Statistical Arbitrage for Independent Traders: Mastering Convergence in Modern Markets

The pursuit of alpha in financial markets often leads independent traders down complex analytical paths, seeking edges that larger institutions might overlook or find too operationally burdensome. Statistical arbitrage, or "stat arb," represents one such avenue, fundamentally betting on the mean reversion of related financial instruments. At its core, stat arb posits that when the price relationship between two correlated assets deviates significantly from its historical norm, it is likely to revert. While pairs trading is the most intuitive manifestation of this strategy, its capital inefficiency and signal wastage can be a significant hurdle for solo operators. This article delves into the advanced "Triangulated Stat Arb" approach, a methodology designed to build a robust universe of high-quality trading pairs, extract valuable signals from them, and aggregate these signals at the individual ticker level to identify mispricings. This sophisticated framework aims to overcome the limitations of traditional pairs trading, offering a more efficient and potentially more profitable strategy for independent traders.

The foundational concept of statistical arbitrage hinges on identifying temporary mispricings between assets that historically exhibit a strong correlation. When these assets diverge, the strategy involves simultaneously taking a long position in the relatively undervalued asset and a short position in the overvalued asset, with the expectation that their price relationship will converge back to its historical average. However, the practical application of this strategy, particularly for individual traders, is fraught with challenges. Traditional pairs trading, while conceptually simple, can tie up significant capital in individual pairs, and signals generated by one pair might not be fully utilized when considering the broader market.

Triangulated Stat Arb, as outlined in previous analyses, addresses these inefficiencies by shifting the focus from individual pairs to individual tickers. This methodology constructs a curated universe of promising pairs, then "flattens" these pairs into per-ticker views, essentially analyzing each asset’s behavior across all the pairs it participates in. By aggregating these ticker-level insights, the strategy aims to pinpoint individual securities that are demonstrably mispriced relative to their correlated peers, allowing for a more diversified and capital-efficient trading portfolio. The efficacy of this approach rests on three critical pillars: the diligent selection of "good pairs," a sophisticated triangulation and consistency mechanism to extract reliable signals, and the integration of external data sources like volume, news, and event-driven information to avoid costly misinterpretations of market movements.

The Crucial Foundation: Identifying High-Quality Pairs

The initial and arguably most critical step in the Triangulated Stat Arb process is the meticulous selection of trading pairs. This stage acts as the primary filter, determining the potential success of all subsequent analytical steps. If the foundation of the strategy is built on a universe of "rubbish" pairs – those that do not exhibit predictable mean reversion – then no amount of sophisticated downstream analysis can salvage the strategy. Conversely, a well-curated universe of high-quality pairs significantly amplifies the value generated by subsequent analytical layers.

The framework for assessing pair quality hinges on two key metrics. The first metric quantifies the potential for frictionless returns by measuring how effectively a pair’s spread has reverted to its mean over a defined lookback window. In essence, it asks: "If we could trade this spread without incurring any transaction costs or slippage, would we have made money by buying the cheaper asset and selling the more expensive one?" Pairs that exhibit persistent divergence, failing to revert to their historical norms, will receive low or negative "reversion-factor" scores, signaling that they should be excluded from the trading universe.

The second metric assesses the consistency of this mean reversion. It investigates whether the spread’s convergence after a divergence is a reliable pattern or merely a random occurrence towards the end of a historical period. A spread that diverges for an entire formation period and then sporadically converges at the very end is far less attractive than one that demonstrates a more consistent tendency to snap back towards its average after deviating.

By combining these two metrics, a robust filter emerges, capable of identifying pairs of stocks that not only tend to diverge and converge but do so with a degree of reliability that makes them amenable to profitable trading strategies. This direct measurement of desirable behavior stands in contrast to more traditional, less direct statistical tests, such as cointegration tests, which may not always capture the nuances of tradable mean reversion.

