The Taguchi Method, Robust Design, and What It Means for Trading Systems

Genichi Taguchi’s framework for designing systems that are less sensitive to noise maps directly to algorithmic trading. This guide explains the method, translates it into trading language, and shows how Build Alpha applies these principles automatically.

Genichi Taguchi, a luminary in the field of quality engineering and experimental design, pioneered a systematic approach to off-line quality control that revolutionized manufacturing processes, initially in Japan and later gaining significant traction globally. His methods were lauded not merely for achieving target performance metrics, but more critically, for their emphasis on reducing variation around those targets. While some specific aspects of his methodology faced criticism from statisticians, Taguchi’s enduring influence stems from his popularization of a powerful, overarching concept: a truly good design is one that performs well consistently, even in the face of unpredictable disturbances. This principle, remarkably prescient, resonates deeply with the challenges faced by algorithmic traders striving for consistent profitability in dynamic markets.

The Taguchi Method, at its core, is a framework designed to create products and processes that exhibit reduced sensitivity to variability. Taguchi redefined quality not by adherence to a rigid specification sheet, but by the minimization of "loss" incurred when performance deviates from a predetermined target. This expected loss, he argued, is a function of both the average performance and the degree of variation around that average. This perspective fundamentally shifts the focus from a binary pass/fail assessment to a continuous measure of quality, where even a design that performs adequately under ideal conditions but falters under minor stress is considered suboptimal. For traders, this translates directly: a strategy with a dazzling historical backtest that disintegrates when subjected to slight parameter adjustments, altered timeframes, or noisy data is not robust; it is an overfit strategy, a testament to poor design in Taguchi’s estimation.

A cornerstone of Taguchi’s philosophy is the distinction between "controllable factors" and "noise factors." Controllable factors are the elements within the designer’s purview, the variables that can be deliberately set and adjusted. In the context of algorithmic trading, these encompass a wide array of decisions: the logic governing trade entries and exits, the parameters for stop-loss and take-profit orders, the chosen holding periods, the trading timeframe, the implementation of filters, the methodology for portfolio weighting, and the rules for position sizing.

Conversely, noise factors represent the inherent variability and unpredictability that plague real-world systems and cannot be fully controlled by the designer. For trading systems, these include the capricious nature of market regime shifts, fluctuations in volatility, the unpredictable variations in spreads and slippage, the sensitivity to specific sample windows or start dates, the imperfections in trade execution, minor shifts in trading parameters, and the artificial variations introduced by synthetic or perturbed market paths.

The fundamental objective of the Taguchi Method is to meticulously select and configure these controllable factors in such a way that the system’s output becomes remarkably insensitive to the influence of noise factors. This is achieved not by attempting to eliminate or control the noise itself – an often futile endeavor in financial markets – but by engineering the system’s design to be resilient, requiring the "noise" to cooperate minimally for acceptable performance. This principle of robust design, articulated succinctly, forms the bedrock of the comprehensive robustness testing methodologies offered by platforms like Build Alpha.

One of the most impactful contributions of Taguchi’s framework is its proactive approach to acknowledging and integrating noise into the experimental process. Rather than treating noise as an abstract concept to be avoided, Taguchi advocated for its deliberate inclusion. He proposed a structure involving an "inner array" for controllable factors and an "outer array" for noise factors. For each potential design configuration tested within the inner array, the experiment is replicated across multiple noise settings. The ensuing analysis then considers both the average response and its variance across these noisy conditions.

Translating this into the language of modern trading strategy development, the Taguchi approach to testing emphasizes a crucial paradigm shift: Do not merely evaluate your strategy in a pristine, idealized environment. Instead, intentionally introduce disturbances and meticulously observe which designs demonstrate resilience and survive the onslaught. In the realm of algorithmic trading, the practical equivalents of this "injecting noise" include a range of sophisticated testing techniques.

The trading lens through which Taguchi’s principles are viewed within platforms like Build Alpha focuses on identifying strategy structures that maintain acceptable performance even as market conditions evolve. This aligns directly with the concept of robust parameter design, a notion often underestimated by many traders. The framework can be elegantly mapped onto trading terminology:

| Taguchi Concept | Trading Equivalent |

|---|---|

| Controllable factors | Entry logic, exit logic, stops, timeframe, filters, sizing |

| Noise factors | Regime shifts, vol changes, slippage, date sensitivity, parameter shifts |

| Inner array | Strategy design space – rule combinations being tested |

| Outer array | Stress environment – noise, Monte Carlo, synthetic data, walk-forward segments |

| Signal-to-noise ratio | Mean performance relative to performance variation across noise tests |

| Robust design | Strategy that survives robustness tests |

| Loss function | Drawdown, variance of returns, performance degradation under stress |

The "inner array" and "outer array" concept finds a direct parallel in trading research. The inner array represents the strategy design space, encompassing the myriad combinations of rules, parameters, and logic that define a trading strategy. This is where the core of the strategy’s logic is explored. The outer array, on the other hand, represents the stress environment. This is where the strategy is subjected to the rigors of realistic market conditions, including various forms of noise, Monte Carlo simulations to introduce randomness, synthetic data generation to mimic potential future market paths, and distinct walk-forward segments to assess performance across different historical periods.

