The Iran Conflict Triggers Unprecedented Market Volatility and Historic V-Shaped Recoveries

The financial markets have experienced a period of extreme turbulence, marked by a swift and significant downturn following the onset of the Iran conflict in late February, followed by an equally rapid ascent to new all-time highs. This pattern of sharp declines and immediate recoveries has become a defining characteristic of the current market cycle, prompting analysis into the underlying drivers and long-term implications. Data from Bespoke Investment Group reveals that this is the first time in a century that the S&P 500 has achieved new record highs within 11 trading days after experiencing a 5-10% correction. This phenomenon challenges traditional market wisdom, which posits that markets typically "take the stairs up and the elevator down." Instead, the past decade has witnessed a reversal, with the "elevator down and the elevator right back up again" becoming a recurring theme.

A Decade of Accelerated Market Cycles

The current market behavior is not an isolated incident but rather an acceleration of a trend observed over the past decade. Several notable instances illustrate this pattern:

- 2018 Mini-Bear Market: Following a period of volatility in 2018, the market demonstrated a swift recovery, erasing earlier losses.

- COVID-19 Crash (2020): The most dramatic example occurred in 2020, where the market experienced its fastest-ever run-up to new all-time highs after a decline exceeding 30%. This "COVID Crash" was a stark illustration of the market’s ability to rebound with unprecedented speed.

- "Liberation Day" Rally: A subsequent rally, described as "Liberation Day," also saw a rapid recovery and push to new highs.

- Iran Conflict Trigger: The recent market reaction to the Iran conflict, with its nearly 10% S&P 500 decline followed by a swift return to record levels, adds another data point to this trend.

The only significant deviation from this V-shaped recovery pattern in recent years was the inflation surge of 2022. While this period saw a bear market, it is characterized as a more "run-of-the-mill non-recessionary bear market," suggesting that even downturns are now being navigated with a degree of resilience not seen in previous economic cycles.

The Information Age and Instantaneous Reactions

The increasing speed of market cycles has been a subject of discussion for years. As early as 2014, analysts noted the accelerating pace of market movements. A senior figure in fixed income at Vanguard, speaking at the time, highlighted the profound shift: "One big difference between when I arrived at Vanguard and today is the speed of the markets. In 1981, when a news event occurred, you could sit and contemplate it. If something happened overseas, it might not affect U.S. markets, and if it did, it took a day or so. Now geopolitics is so much more important. Everything is instantaneous. We have to make snap decisions all the time without waiting."

This observation has only become more pertinent in the ensuing decade. The proliferation of information, the 24/7 news cycle, and the immediacy of global communication have created an environment where market participants react to events with unprecedented speed. This has led to shorter decision-making windows and a greater emphasis on rapid adjustments to portfolios and strategies.

Broader Economic Indicators Mirror Market Acceleration

The accelerated cycle phenomenon is not confined to the stock market; it is evident across various economic indicators.