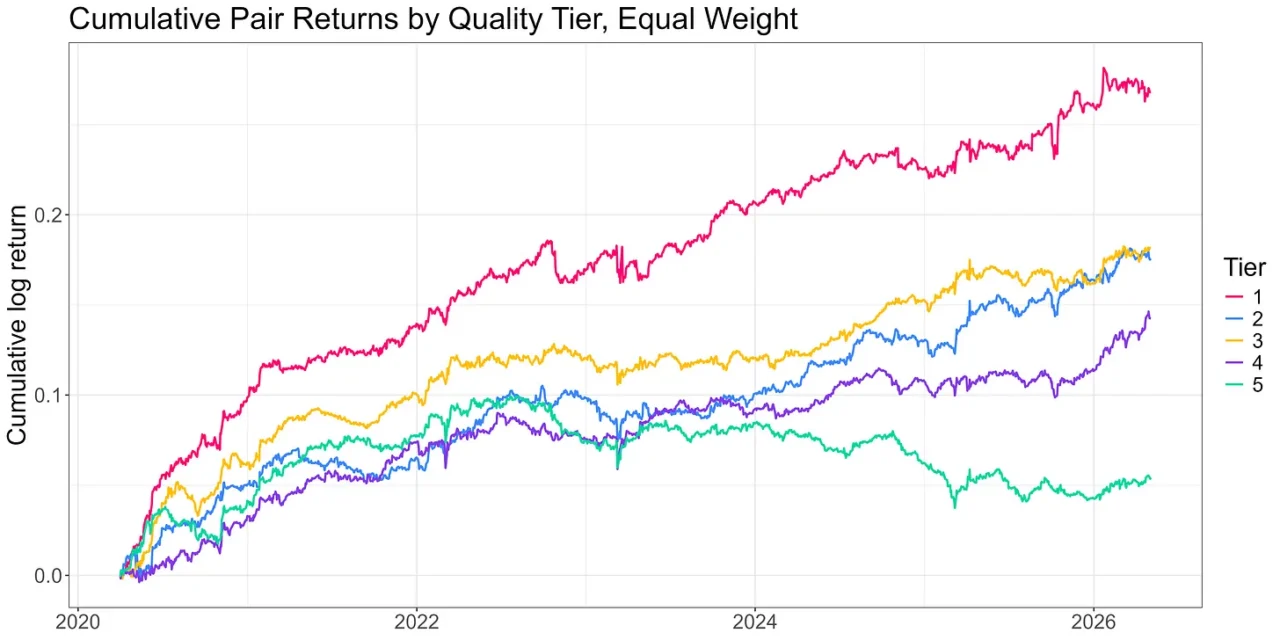

In practice, this ranking system typically identifies the top 10% of pairs from a broad universe of potential candidates. These selected pairs are then further screened to ensure they exhibit economic sense, meaning they are broadly exposed to similar risk factors, such as being in the same industry or sector. This selection process is typically conducted on a monthly basis, utilizing the preceding 24 months of historical price data.

Within this top-tier selection, pairs are often segmented into five distinct tiers. An analysis of before-cost returns for a simple pairs trading strategy applied to each tier, using an equal-weighted approach, reveals the effectiveness of this ranking system. The results consistently show Tier 1 pairs outperforming significantly, while the middle tiers exhibit more variability but still demonstrate reasonable performance. Tier 5, conversely, performs noticeably worse, underscoring the importance of the upstream ranking methodology.

Quantifying risk-adjusted returns across these tiers further highlights the impact of pair selection. A notable spread in Sharpe ratios, often around a 4x difference between the top and bottom tiers, indicates that the quality of the selected pairs is a dominant factor in performance. While total returns for traditional pairs trading can be modest – a drawback addressed by the subsequent triangulation strategy – the risk-adjusted performance derived from superior pair selection is substantial. This initial stage of pair selection is not merely a preliminary step; it is the bedrock upon which the entire strategy is built, dictating the potential for alpha generation throughout the entire pipeline.

The operationalization of this pair selection process involves several subtle yet crucial considerations. These include implementing liquidity filters to ensure tradability, applying industry constraints to maintain economic relevance, defining appropriate refresh cadences for the pair universe, and establishing protocols for handling delistings and corporate actions like acquisitions. Despite these complexities, the overarching principle remains clear: the most significant return on analytical effort comes from the slow, painstaking work of generating a clean, ranked universe of trading pairs. While this approach demands more meticulous effort and deeper analytical thought than simply running a multitude of cointegration tests, its demonstrable effectiveness and the fact that the majority of potential alpha is determined at this early stage make it an indispensable component of the Triangulated Stat Arb strategy.