Instead of posing the simplistic question, "Which strategy generated the most profit in a single, idealized test?", the robust design approach encourages a more profound inquiry: "Which strategy consistently demonstrates sound behavior even after repeated exposure to market noise and variability?" This is the quintessential question that robustness testing aims to answer.

Central to Taguchi’s method for comparing different designs is the "signal-to-noise" (SNR) ratio. This metric allows for an evaluation based on both the mean performance and its associated variation. Traders intuitively grasp this concept; they recognize that a strategy yielding high in-sample results but collapsing under slight modifications, or one that exhibits wild swings based on minor assumptions, is not desirable.

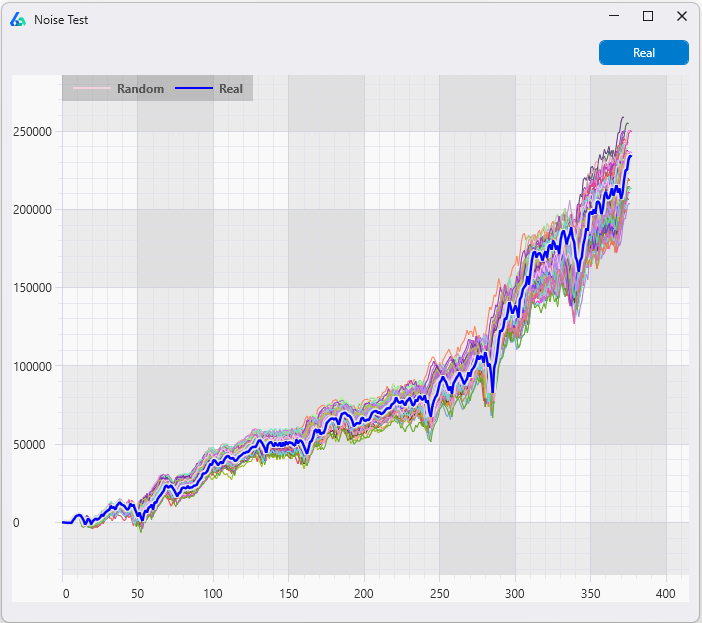

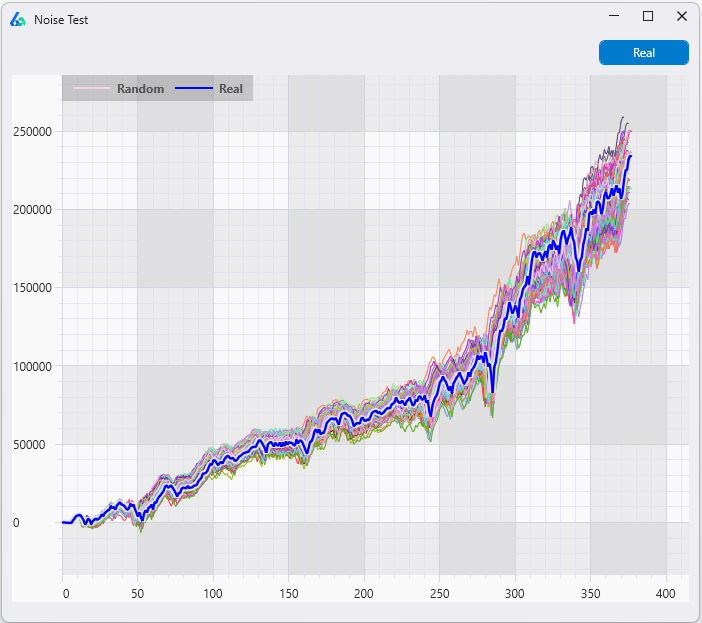

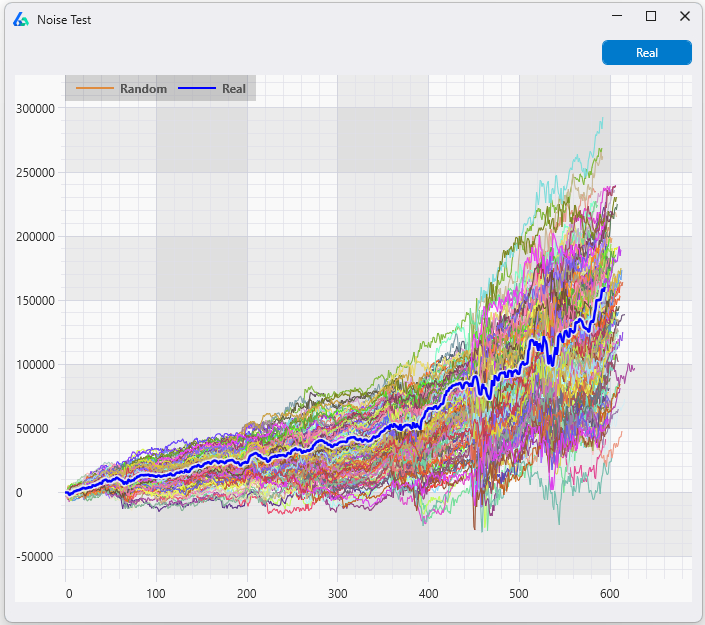

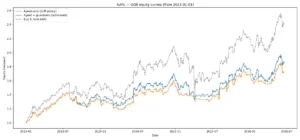

Consequently, raw net profit alone is insufficient as a performance indicator. A strategy boasting the highest return might, paradoxically, be the least attractive if it is acutely sensitive to noise. A strategy with a more modest return but exhibiting stable behavior across a spectrum of realistic market perturbations may ultimately prove to be the superior choice for live trading. This principle underpins the value of tools like Build Alpha’s Noise Test, which quantifies signal-to-noise behavior by assessing the tightness of an equity curve’s distribution across thousands of noise-adjusted data series, as opposed to a wide, scattered dispersion.