Labor Market Dynamics

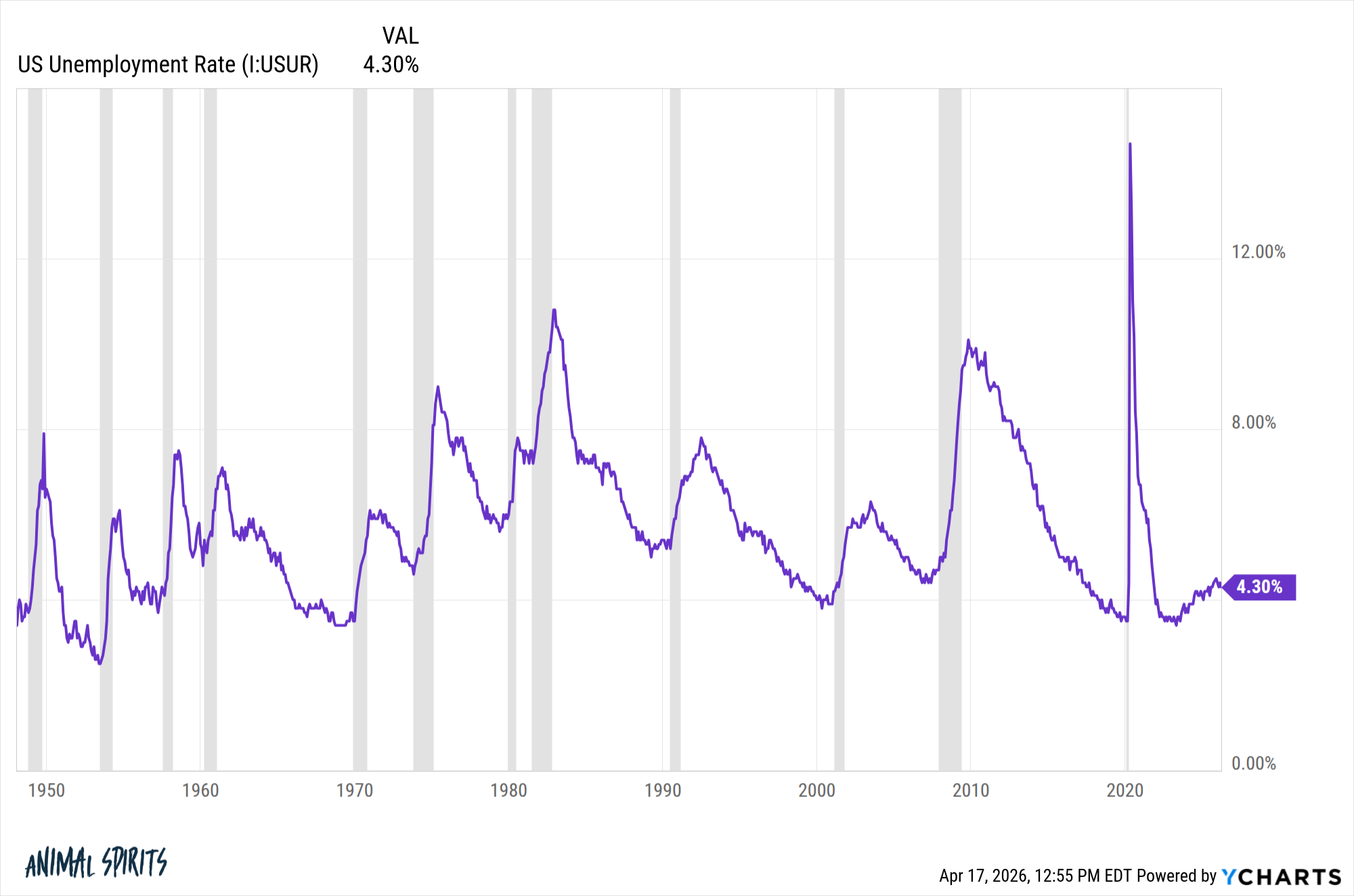

Following the brief but sharp COVID-19 recession, the U.S. labor market experienced its fastest recovery on record. The unemployment rate plummeted from nearly 15% in early 2020 to around 3.5% within two years. This rapid rebound underscores the dynamic and often unpredictable nature of the current economic landscape.