Enhancing Signal Integrity: Triangulation and Consistency

Once a high-quality universe of trading pairs has been established, the focus shifts to optimizing signal generation and, crucially, addressing the inherent limitations of traditional pairs trading. The core innovation of Triangulated Stat Arb lies in its transition from a pair-centric to a ticker-centric perspective. This transformation is vital for improving capital efficiency and mitigating signal wastage, two significant drawbacks that often hamstring solo traders employing simpler pairs trading strategies.

The process begins by examining each individual ticker that appears within the curated universe of pairs. For every such ticker, the strategy analyzes all the pairs it is a part of. Each pair provides a "per-ticker view," indicating whether the ticker is currently trading at a discount or premium relative to its correlated partner, quantified by a z-score representing the spread’s deviation from its rolling mean. These individual per-ticker views are then aggregated across all the pairs a given ticker participates in. The resulting aggregated view forms the basis of the trading signal for that specific ticker. This aggregation process, detailed in prior analyses, generates a network signal that is inherently more robust than what any single pair could provide. When multiple pairs independently signal that a ticker is mispriced, the confidence in that signal is significantly amplified.

However, a naive aggregation can lead to suboptimal results. Two primary pitfalls can undermine this process:

- Over-reliance on individual pair signals: If a ticker is part of many pairs, but most of those pairs are of lower quality, the aggregated signal can be diluted or distorted.

- Ignoring signal strength variations: Not all pair signals are created equal. Some divergences might be minor, while others are extreme. A simple aggregation might not adequately weigh these differences.

To overcome these challenges, the Triangulated Stat Arb approach incorporates a "consistency" element. This involves assessing how reliably the aggregated ticker-level signal aligns with the individual pair signals and how consistently these signals have manifested over time. Furthermore, the strategy emphasizes trading the "extremes" of the distribution. Similar to how a pairs trader would not initiate a trade at a mere 0.5 z-score, Triangulated Stat Arb focuses on ticker-level signals that are significantly stretched. Trading these outliers, rather than every name in the universe, materially improves the overall performance and capital efficiency.