A compelling illustration of the Taguchi principle in action can be observed in case studies examining strategies with seemingly identical backtests. When subjected to the Noise Test, which deliberately perturbs historical data to expose sensitivity to noise, two strategies with nearly identical historical performance can diverge dramatically. One strategy might exhibit tight clustering of its equity curves across all noise-adjusted scenarios, indicating robustness and low sensitivity to variation. The other, however, might show wide dispersion, revealing that its historical success was largely a product of fitting to the specific noise present in that particular historical dataset, thus exhibiting high sensitivity to variation. This stark contrast highlights the critical difference between a mere backtest and a truly robust design.

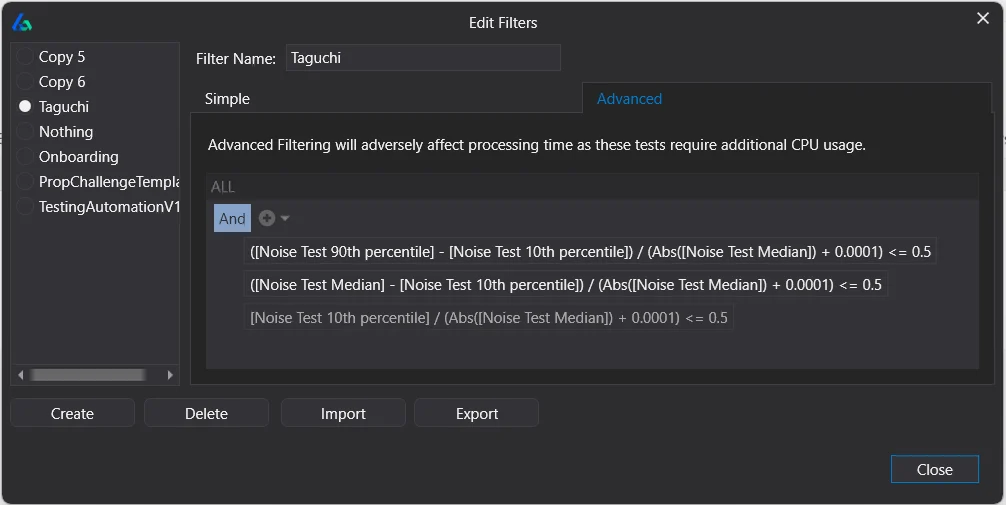

To operationalize Taguchi’s philosophy in trading, several modern, trading-centric formulas have been developed. These formulas aim to reward satisfactory central performance while penalizing excessive sensitivity to noise. While not direct replicas of Taguchi’s original mathematical formulations, they are adapted for evaluating strategy performance across various noise tests:

1. Normalized Percentile Spread

- Formula: (P90 – P10) / (|Median| + 0.0001)

- Measures: The width of the performance distribution across noise tests relative to the typical (median) result.

- Interpretation: A lower value indicates better robustness, signifying less instability. A higher value suggests greater fragility and scatter in outcomes. This acts as a general fragility measure, quantifying how dispersed the noise test results are.

2. Downside Robustness Loss

- Formula: (Median – P10) / (|Median| + 0.0001)

- Measures: The extent to which the weaker performance scenarios (lower percentiles) fall below the central case (median).