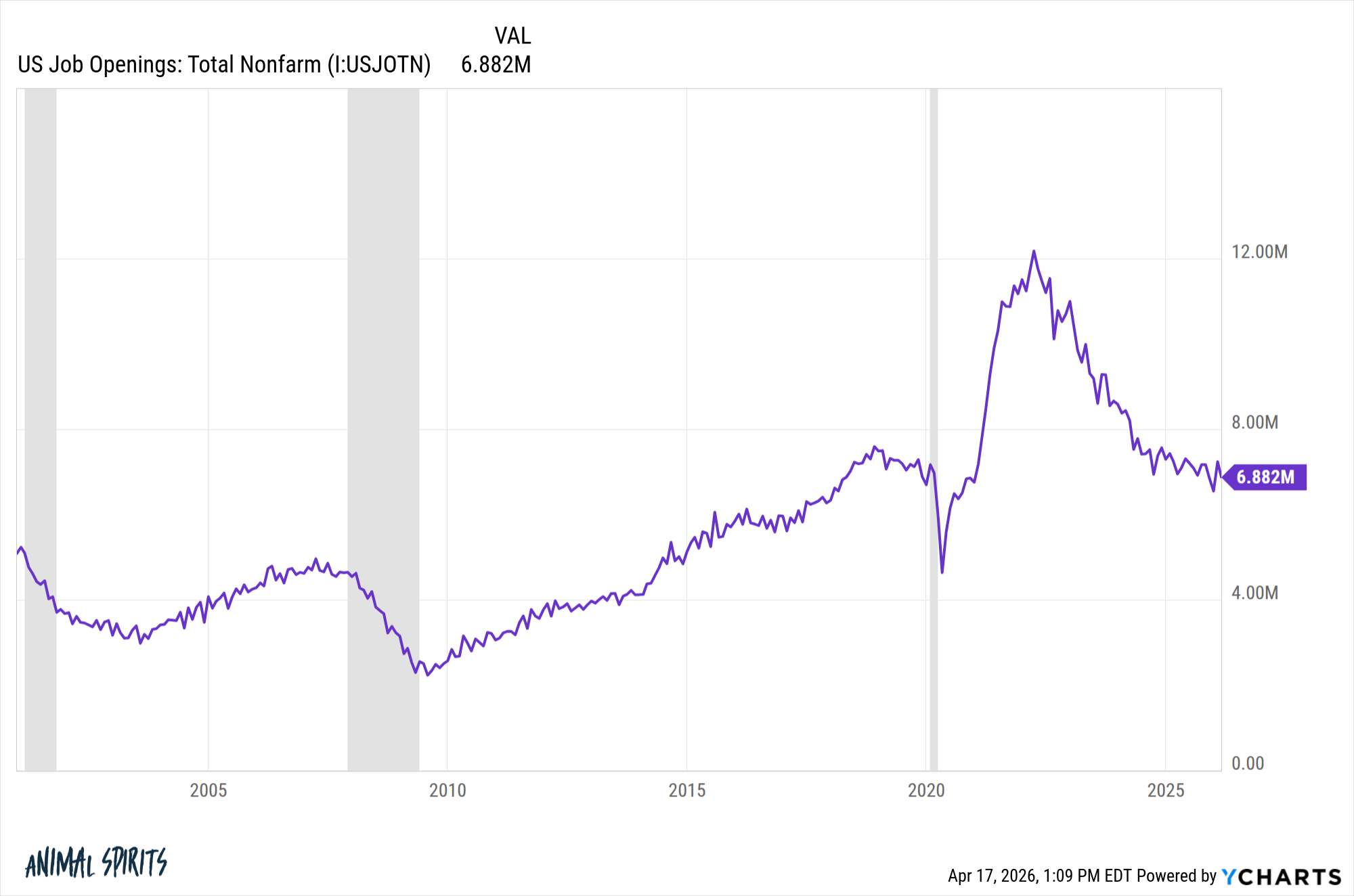

Furthermore, the pandemic fueled an unprecedented surge in job openings. Pre-pandemic levels hovered around 7 million, but at the peak of the labor market’s frenzied activity, job openings exceeded 12 million. This imbalance created a strong leverage for workers, leading to significant wage growth and a highly competitive hiring environment. However, this dynamic has also reversed, with job openings trending downwards and concerns about the impact of Artificial Intelligence on employment becoming more prominent. The shift from a worker’s market to one where job security is a growing concern illustrates the rapid swings in economic sentiment and conditions.

Oil Market Volatility

The oil market has been a prime example of extreme price swings in the 2020s. Starting at approximately $60 per barrel at the end of 2019, crude oil prices famously plunged into negative territory, reaching -$37 per barrel in early 2020. This unprecedented event was largely attributed to a collapse in demand due to global lockdowns and a simultaneous oversupply.