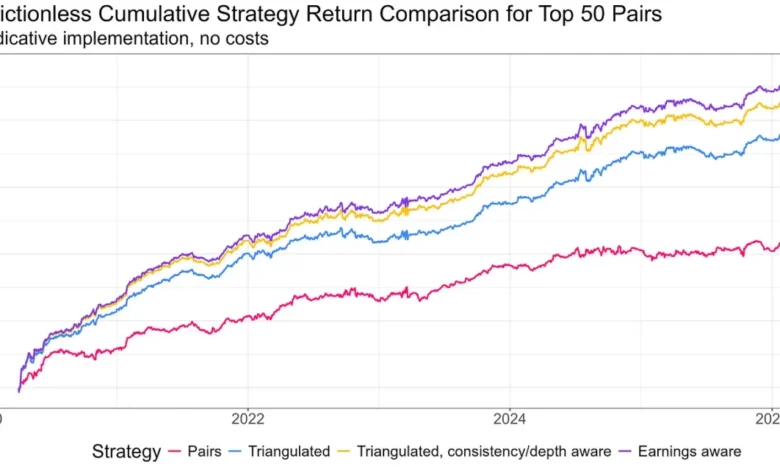

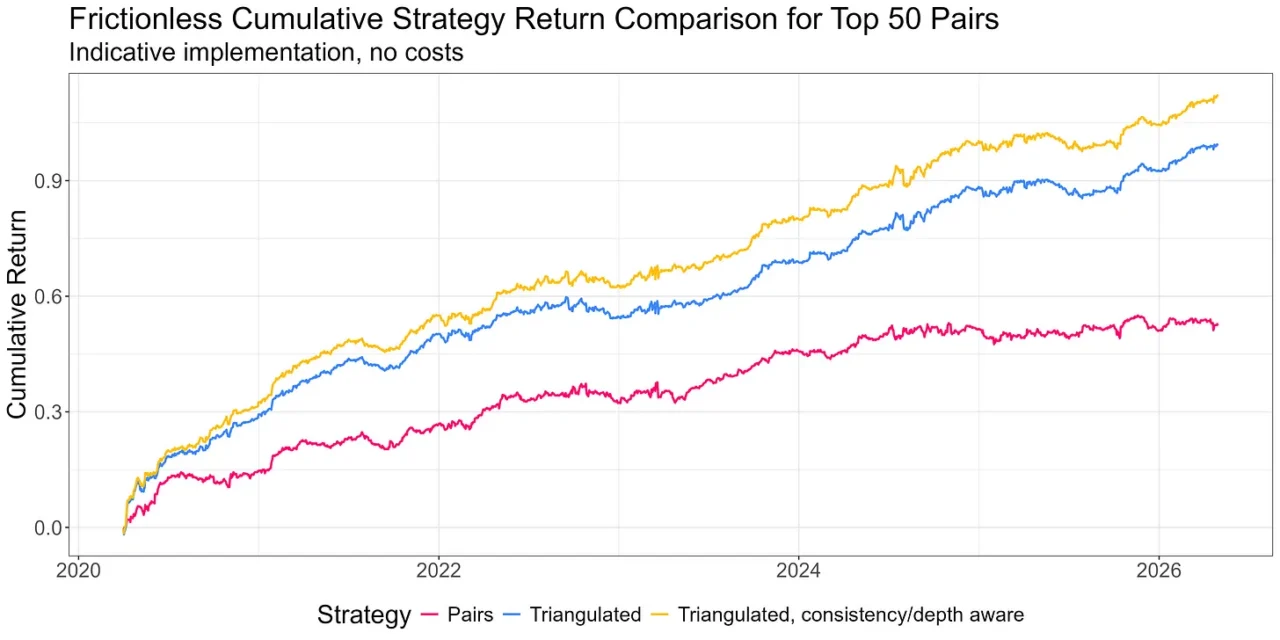

Empirical evidence supports the superiority of this ticker-centric approach. When comparing the cost-free returns of trading a portfolio of the top 50 pairs against trading them as a triangulated long-short portfolio of mispriced legs, the latter demonstrates a significant outperformance. Further refinements, incorporating "depth and consistency" metrics into the signal construction, yield even greater improvements. This methodology offers a substantially more capital-efficient way for independent traders to leverage statistical arbitrage opportunities.

The operational decisions involved in refining the ticker-level signal are crucial. Beyond simply identifying a mispriced ticker, it is important to consider the strength and consistency of the signal. For instance, a ticker that is consistently flagged as mispriced across a large number of high-quality pairs, with significant deviations from historical norms, presents a stronger trading opportunity than a ticker flagged by only a few pairs with marginal deviations. This nuanced approach to signal generation and filtering is key to extracting maximum alpha from the curated pair universe.

Navigating Market Dynamics: Avoiding Pitfalls with External Data

The third crucial pillar of Triangulated Stat Arb addresses a fundamental challenge: distinguishing between temporary, tradable divergences and those driven by genuine, lasting fundamental shifts in asset valuation. The aggregated ticker-level signal, while powerful, indicates that a spread has diverged but not necessarily why. A stretched spread might appear attractive for a mean-reversion trade, but if the divergence is due to new, impactful information that has fundamentally repriced one of the assets, attempting to fade this move would be a costly error.

The key to navigating these situations lies in incorporating external data sources that can provide insights into the underlying drivers of price movements. These sources typically include volume data, news feeds, and event-driven information. The objective is to discern whether a divergence is primarily "technical" (i.e., a temporary imbalance likely to revert) or "fundamental" (i.e., a repricing based on new information, suggesting continuation rather than reversion).

Extensive research has explored the utility of these data sources. Interestingly, the initial intuition regarding volume asymmetry – the idea that forced selling on a cheap leg might look different from informed buying on an expensive leg – yielded a real effect at the pair level. However, when this signal was integrated into the production strategy at the ticker-aggregation level, its impact diminished significantly. The punchline here is that much of the information conveyed by volume was already implicitly captured by the upstream pair-quality selection process. While volume features might be valuable for pure pairs trading, their marginal contribution to the aggregated, triangulated strategy was found to be minimal.