- Interpretation: Lower is better. This metric is particularly valuable for traders as it isolates the downside risk, focusing on how severe negative outcomes can be relative to the typical performance.

3. Survival Ratio Under Stress

- Formula: P10 / (|Median| + 0.0001)

- Measures: The proportion of the median result that is retained in the weakest performance scenarios.

- Interpretation: A higher ratio is desirable when the median performance is positive. This metric effectively identifies strategies whose median performance appears acceptable but whose lower tail performance is significantly compromised under stress.

These formulas are most potent when integrated into an automated workflow, transcending the status of a one-off statistic. Platforms like Build Alpha facilitate an automated pipeline where strategies are generated and then rigorously filtered, with only those that meet predefined robustness thresholds being presented. This automated process shifts the optimization objective from merely achieving the "best backtest" to a more holistic goal: optimizing for good central performance, acceptable downside risk, and demonstrably lower sensitivity to market noise. This represents the practical implementation of Taguchi’s philosophy.

The automated workflow seamlessly integrates with existing robustness pipelines, encompassing noise testing for deliberate disturbance, synthetic data generation for simulating realistic market variations, "vs. random" testing to verify genuine edge, noise test parameter optimization to assess parameter sensitivity, and walk-forward optimization to gauge temporal robustness. This comprehensive approach, often detailed in robustness testing guides, ensures a multi-faceted validation of trading strategies.

However, a necessary caution is warranted: while Taguchi’s methods have been profoundly influential, they are not infallible. Statistical criticisms have been leveled at his use of orthogonal arrays, suggesting they might overlook critical interaction effects between controllable factors. Certain experimental choices have also been deemed overly simplistic.

In the context of trading, where interactions are ubiquitous – a specific filter might only enhance performance with a particular exit strategy, or a stop-loss level might prove effective on daily charts but fail on intraday data – understanding these nuances is crucial. The most valuable takeaway from Taguchi’s work is not a rigid adherence to his literal formulas, but rather the adoption of his philosophy of robustness. This philosophy champions the understanding that no single test is sufficient; a comprehensive pipeline of diverse testing methodologies is essential for building truly resilient trading systems.

In essence, the focus should shift from merely seeking the strategy with the most impressive backtest to identifying strategies that maintain reasonable behavior even after noise, variation, and stress have been deliberately introduced. This refined definition of robustness more accurately reflects the realities of live market trading, and platforms like Build Alpha are dedicated to automating this rigorous validation process.

Frequently Asked Questions

-

What is the Taguchi Method in trading?

The Taguchi Method, when applied to trading, refers to the application of Genichi Taguchi’s quality engineering principles to design trading strategies that are inherently less sensitive to market noise and variability. This means developing systems that perform reliably not just in historical backtests, but also under the dynamic and often unpredictable conditions encountered in live markets, such as regime changes, parameter fluctuations, slippage variations, and data noise. -

How does robust design apply to algorithmic trading?

Robust design in algorithmic trading involves systematically distinguishing between controllable factors—the elements a trader can directly influence, like entry rules, exit logic, and stop-loss levels—and noise factors, which are the uncontrollable market elements like shifts in volatility, execution quality, and market regimes. The primary objective is to select controllable settings that render the trading strategy’s performance minimally susceptible to these noise factors. This is precisely the outcome that comprehensive robustness testing aims to identify. -

What is the signal-to-noise ratio for trading strategies?

In the context of trading strategies, the Taguchi signal-to-noise ratio (SNR) is a metric used to evaluate the consistency of a strategy’s performance. It measures how stable the strategy’s returns are across various noise-adjusted tests relative to its average performance. A strategy that exhibits high returns but also significant performance dispersion across noise tests is considered to have a low SNR, suggesting it might be overfit to the historical data. -

Does Build Alpha use the Taguchi Method?

Build Alpha embodies the core philosophy of the Taguchi Method. It focuses on generating a multitude of trading strategy candidates and then subjecting them to rigorous testing environments designed to simulate real-world market disturbances. Only strategies that demonstrate consistent and acceptable performance under these stressful conditions are presented. The platform’s suite of over 12 robustness tests serves as the trading equivalent of Taguchi’s "outer array," designed to expose strategies to deliberate noise and variation. -

What is the difference between optimization and robust design?

Optimization typically aims to find the specific set of parameters or rules that yield the maximum performance within a single, defined test scenario. In contrast, robust design seeks to identify parameters or rules that maintain good performance across a wide range of different conditions and potential disturbances. Recognizing this fundamental difference between simple optimization and the pursuit of robust design is critical for avoiding the pitfalls of overfitting and developing strategies that have a higher probability of performing well in live trading.

{kind=link}