin card infrastructure market. Its "local-first" regulatory approach is a pragmatic response to a complex global landscape, offering a differentiated entry point into high-growth markets where stablecoins are already indispensable. The commitment to genuinely self-custodial settlement models aligns with the core principles of decentralized finance, appealing to a user base increasingly wary of centralized control. Coupled with a highly experienced team and robust early traction, Kulipa is well-positioned to become a foundational layer for fintechs and crypto wallets aspiring to offer comprehensive financial services powered by digital assets.

While the company is still young, and its global coverage is not yet universal, for builders in Europe, Latin America, or Africa seeking to launch branded stablecoin cards and accounts without the prohibitive overhead of becoming a licensed issuer, Kulipa deserves serious consideration and a thorough technical evaluation. It serves as a vital piece of the puzzle in bringing the efficiency and innovation of stablecoins to the mainstream, driving the convergence of traditional finance with the digital asset economy. As the stablecoin market continues to mature and regulatory clarity evolves, Kulipa’s infrastructure will likely play an increasingly significant role in shaping how digital dollars are spent in the real world.

{kind=link}