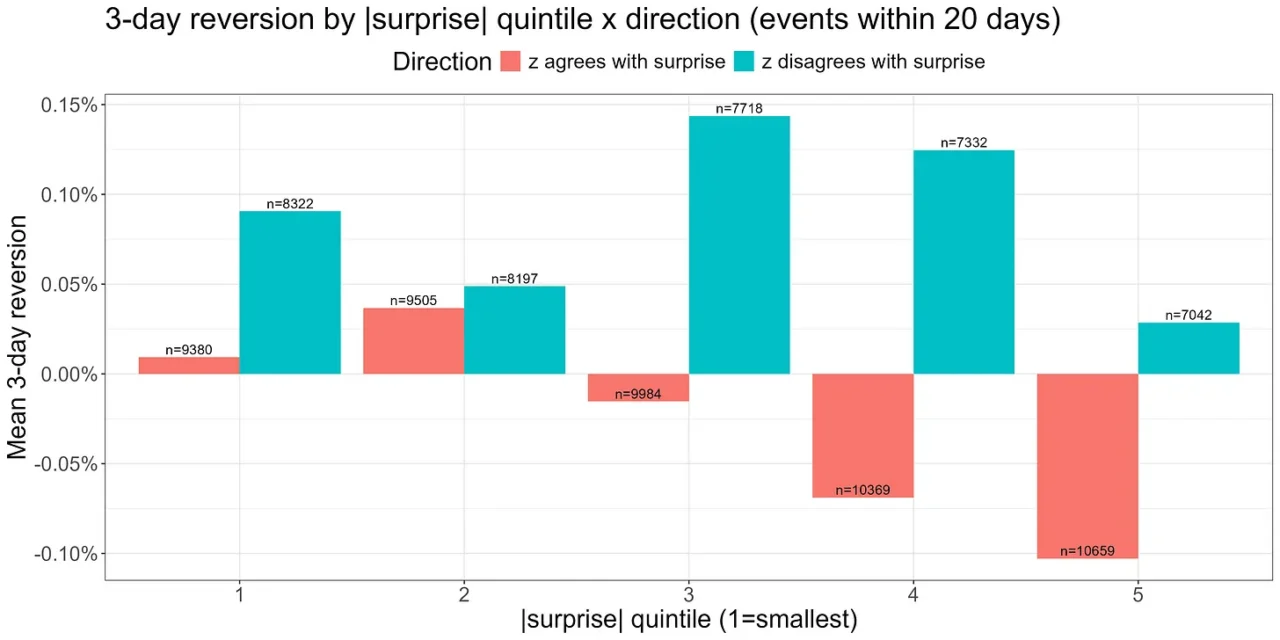

The most significant breakthrough in this third pillar has come from incorporating an earnings filter. The logic is straightforward: when a spread experiences a divergence during an earnings announcement period, and that divergence is in the direction of the earnings surprise, the stock has likely repriced based on genuine, new information. In such cases, attempting to fade this move is ill-advised. This observation is strongly supported by empirical data. A detailed analysis of three-day reversion periods, signed by the negative of the z-score, reveals that when an earnings surprise aligns with the divergence, reversion is significantly weaker. For large surprises, there can even be a continuation of the move, a phenomenon often referred to as post-earnings drift.

The inclusion of an earnings filter in the Triangulated Stat Arb strategy provides a small but meaningful uplift in live trading performance. By identifying and excluding trades where a divergence is likely driven by fundamental news, the strategy avoids costly reversals. This highlights the importance of carefully considering the causal factors behind price movements.

The next frontier in this area involves a broader integration of news features. The intuition that drove the success of the earnings filter is expected to generalize. Any surprise event that causes a significant move in one leg of a spread, based on genuinely new information, is likely to undermine the mean-reversion thesis. Identifying and filtering out such events is a key area for ongoing research and development.

While the third piece of the puzzle – incorporating external data to refine signals – clearly adds value, the observed improvements are often incremental. This is a testament to the effectiveness of the preceding stages. The rigorous pair selection and sophisticated triangulation processes already capture a substantial portion of the potential alpha. It is estimated that the upstream pair-quality work accounts for 80-90% of the overall strategy’s success. Consequently, each subsequent layer, while important, contributes diminishing marginal returns on the effort invested in its development. This hierarchical structure emphasizes that the success of Triangulated Stat Arb is fundamentally determined by the quality of the initial pair universe.