The subsequent recovery was equally dramatic. Prices surged to over $120 per barrel following the Russia-Ukraine war, driven by supply concerns and geopolitical tensions. While prices have since moderated, they experienced another sharp spike above $120 when the Iran conflict escalated, before settling back to around $80 per barrel. This rollercoaster ride highlights the sensitivity of oil prices to geopolitical events and global economic sentiment.

Interest Rate Environment

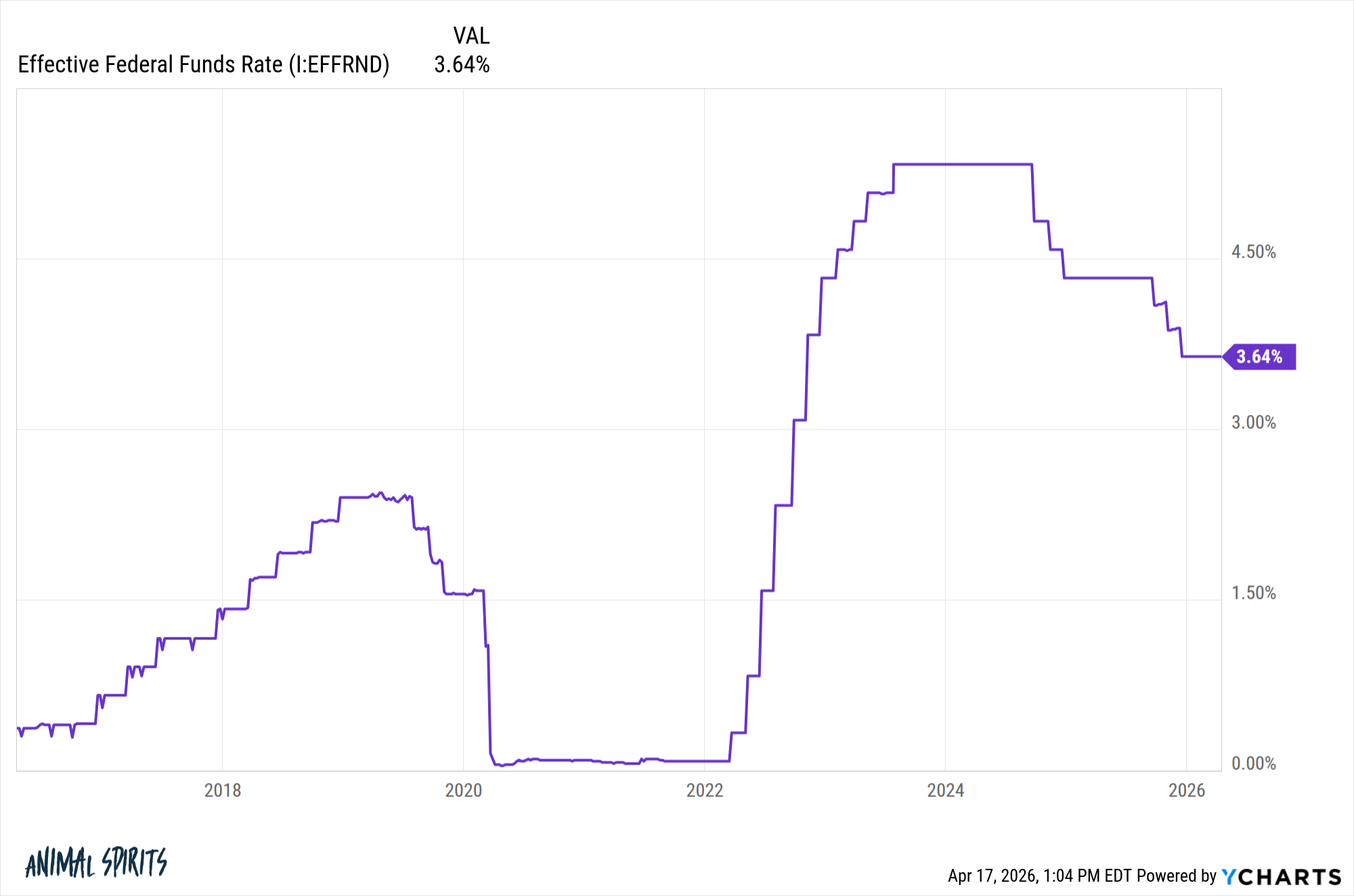

The interest rate landscape has also undergone significant transformations. For much of the 2010s, following the Great Financial Crisis, the Federal Funds rate remained near historic lows. The Federal Reserve’s attempts to normalize rates towards the end of the decade were hampered by trade tensions, and the onset of the COVID-19 pandemic sent rates back to near zero.

The subsequent surge in inflation prompted one of the most aggressive monetary tightening cycles in history. The Federal Reserve rapidly increased the Federal Funds rate from 0% to over 5% in just over a year. This swift action had a ripple effect across the economy, most notably impacting mortgage rates. The 30-year fixed mortgage rate climbed from below 3% in late 2021 to over 8% by the fall of 2023, representing a substantial increase in borrowing costs for consumers.