Resourcing the Strategy: Infrastructure and Community for Independent Traders

The methodological framework of Triangulated Stat Arb is only as effective as its implementation and the resources supporting it. For independent traders, the challenge often lies in building and maintaining the sophisticated infrastructure required to execute such a strategy. This is where services and platforms designed to democratize access to advanced trading methodologies become invaluable.

A fully resourced Triangulated Stat Arb strategy necessitates robust data pipelines and analytical environments. This includes access to end-of-day and intraday spread data, crucial for both live trading and ongoing research. The upstream pipeline, responsible for generating a monthly pair universe from thousands of candidate stocks, involves significant data ingestion, cleaning, and computational power for ranking hundreds of thousands of potential pairs. The cost and complexity of building and maintaining such infrastructure alone can be prohibitive for individual traders, often exceeding the cost of premium trading subscriptions.

Platforms that offer a comprehensive data API, historical feeds, and a dedicated research environment provide a critical advantage. Such environments allow members to not only execute trades but also to explore the underlying data, test hypotheses, and refine their understanding of the strategy. The ability to interact with the full historical datasets upon which the methodology was built empowers traders to investigate the nuances of pair selection, explore new features for signal refinement, and experiment with different signal construction techniques.

Furthermore, the availability of an example implementation notebook is a surprisingly potent asset. While there is no single "canonical" signal that fits every trader, these notebooks provide a starting point, illustrating how to configure various parameters such as universe size, weighting schemes, no-trade buffers, signal thresholds, and leverage. This flexibility is essential, as the optimal configuration will vary based on individual account sizes, cost structures, risk tolerances, and operational capacities. A trader managing a $5 million portfolio full-time will have different constraints and objectives than a part-time trader managing $100,000.

The true value of such a resourced approach extends beyond the technical infrastructure. It fosters a community of like-minded traders who are not only running solo operations but also possess a deep understanding of what they are trading, why they are trading it, and the associated trade-offs. This collaborative environment is instrumental in developing traders’ independence and equipping them with the knowledge to navigate market complexities effectively. The research and development process itself is often a collaborative effort, with community members contributing insights, asking probing questions, and even sharing their own research that can be integrated into the live strategy. This symbiotic relationship ensures that the methodology evolves and improves, benefiting all participants.

In essence, the Triangulated Stat Arb methodology, when properly resourced through advanced infrastructure and a supportive community, transforms a potentially overwhelming analytical endeavor into a realistic and sustainable strategy for independent traders. It provides not just the tools to trade but the knowledge and context to become more adept and self-sufficient market participants.

The Hierarchy of Returns and the Path Forward

The Triangulated Stat Arb methodology, when fully resourced, presents a clear hierarchy of returns. The foundational work of selecting high-quality pairs at the universe level yields the most significant gains, accounting for the lion’s share of the strategy’s potential alpha. The subsequent aggregation of signals across pairs, moving to a ticker-centric view, provides a meaningful uplift by improving capital efficiency and signal robustness. Further refinement through depth- and consistency-aware filtering adds another layer of improvement, albeit smaller. Finally, the integration of external data, such as the earnings filter, contributes further incremental gains, while other avenues like volume analysis and news integration represent ongoing frontiers for exploration.

This pattern of diminishing marginal returns is consistent: each successive analytical step, while valuable, contributes less to overall performance than the preceding one. This underscores the paramount importance of the initial pair selection process; it is the stage where the strategy’s ultimate success or failure is largely determined.

The Triangulated Stat Arb approach fundamentally redefines the viability of equity pairs trading for independent operators. By shifting the focus from capital-intensive pairs to diversified ticker portfolios and incorporating sophisticated signal refinement techniques, it overcomes many of the traditional limitations. The provision of necessary infrastructure – including data APIs, research environments, and example implementations – is what makes this advanced strategy accessible without demanding the resources of a full-time engineering team.

For traders who have followed the evolution of this strategy, the conceptual roadmap is now clear. The Triangulated Stat Arb methodology offers a structured and data-driven approach to statistical arbitrage, empowering independent traders with a sophisticated toolset for navigating modern markets. The continued development and refinement of this strategy, supported by robust infrastructure and a collaborative community, promise to deliver consistent value and foster greater independence for those who embrace its principles.

{kind=link}