Global Inflation Trends

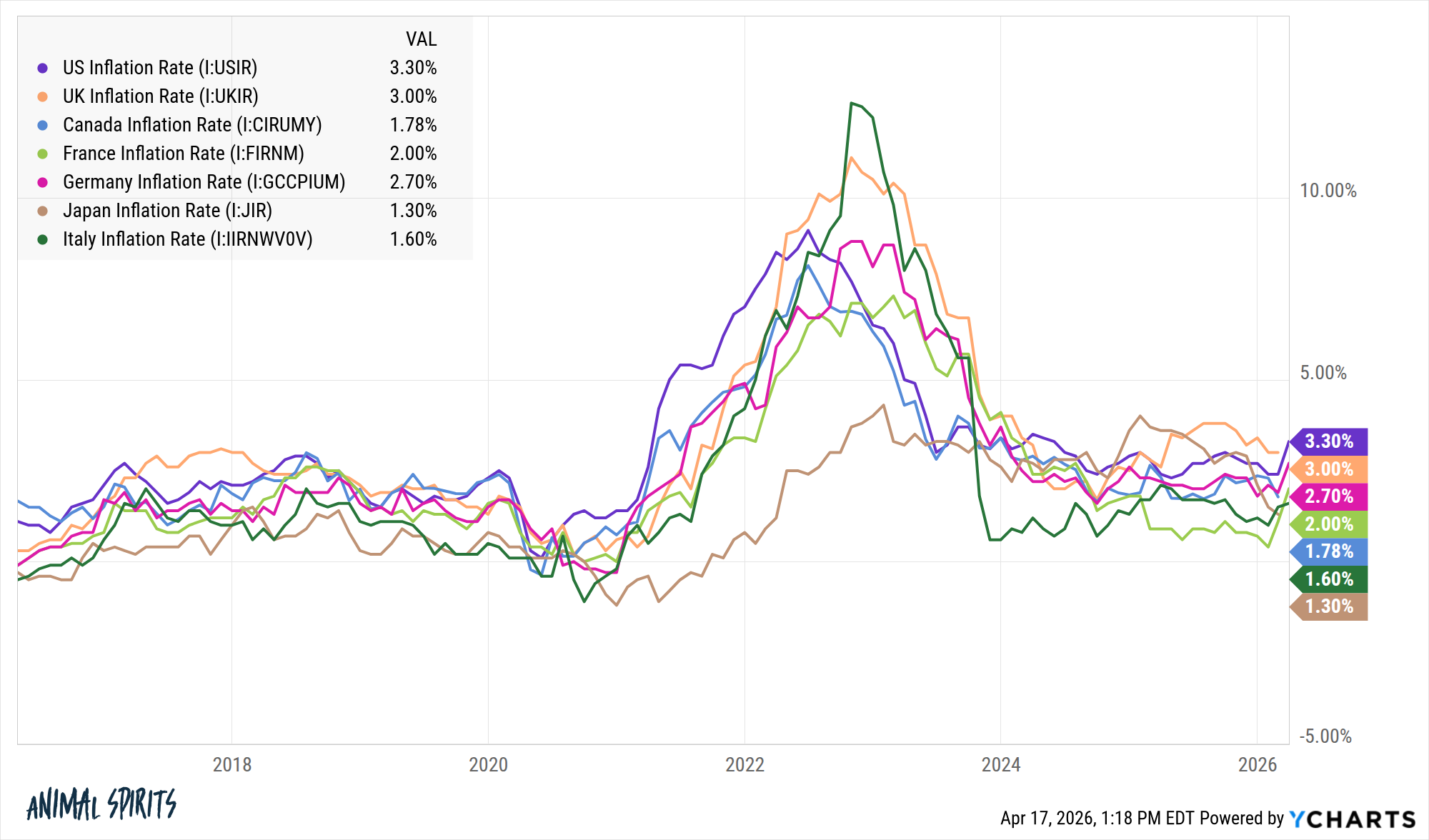

Inflationary pressures have also been a global phenomenon. After a prolonged period of low inflation, many countries experienced a sharp increase, driven by supply chain disruptions, increased government spending, and pent-up consumer demand. However, as central banks have tightened monetary policy and supply chain issues have eased, inflation rates have begun to moderate, returning closer to historical averages. This rapid ascent and subsequent descent of inflation over a few years further underscore the accelerated nature of economic cycles.

The Role of Government Stimulus and Money Supply

A significant contributing factor to many of these market and economic swings has been the unprecedented level of government stimulus provided during the pandemic and its aftermath. This stimulus injected substantial liquidity into the economy, leading to a massive spike in the money supply. The subsequent pullback in this stimulus has also contributed to the observed market and economic adjustments. The dramatic increase and subsequent decrease in the money supply demonstrate the powerful influence of fiscal and monetary policy on economic dynamics.

Psychological Impact of Rapid Changes

The rapid and dramatic swings in markets and economic indicators have a profound psychological impact on consumers and investors. Consumer sentiment has remained subdued for extended periods, partly because of the swift and significant increases in prices and mortgage rates. The rapid transition of gas prices from $3 per gallon to $4-$5 per gallon, for instance, represents a shock to household budgets that is difficult to absorb without time for acclimatization.

This acceleration means that traditional notions of market stability and gradual change are being challenged. While V-shaped recoveries have become common, analysts caution that this trend may not be sustainable indefinitely. Economic downturns or financial crises could eventually lead to prolonged bear markets, and labor markets or interest rates may not always rebound with the same alacrity.

The Enduring Impact of the Information Age and Intervention

While the pandemic and its aftereffects are undeniable drivers of these accelerated cycles, there is a strong argument that we are now operating in a fundamentally faster-moving global economy. The pervasive influence of the information age, coupled with significant government intervention in economic affairs, has created an environment where market cycles are shorter, more volatile, and often more extreme. This is a paradigm shift that appears to be permanent, requiring a recalibration of investment strategies and economic outlooks.

The challenge for individuals and institutions lies in navigating this accelerated world. While markets are moving faster, the wisdom of slowing down and adopting a more deliberate approach can become a strategic advantage. This includes rigorous analysis, disciplined decision-making, and a long-term perspective that is not easily swayed by short-term volatility.

Looking Ahead: Navigating a Faster World

The recent market behavior, triggered by geopolitical events and characterized by rapid recoveries, is a symptom of a broader trend towards accelerated economic and financial cycles. This acceleration, driven by technological advancements, instant information dissemination, and active government intervention, presents both challenges and opportunities. Understanding the underlying forces at play and adapting investment and economic strategies accordingly will be crucial for navigating the complexities of the modern financial landscape. The ability to remain composed and make informed decisions amidst rapid change may well be the key to success in this evolving environment.

{kind=link}